- Quick take

- 22 January

- Rates South Korea

South Korean GDP shrank in fourth quarter as fiscal stimulus fades

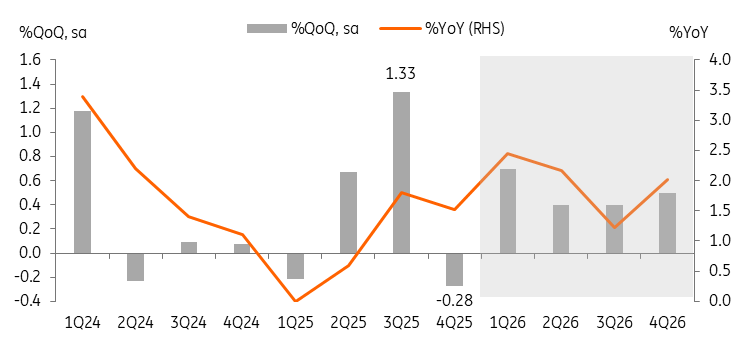

South Korean GDP unexpectedly contracted 0.3% quarter on quarter in the October-December period, partly due to a technical payback from fiscally supported growth. A first-quarter rebound is expected amid strong chip demand and recovering investment. The Bank of Korea is likely to maintain a neutral stance as growth prospects improve

| -0.3% |

4Q25 GDP (%QoQ, sa)2025 GDP growth 1.0% YoY |

| Lower than expected | |

Downside surprise came from the contraction of exports and investment

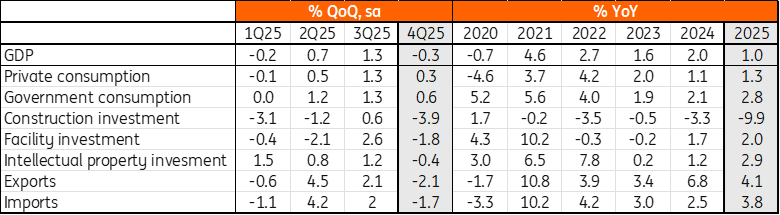

We previously projected fourth-quarter South Korean GDP growth to slow to 0.4% quarter-on-quarter, seasonally adjusted, as fiscal stimulus waned even as strong chip exports likely supported overall export growth. Today's data showed that the economy contracted instead. The slowdown in consumption growth was in line with our expectations. But declines in investment and exports diverged from our estimates. Weak GDP exports likely indicate that robust chip exports are driven by higher prices while auto and machinery exports in real terms dropped due to tariffs and weak global demand. For investment, transportation equipment investment declined sharply, partially offset by IT investment growth.

GDP growth by expenditure

GDP is expected to rebound in 1Q26

Although the 4Q25 growth was weaker than expected, we are keeping our 2026 GDP growth unchanged at 2.0% year on year. Stronger-than-expected chip demand is likely to boost exports and facility investment. After five years of contraction, the construction sector is expected to enter a cyclical recovery. Forward-looking construction orders data have rebounded since last year, and much of the project-finance restructuring has been completed. Private consumption should increase moderately. While a significant rise in domestic equities, expanded welfare programmes, and improved consumer sentiment are likely to be supportive factors, stringent housing regulations and a weak Korean won may temper overall optimism.

GDP is expected to grow 2.0% YoY in 2026 compared to 1.0% in 2025

BoK watch

The weaker-than-expected 4Q25 GDP outcome is not likely to affect the Bank of Korea’s near-term rate trajectory. Most temporary policy influences are subsiding, and the underlying growth trend is showing signs of recovery. We expect the BoK to revise its 2026 GDP forecast from 1.8% YoY to 2.0% when it updates its projections in February. The recovery is likely to be uneven, and the BoK is still concerned about financial instability. As such, the BoK will keep its current neutral tone for an extended period.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more