- Quick take

- 2 September 2021

- South Korea

Korean inflation for August provides another excuse to raise rates

Although the headline inflation rate looks to be driven mostly by food anomalies which probably reflect the recent weakness of the Korean won, a rise in the core inflation rate and fairly broad-based gains in most components could provide an excuse for the Bank of Korea (BoK) to follow up their August rate hike with another in October.

| 0.6 |

MoM%Headline CPI |

| Higher than expected | |

Inflation rise broad based

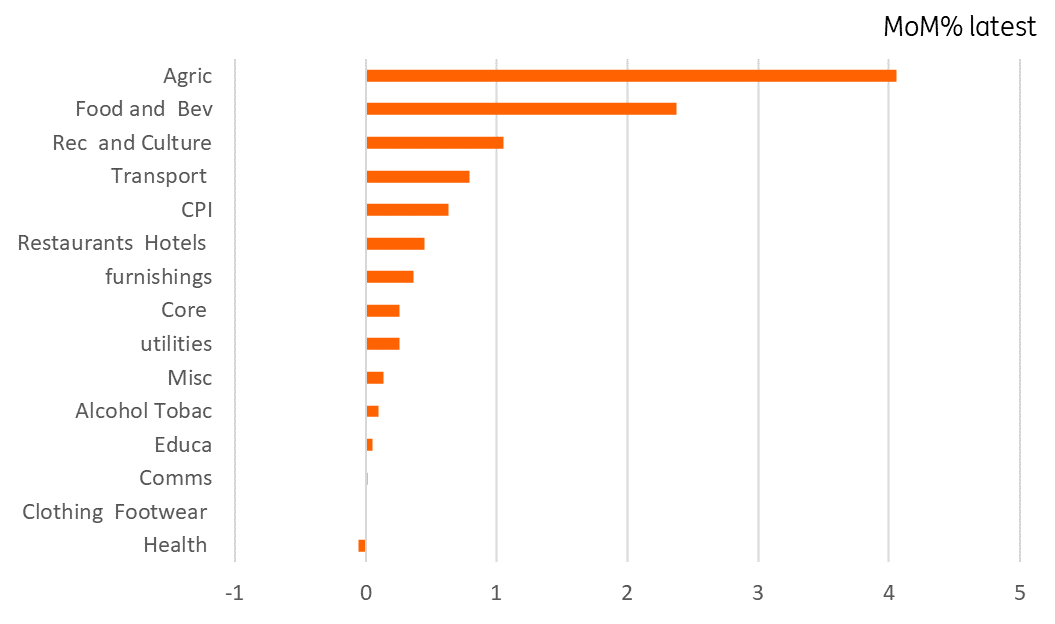

Following months of weak inflation data, the 0.6%MoM increase in the CPI headline index in August was unexpected. Almost every single sub-component of the index rose (the exception being a tiny 0.1% MoM decline in the health index). Headline inflation now stands at 2.6%YoY, unchanged from the July reading.

What seems to be driving prices higher is the weakness of the KRW. The biggest increases were seen in agricultural items, with things like imported beef and other meat rising strongly. The weaker KRW was also reflected in higher energy prices.

But there is some evidence of core inflation rising too. Service-oriented subcomponents, like recreation and culture also showed a strong (1.1%MoM) increase, which we can't blame on the currency. And the core index as a whole was up 0.3% MoM taking the core inflation rate to 1.8%YoY, up from 1.7% in July.

August CPI MoM% by component

Brings October rate hike into play

Although BoK Governor Lee left markets guessing about the BoK's next steps after the August meeting, he did note that policy was still expansionary following the August hike. Together with today's inflation, plus the decent 2Q21 GDP figures, which also received a slight upward revision to 0.8%QoQ today (6.0%YoY), the probability that the BoK follows up with a further hike at their October meeting has definitely gained some ground today. That does not seem to have provided much of a boost for the KRW, which continues to trade just below 1158 as of writing. And as a KRW rally would likely reverse the imported inflation that has driven the August reading, the weaker the KRW, the more likely it is that rates rise again soon.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more