Korea’s third-quarter GDP expands more than expected

Korea’s economy grew 0.6% in the third quarter, as private spending and exports rebounded. Soft survey data suggests a cloudy near-term outlook though while the Bank of Korea is set to remain hawkish

| 0.6% |

Real GDPQuarter on quarter, seasonally adjusted |

| Higher than expected | |

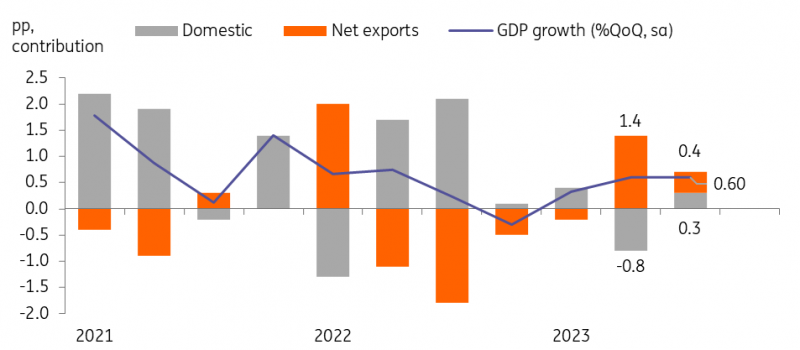

GDP rose 0.6% QoQ sa in 3Q23 with improved details

In terms of domestic growth components, private consumption (0.3%) and construction investment (2.2%) rebounded while the contraction in facility investment (-2.7%) deepened further. Services consumption including leisure, accommodation, and eating out were the main drivers of the rebound but goods consumption was soft as wholesale/retail sales activity contracted. A longer-than-usual Chuseok holiday might have boosted private consumption. Also, as monthly activity data indicated, construction investment recovered on the back of increased government spending on civil engineering and improved supply bottlenecks for construction materials. The positive contribution of net exports narrowed to 0.4ppt compared to the previous quarter's 1.4ppt, but both exports (3.5%) and imports (2.6%) rose. We believe the high-end chip market has led the recent recovery in chip exports.

Exports and consumption led the growth in 3Q23

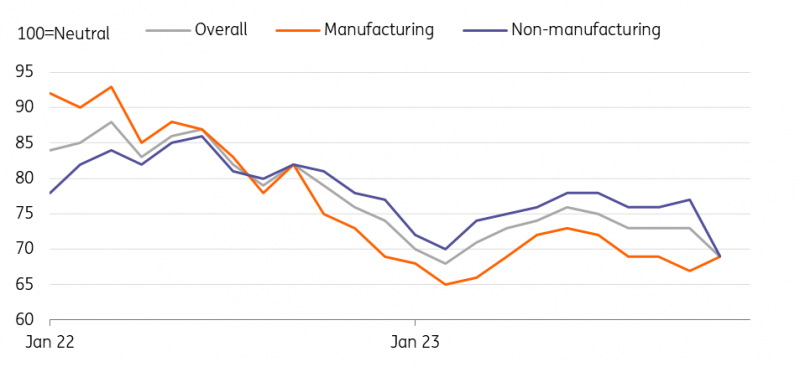

Survey results suggest cloudy growth ahead

Consumer confidence deteriorated further in October (98.1 in October vs 99.7 in September) due to high inflation, high borrowing costs, and high fuel prices. The business survey outcome was also quite gloomy with overall business conditions dropping to the lowest level in eight months. Manufacturing edged up 2pts but was offset by a sharp decline (-8pts) in non-manufacturing. Service activity has been the main driver of growth so far, but there are more clear signs of a slowdown while we expect a gradual manufacturing recovery led by high-end chip markets.

Business survey suggests a weakening service industry

GDP outlook

We expect GDP growth to slow in the current quarter. Private consumption is expected to decelerate on the back of an increased debt service burden and weaker asset market performance. However, various government subsidy programmes, including extending the electric vehicle purchase credit until year-end, will likely provide some stimulus.

We believe the rebound in construction last quarter was temporary, and it is likely to fall back into contraction this quarter as almost all forward-looking construction data suggests a decline. Meanwhile, weak facility investment is expected to continue for at least a couple of quarters. The IT investment cycle will likely rebound next year, but increased funding costs and increased global growth uncertainty will weigh on business investment in the near future.

Exports will contribute positively to growth, especially with the gradual recovery of semiconductors. Yet rising oil prices will push up imports faster, making the positive contribution of net exports smaller or even turning negative depending on oil prices. Putting it all together, GDP will likely expand in the fourth quarter, but at a slower pace than the previous quarter at 0.2% QoQ sa, with downside risks growing. With a better-than-expected third-quarter GDP outcome, we have revised up 2023 GDP from 1.1% year-on-year to 1.2% and 2024 GDP from 1.7% to 1.8%.

BoK watch

Supported by solid growth results, the Bank of Korea will continue to focus on curbing inflation and containing rising household debt in the coming months. The BoK commented that it could consider raising policy rates if household debt continues to increase excessively, but we still believe another rate hike is highly unlikely, especially at a time when the growth outlook has become grimmer than in the past due to growing geopolitical risks. The government has also tightened conditions on policy mortgages, and we will likely see some stabilisation of household debt growth from the end of this year. Depending on inflation and debt conditions, there is a growing possibility that the first rate cut could be delayed by a quarter or so to the third quarter, but for now, we keep our first rate cut call in the second quarter of next year as it is.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap