- Quick take

- 1 October 2021

- Japan

Japan’s Tankan business survey beats consensus

The Bank Of Japan's September Tankan survey of business conditions was a rare piece of positive newsflow from Japan - though there remain big differences between manufacturing and non-manufacturing firms

| 18 |

Large Manufacturing3Q Index |

| Higher than expected | |

Large manufacturing firms beat expectations

It looks as if, contrary to expectations, large manufacturing firms had a reasonable third quarter. The Tankan index for such firms registered 18, up from 14 in the second quarter, and beating expectations for a slight decline to 13.

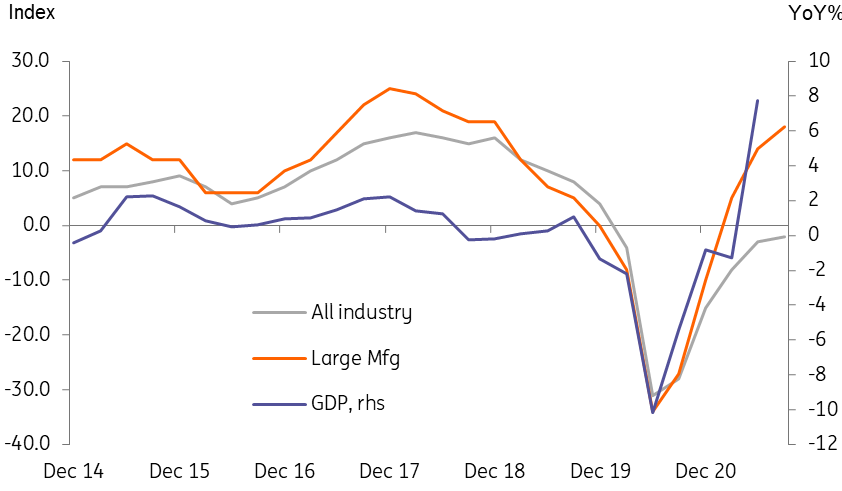

Like most diffusion indices, care is needed in interpreting these figures. But what this latest set of data tells us is that large manufacturing firms continued to grow in 3Q21, and apparently at a slightly faster pace than in 2Q21.

The importance of the Tankan survey is partly a legacy of historically volatile and sometimes not totally credible swings in Japanese GDP figures. The Tankan was traditionally a steadier indicator of broad economic trends. Given the impact of Covid on GDP figures around the world, which have alternately plunged then soared, the latest Tankan survey provides a steadier assessment of economic momentum and suggests that the economy continued to make progress in 3Q. If so, then that is not a bad outcome taking into account all the talk about supply chain disruption in Asia that has been floating around. But if we can believe the Tankan outlook figures (probably need to take with a pinch of salt as not hugely reliable), then businesses expect next quarter growth to ease back a bit. Perhaps those supply chain disruptions are expected to start biting harder in the coming months.

Tankan headline indices and GDP

It's not all good

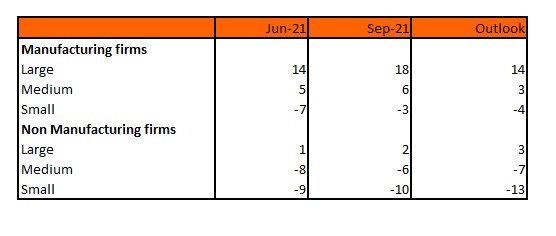

As is often the case, the Tankan survey's large manufacturing headline index doesn't tell the full story. Non-manufacturing firms' sentiment remained stuck at 2, consistent with only very slow growth, and was expected to fall back to only 1 next quarter. Conditions were worse for small firms, though especially for small non-manufacturing firms. This may reflect the impact of social movement restrictions imposed during 3Q21 to combat the Covid pandemic - these will have had a much greater negative impact on small service sector firms, in the leisure, and hospitality sectors in particular. The outlook for small firms in both manufacturing and non-manufacturing industries was for conditions to worsen next quarter.

Moreover, if you follow the link to the Official Tankan release, and scroll down to look at the supply/ demand section, you can see that indices for both input prices and output prices rose substantially - a further bit of evidence for those who are calling stagflation. So all is not quite as rosy as the headline indices suggest.

Tankan main indices

Data could provide some JPY support

Today's data comes against the backdrop of a strengthening USD, and worsening market sentiment, but where the JPY has been until recently been losing out to the USD on real interest rate comparisons. The last 24 hours has seen the JPY strengthen again, and it seems as if risk sentiment is now back in the driving seat for currencies. Today's better Tankan data may help to push in the same direction that markets seem to want to go anyway.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more