- Quick take

- 22 October 2025

- Rates China Japan

Japanese exports recovered in September despite US tariff hit

Japanese exports recovered mostly in line with market expectations. We cautiously expect US-bound exports to stabilise after the recent trade deal. Stronger-than-expected imports indicate continued investment in AI and semiconductors, supporting growth in the fourth quarter

| 4.2% |

Exports%YoY |

| Lower than expected | |

Japanese exports rebounded to 4.2% YoY in September (-0.1% in Aug, 4.4% market consensus)

The US tariffs negatively affected exports to the US, but shipments elsewhere stayed strong, highlighting Japan's export resilience.

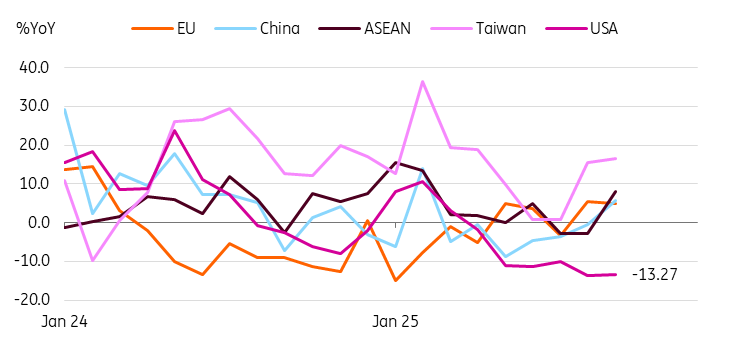

By destination, exports to the US dropped 13.3% year-on-year, while exports to Asia (9.2%), China (5.8%), and the EU (5.0%) posted solid gains. Strong export performance to Asia, particularly to Hong Kong, Malaysia, Taiwan, and Vietnam, is related to IT exports as they are top global hubs.

Examining US exports in greater detail, the tariff has resulted in decreases across all export categories: chemicals (-17.8%), iron and steel (-34.7%), machinery (-8.7%), electrical machinery (-3.7%), and transport equipment (-19.2%).

We found that exports of machinery, electrical machinery, and transport equipment to the EU, Asia, and China were quite strong, but exports of iron and steel showed a decline across the globe. Overall, trade in iron and steel was hit by spreading tariffs from the US to the EU, sluggish construction activity, and severe price competition.

Meanwhile, the overall weakness in vehicle exports (0.6%) was mainly due to weak US exports, while semiconductor booms continued to support Japanese chipmakers.

Weak exports to the US continued while others rebounded

Imports rose 3.3% YoY in September (vs -5.2% in August, 0.6% market consensus)

Mineral fuel prices fell 14.4% due to lower global commodity prices, indicating possible domestic energy price reductions. Meanwhile, machinery and electrical machinery imports rose 13.8% and 9.9% respectively. This will translate into an increase in capital investment in the coming months. As imports grew faster than exports, the trade balance recorded a JPY 234.6 billion deficit.

BoJ watch

Today’s trade data was overall positive for growth. The weakness of US exports was more than offset by strong demand from the rest of the world. We cautiously expect the gradual normalisation of exports to the US in the near term. We continue to believe that the Japanese economy will stay on the recovery path. Also, this should support additional Bank of Japan rate hikes, although the pace might slow a bit due to several lingering uncertainty factors.

When it comes to the BoJ's decision, markets widely expect the central bank to pause at its October meeting and resume its hike in December. But we still believe an October hike remains a possibility. If the BoJ stays pat in October, but shows a 2-7 split vote and any upward revisions on growth and inflation, market sentiment could shift rapidly before the December meeting. Going forward, comments from the new Prime Minister Takaichi, changes in USDJPY, and inflation data should be monitored to assess potential timing for the BoJ’s rate decision.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more