- Quick take

- 6 March

- Romania

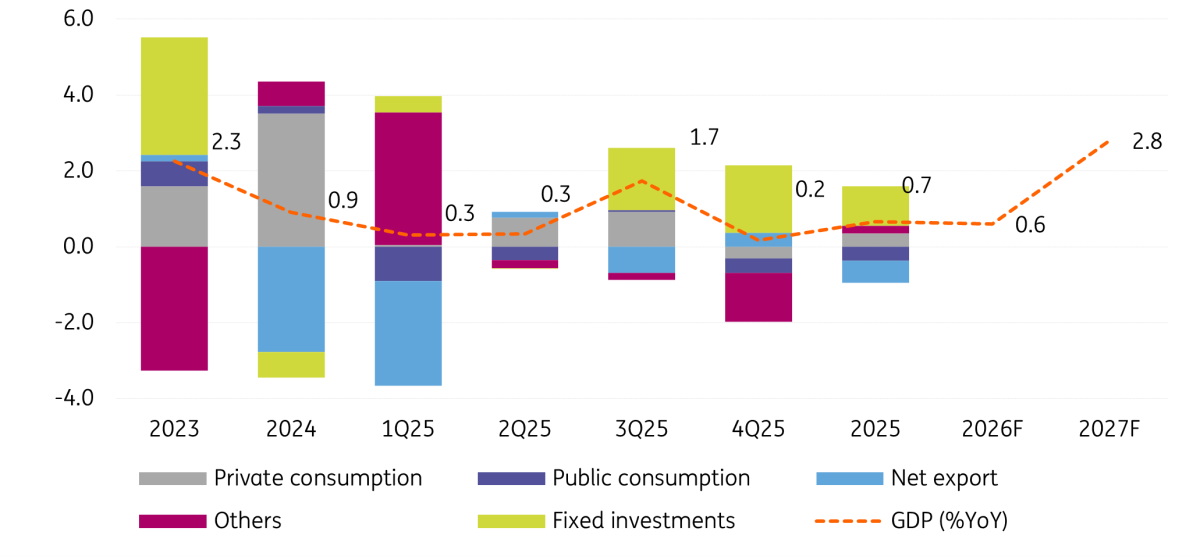

Investments take centre stage in Romanian GDP growth

Today’s confirmation of the significantly weaker-than-expected fourth-quarter GDP underscores the continued strain on private consumption, contrasted by a solid performance in investments. We maintain our 2026 GDP growth forecast of 0.6%, while acknowledging rising risks of delays to interest rate cuts

What the latest data shows

In the fourth quarter of 2025, GDP contracted by 1.9% quarter‑on‑quarter, while showing a modest 0.2% expansion compared with the same period in 2024. On the demand side, private and public consumption were the main drags, jointly reducing annual GDP growth by 0.7pp. As expected, investment provided a strong offset, contributing 1.8pp and helping to stabilise overall activity. The decline in consumption also kept net exports in positive territory. Meanwhile, inventory changes were a significant negative factor, subtracting 1.3pp from growth.

For the full year 2025, private consumption added only a modest 0.3pp to growth, a historically low value, given the long-term average contribution of around 3-4%. Investments added a solid 1.0pp contribution to growth for the whole year. On the other hand, public consumption and net exports subtracted a total of 1.0pp from growth.

GDP growth (%) and contributions (ppts)

On the supply side, construction activity remained the standout performer in late 2025, contributing 0.7pp to growth (following 0.8pp in 3Q25). The information and communication sector also recorded solid momentum, adding 0.5pp. In contrast, wholesale and retail trade, along with professional services, were the main negative contributors, jointly subtracting 0.7pp from annual growth.

Overall, one small positive in an otherwise subdued growth picture is the upward revision of full-year 2025 GDP from 0.6% to 0.7%. After 2024’s modest 0.9%, these low growth rates underscore the limitations of Romania’s long-standing consumption-driven economic model. The current adjustment phase reflects a rebalancing toward investment-led growth, which should begin to support Romania’s productive capacity.

The outlook and what’s ahead for policy decisions

In principle, today’s confirmation of a very weak Q4 result strengthens the case for earlier monetary policy easing to support growth. Another soft quarter – this time 1Q26 – would reinforce this position further. We have long expected the National Bank of Romania (NBR) to begin its cutting cycle in May, delivering 100bp in total cuts throughout 2026. This view was based on the widening negative output gap and the risk of monetary policy lagging behind economic momentum.

However, rising geopolitical tensions in the Middle East and their implications for inflation, risk sentiment, and capital flows introduce significant risks of delayed rate cuts. The likelihood has now increased for a later start and a shorter easing cycle. Under this alternative scenario, we would expect the first cut in August, with total cuts reduced to 75bp for 2026. An August move would also align with the publication of the August Inflation Report, allowing room for updated guidance and projections.

On the growth side, we continue to expect the economy to expand by 0.6% in 2026 and 2.8% in 2027, though short-term downside risks are becoming more pronounced.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more