- Quick take

Industry and retail sales move in opposite directions in Hungary

- 5 November 2021

- Hungary

The bad news first: industry has been unable to shake off the negative impact of shortages. However, retail sales have provided a silver lining with a better-than-expected performance in September

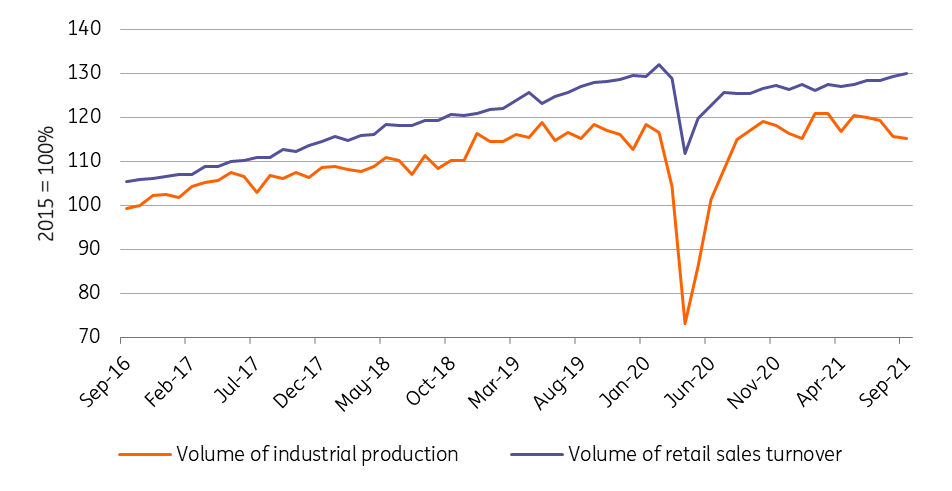

The latest set of data on industry and retail sales present a mixed picture, as the two sectors are trending in opposite directions. Retail sales showed a significant upside surprise in September, meaning we are now looking at a series of good numbers. Industry, on the other hand, was a huge disappointment, showing a trajectory of declining output.

Fixed based volume indices of Hungarian industry and retail sales

Industry

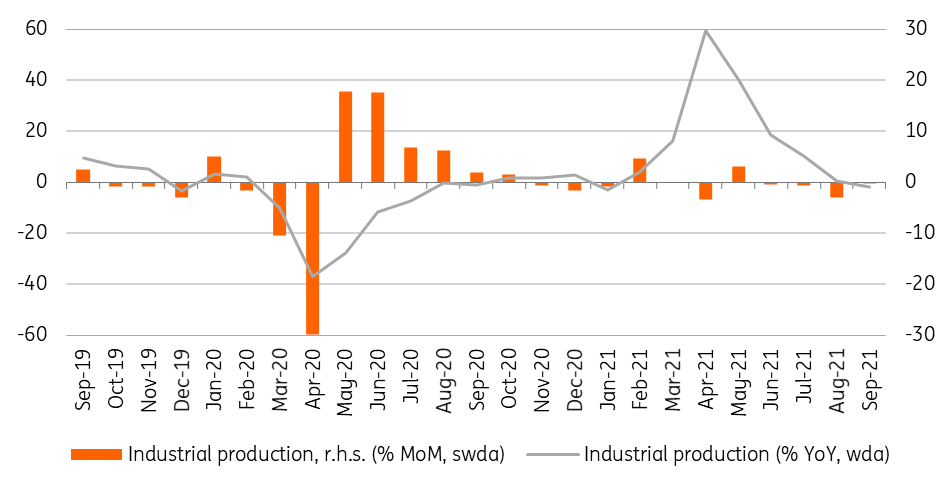

Industry has fallen far short of expectations. We expected a rebound after an extremely weak performance in August, burdened by longer-than-usual summer shutdowns, but Hungarian manufacturing has disappointed. This is mostly due to the fact that despite the already low level of output in August, September brought another decline: a 0.3% month-on-month decrease in volumes. In parallel, the yearly-based performance also showed a drop, of 1.7%, based on working-day adjusted data.

Performance of Hungarian industry

The press release from the Statistical Office revealed that growth was measured in most manufacturing sub-sectors, while output was on the decline in car and electronics manufacturing. A strong performance in sectors with a smaller weight in total industrial production is not too helpful if the two biggest ones are performing poorly. The obvious reason behind the drop in output in the car and electronics sectors is the global shortage of semiconductors and other spare parts, accompanied by delays in shipping problems.

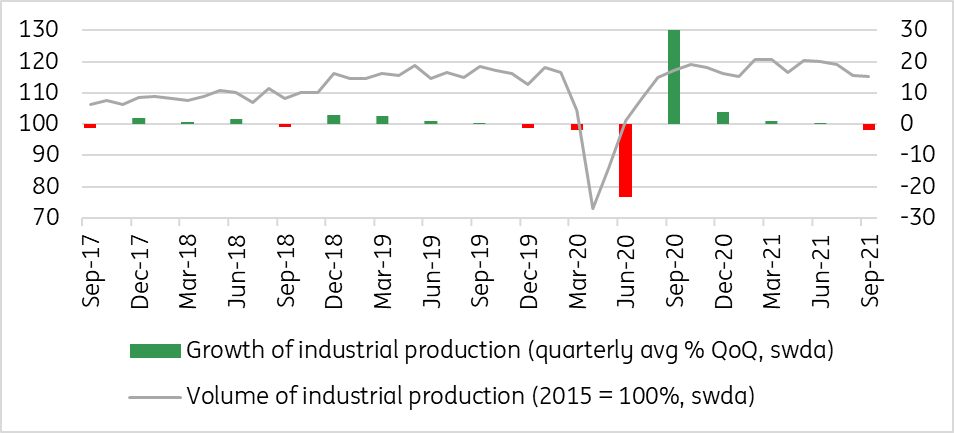

Based on the fixed base volume index of industrial production, the overall performance in the third quarter is bad. Compared to the previous quarter, the volume of production decreased by almost 2%. On an annual basis – due to the low base – third quarter output is still nearly 3% higher. The combination of transportation problems, spare parts sourcing difficulties and labour shortages has already been an effective constraint on production in the third quarter of 2021.

Production level and quarterly performance of industry

Looking ahead, these problems will remain with us going into 2022, thus the fourth quarter also carries serious downside risks to economic activity, mainly due to net export developments. After all, the lack of export activity is accompanied by strong import demand driven by consumption and investment, which thus curbs GDP growth. However, there is a silver lining, provided by retail sales.

Retail sales

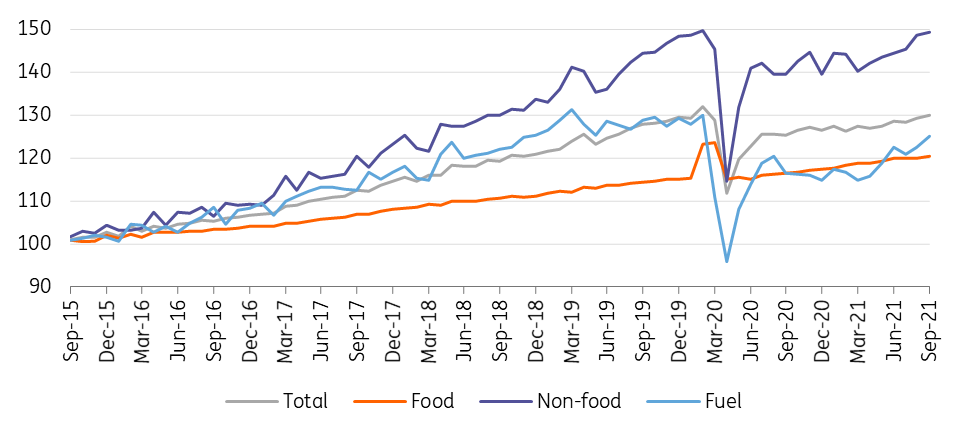

In contrast with industry, retail sales surprised to the upside during the third quarter. The volume of turnover was up by 5.8% year-on-year in September, while the consensus was for a more moderate expansion. Another positive development is that the expansion was not only due to the low base, as the sector also showed substantial month-on-month growth of 0.6%. Today’s data also means that retail is starting to put together a series of good numbers, trending up since spring 2021. Moreover, in recent months the trend growth has been steeper, approaching pre-Covid dynamics.

Retail sales volume in details (2015 = 100%)

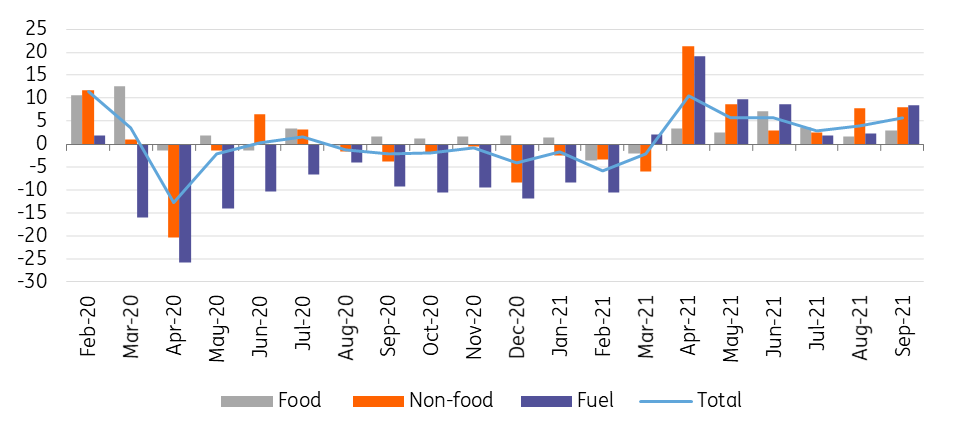

The favourable performance in September is mainly due to the significant (2.1% MoM) increase in fuel retailing. With the end of the summer holidays and the start of in-person schooling, road traffic also increased significantly. In addition, non-food retail sales performed well again after a strong August, posting growth of around 8% on a yearly basis. Demand for clothing products expanded significantly, but presumably due to rising inflation, the turnover of second-hand shops also showed double-digit growth. As for food retailing, we do not see any significant changes compared to the trends observed earlier. On an annual basis, growth was 3%.

Breakdown of retail sales (% YoY, wda)

The good performance in the last two months is certainly encouraging in terms of third quarter GDP growth. We calculate that retail sales rose by 1.2% quarter-on-quarter. Given that the summer months tend to be much stronger in services than in retail, we can expect a significant contribution to economic activity via consumption. This positive surprise is mostly a counterbalance to the negative developments in industry. So looking at today’s retail and industry data, we maintain our expectation that the Hungarian economy will continue to grow in 3Q21. We forecast a 1% QoQ increase with some upside risks mainly stemming from investment activity. When it comes to 2021 as a whole, we forecast 7.7% YoY GDP growth.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more