- Quick take

- 5 February 2021

- Indonesia

Indonesia’s economy shrinks as mobility restrictions weigh on consumption

As Indonesia records its first annual contraction since the 1998 Asian financial crisis, the path to more easing remains wide open with the rupiah stability the likely determinant for the timing of the next rate cut

| -2.2% |

4Q GDP |

| Better than expected | |

Indonesia records first annual contraction since the 1998 Asian financial crisis

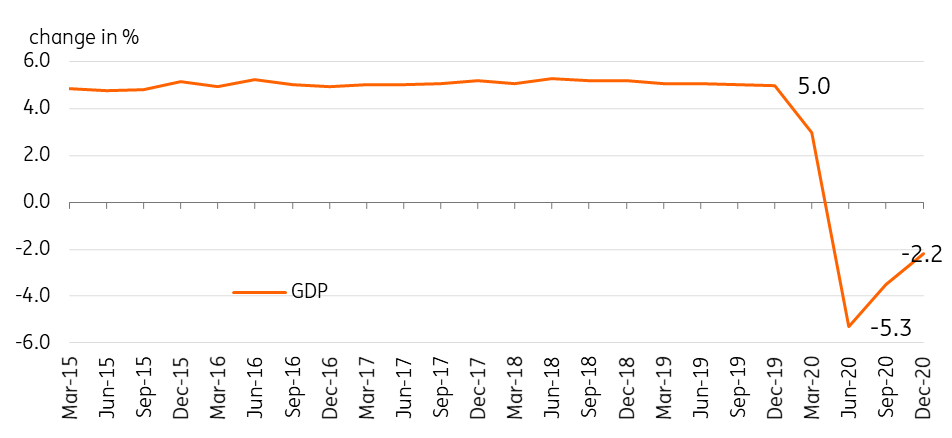

Indonesia’s economy contracted by 2.2% in the fourth quarter while 2020 full-year GDP is down by 2.1%.

Household consumption, which accounts for the bulk of economic activity, fell by 3.6% with retail sales in freefall, declining for the eleventh consecutive month. Anaemic consumption has manifested in below-target inflation and we expect these trends to continue with both Java and Bali under partial mobility restrictions to contain the virus.

Capital formation and exports were also down in 4Q, falling by 6.2% and 7.2%, respectively with only government spending positing gains for the quarter (1.8%). We expect GDP to remain in contraction 1Q21 after several natural calamities hit the country.

Indonesian GDP

Central bank on hold for now but open for further easing

Authorities remain hopeful for a recovery in 2021 but recognise the fresh set of challenges this year.

Although Covid-19 vaccinations have started, new infections remain elevated (11,434 recorded on 4 February) while the bulk of vaccine supply is set to arrive in the coming months. Finance minister Sri Mulyani Indrawati announced an increase in fiscal support to offset the slowing momentum, increasing the budget to IDR 619 trillion from IDR 533 trillion with the government moving to support the health care sector and business.

Meanwhile, the central bank Governor Perry Warjiyo vowed to keep monetary policy accommodative given benign inflation and we expect to see easing policy rates further with IDR stability the likely determinant for the timing of the next policy rate cut.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more