- Quick take

India: GDP growth accelerates in 2Q23

- 1 September 2023

- India

At 7.8% YoY, India's GDP print for 2Q23 was precisely in line with the consensus expectation but nonetheless, singles out India as one of the few economies in the region where growth is actually firming, not declining. Total calendar-year growth of 7% or close is within reach

| 7.8% |

2Q23 GDP YoY%Up from 6.1% |

| As expected | |

No surprise, but it's still a good result

The consensus forecast seems to have correctly decided to trust in some of the NowCasts circulating, which also pointed to a 7.8% growth rate. But although the number was correctly anticipated, this doesn't reduce just what a good figure this is.

Across the region, the combination of China's faltering economy, along with the lingering impacts of the semiconductor downcycle, is keeping growth subdued, and in some cases, actually weakening. Not so in India, where growth remains very firm. Part of that is clearly due to the very limited direct exposure to trade with China - the legacy of decades of political tensions. India is also not as exposed to the semiconductor industry as some other economies in the region, though this is slowly changing as supply chains are shifted around the region. At least for now, that has provided some insulation for India against some of the headwinds being faced by other Asian economies.

Where's the growth coming from

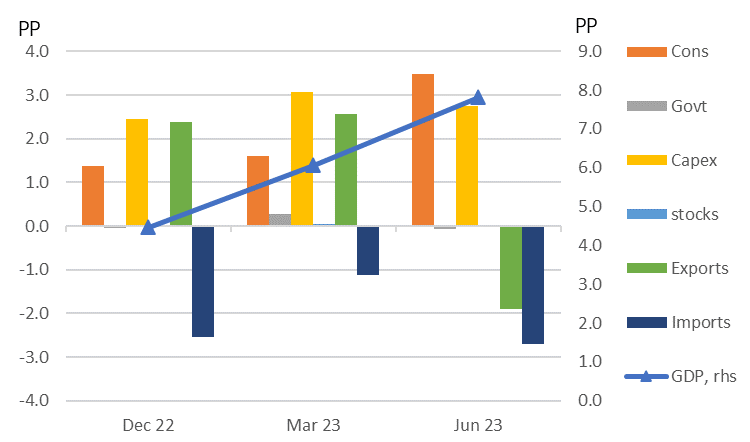

Despite what was a fairly generous Union Budget this year, with only a modest reduction in the deficit target to 5.9% of GDP in fiscal 2023/24 from 6.4% in fiscal 2022/23, government spending is doing none of the direct heavy lifting at the moment. That said, behind the scenes, government capex and infrastructure development is almost certainly helping to draw in private investment growth. Capital investment contributed 2.8 percentage points of the 7.8% GDP growth total - another solid contribution after the 3.1pp contribution in 1Q23.

The other big contributor remained consumer spending. This too has been consistently strong, but has more than doubled its contribution this quarter to 3.5pp, up from 1.6pp in 1Q23.

The only blot on the ledger was from net exports, which were a substantial drag on growth this quarter, though this has not shown up in terms of a large inventory build, which often happens, so that doesn't necessarily imply any ominous unwinding of stock build-ups in the coming quarters. There was, however, also a fairly chunky swing in the "discrepancies" part of GDP, which is a residual term to account for GDP not picked up in the other main areas. This may well end up being reclassified into stocks at some point, so we aren't ruling out a future stock correction just yet.

Contributions to YoY% GDP growth (pp)

Production measures also looking promising

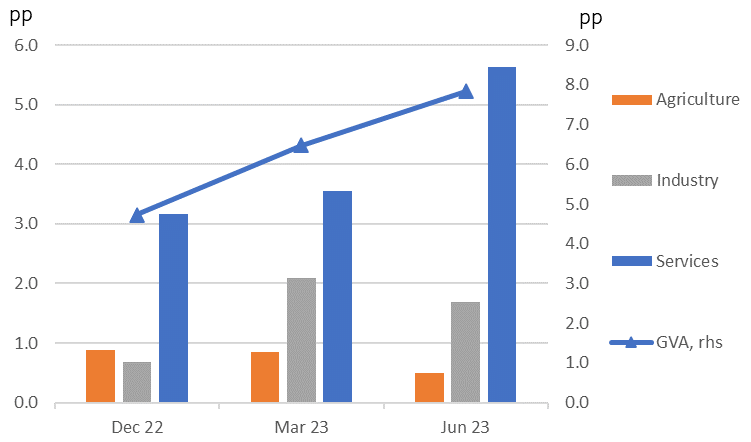

GDP, or more precisely GVA (gross value added) measured in terms of industrial sector production, is also with a quick look.

Here, we see that the main engine for growth is not industry, which has slowed a little, but the service sector. And that ties in with the consumer spending observation we made earlier. Agriculture contributed a little less this quarter - perhaps reflecting the erratic monsoons we have seen this year.

GVA by sector (contribution to growth pp)

RBI easing not a priority

Putting all of this together, it looks like the Reserve Bank of India (RBI) will be in no hurry to cut rates. Growth is clearly very strong and it looks like it will remain so in the quarters ahead. A growth rate of about 7% for the full calendar year looks probable, and something in the 6-7% range for next year is also looking likely.

The recent upward spike in inflation is, for now, almost entirely food price-driven, and there are already signs that the worst increases in tomatoes and onions are behind us, so there is equally little need for the RBI to tighten rates in response to this growth backdrop. The 6.5% policy rate will already look quite restrictive once the inflation numbers settle down again, which we believe they will do soon. Rate cuts are most likely the next direction for the RBI, but these can wait until next year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more