- Quick take

- 10 February 2023

- Hungary

Hungary’s inflation likely peaked in January

Inflation accelerated to new highs at the start of 2023, but it is very likely that January marked the peak. The lifting of the fuel price cap, along with food and services price increases were the main drivers

| 25.7% |

Headline inflation (YoY)ING estimate 25.5% / Consensus 25.2% / Previous 24.5% |

| Higher than expected | |

Once again, the motor fuel component stole the show

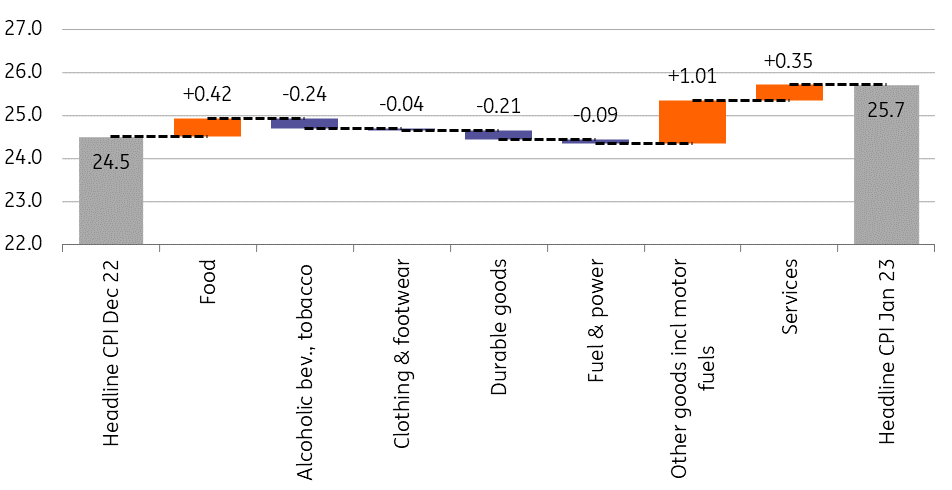

Inflation in Hungary accelerated further pushing both headline and core inflation to the highest level in 27 years. The market consensus was exceeded as headline inflation registered a 25.7% year-on-year (YoY) increase, which is the result of a 2.3% monthly acceleration. The upside surprise was not just fuelled by the price changes, but also by the usual start-of-the-year re-weighting of the consumer basket. Food and other goods (including motor fuel) got a bump in their share of the basket, resulting in a higher contribution of these items in the headline inflation.

Main drivers of the change in headline CPI (%)

The details

- The motor fuel component was the biggest contributor to this month’s acceleration in inflation. As we highlighted in our latest piece, due to methodological technicalities, the entire effect of fuel price lifting was not reflected in December’s inflation figure. In fact, part of the effect spilt over to January, explaining 1.0ppt from the 1.2ppt increase in the headline number from December to January. In the absence of external energy shocks over the coming months, the price of motor fuel should moderate – as we have already seen in prices at the pump, thus this could be a drag on inflation.

- Food prices posted a surprising 44.0% YoY increase, which in fact translates to good news given the 44.8% yearly increase registered back in December. While processed food prices posted a 2.4% monthly increase, the price of unprocessed food accelerated by 3.1% month-on-month, according to NBH’s calculations. All items in the food basket posted price increases, except for eggs which are under price caps, boosting the headline number by 0.4ppt from December. We believe that the effect of intense re-pricings at the start of the year will fade in the following months. Anecdotal evidence shows that retailers are facing a demand crunch, translating into selective price cuts. However, as long as price caps are in effect on a sub-sample of foods, we might have to wait to see a significant decline in prices in general.

- Services prices jumped to 11.3% YoY, which explains 0.35ppt of the acceleration in headline inflation. The higher-than-expected 2.4% monthly increase is likely a response to energy and labour cost shocks, which resulted in stronger repricing at the beginning of the year. This resonates well with the NBH’s own so-called market services inflation, which moved to 2.3% in January, putting the start-of-the-year repricing at an extreme level as history shows around a 0.3-0.6% monthly price increase in the first month of the year.

- As for the fuel and power component, prices fell for the second time in a row. This item contains household energy as well. The decrease in prices is likely due to the combination of more conscious energy consumption and milder-than-expected winter weather, resulting in lower overhead costs for households.

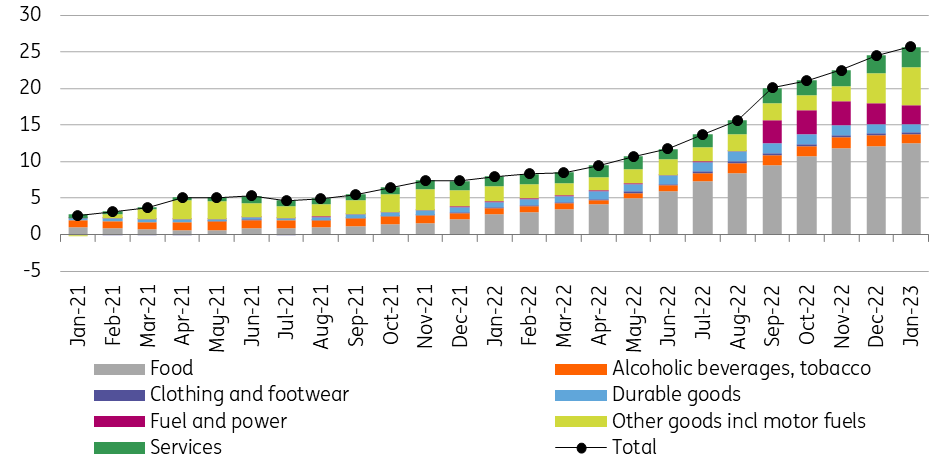

The composition of headline inflation (ppt)

Headline inflation outstrips core inflation

Core inflation accelerated to 25.4% year-on-year, remaining below the headline number for the first time since February 2022. As core inflation posted a 1.8% MoM increase, there are clear signs that the underlying price pressures remained strong. The monthly increase is largely due to an acceleration in processed food and services prices, which could not be counterbalanced by a slight decrease in durable goods prices. According to our estimates, more than 56% of the items in the consumer basket already showed at least a 20% YoY inflation figure in January.

Headline and underlying inflation measures (% YoY)

January likely marked the top

In light of today’s higher-than-expected reading, we believe that it is very likely that inflation peaked in January. As the effect of lifting the fuel price cap was fully accounted for in the last two readings and prices have started to decline based on pump prices, we expect that price pressures for this component in the future will be markedly contained. Food and consumer durables prices should follow suit as the forint’s recent strength should help to tame imported inflation, while a drop in household demand is reducing the pricing power of retailers. Moreover, household energy could also prove to be a drag on inflation with a further reduction of energy consumption. The caveat, however, comes from market services. We expect further price increases in the services sector, so despite the above-mentioned drags, this could be a significant counterforce. In all, the year-on-year inflation rate will most likely show small drops (or go sideways at worst) in the coming months. A more serious deceleration is likely to take place from April onwards as base effects should also help the index to fall substantially. For this year, we expect average inflation of 18.5%, with year-end figures dipping into high single-digit territory. However, the real challenge comes in 2024 when it comes to further deceleration.

Upside risks still can't be ruled out

The main reason for this is that the risk of persistently high inflation has not been averted. In our view, the dynamic wage growth could translate into positive real wage growth in the second half of the year, which could support the economic rebound from a technical recession. However, at the same time, companies could regain their price-setting power, which in turn can trigger further repricing as the wage-price spiral intensifies. Against this backdrop, we believe that monetary policymakers will continue to be patient, monitoring recent developments and sit on their hands during the first quarter and possibly even in the early second quarter before a dovish pivot starts.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more