- Quick take

Hungary’s economy wraps up a muted first half

- 30 July 2025

- Hungary

Flash GDP data for the second quarter shows yet another stretch of stagnant growth, underscoring the subdued performance so far in 2025. Although we anticipate a slight improvement in the coming quarters, we have downgraded our GDP growth outlook for 2025 to 0.7%

| 0.4% |

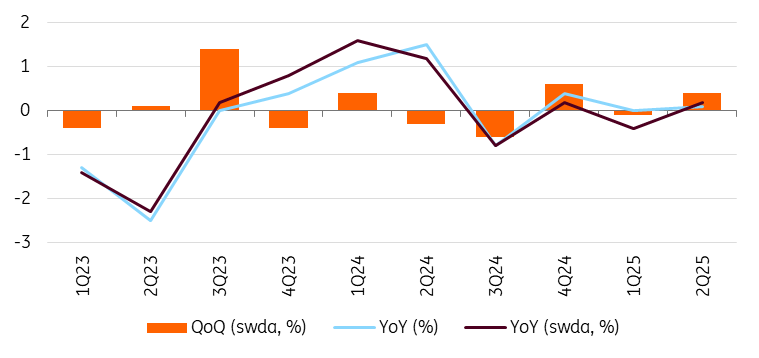

GDP growth in Q2 (QoQ, swda)ING forecast 0.1% / Previous -0.1% |

| Better than expected | |

Ahead of the latest GDP release, both the Ministry for National Economy and the National Bank of Hungary reiterated their forecasts of stagnation based on nowcast estimates. As a result, the Statistical Office’s report - showing just 0.1% year-on-year growth in 2Q - generated little reaction. The quarterly performance of the economy, showing 0.4% QoQ growth, is more of a positive surprise. This figure means that another technical recession has been avoided, though this is little consolation given the economy's overall performance so far this year.

Compared to expectations at the end of last year, GDP growth in 2025 has been disappointing. Based on raw data, the first half of the year brought stagnation; however, the seasonally adjusted data indicates a slight decline in January-June compared to the same period in the previous year.

Hungarian GDP growth

The Hungarian Central Statistical Office provided few details about the underlying drivers in its flash reports, as is usually the case. However, the information we obtained from the current report is consistent with what could be inferred from preliminary sectoral data. Agriculture and industry performed poorly on an annual basis, significantly dampening the economy's performance. The weather was unkind to agriculture this year, with late frost and drought. In addition to crop production, livestock farming had a poor first half of the year due to bird flu and foot-and-mouth disease outbreaks. Industry continues to be held back by a lack of external demand and the failure of the expected turnaround in the inventory cycle.

Surprisingly, the HCSO didn’t list the construction industry as one of the positive performers, despite the sector's strong performance in April and May. Therefore, it is quite possible that either June was a weak month for the construction industry, resulting in a low contribution to GDP, or the value added of the sector was much lower than the production data suggested. While the service sector's role in driving economic growth is perhaps less surprising, the information and communication sector's dominance – highlighted by the data release – is more surprising. In the case of services, we estimated that growth would be driven primarily by household-related services (including tourism), while corporate-driven services would be dominated by savings and cost-cutting measures. Of course, this may still prove to be true, but only the detailed data release on 2 September will provide clarity.

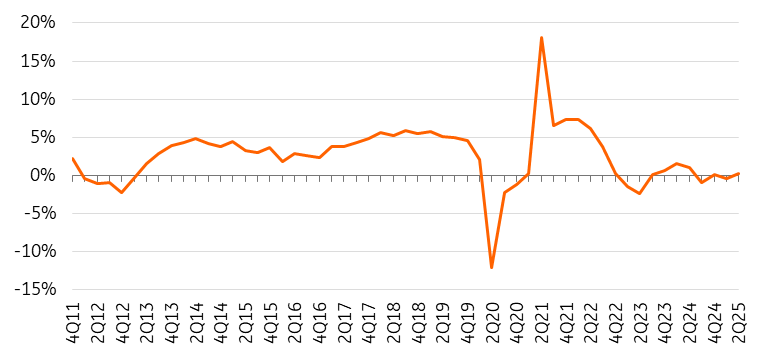

The quarterly annualised growth rate of Hungarian real GDP

On the final use side, we think consumption has been the driving force of GDP. However, the performance of investment activity and net exports probably counterbalanced it, pulling back the economy’s overall performance to near stagnation.

Regarding the expected GDP growth for this entire year, second-quarter data was slightly better than our expectations. However, this remains too marginal to support expectations of Hungary’s GDP significantly exceeding 1% growth this year.

In our view, GDP growth will most likely be between 0.5 and 1.0% in 2025. Taking today's data into account, our estimate sits at 0.7%, down from 1% previously. Consumption will likely remain the driving force until the end of this year, primarily due to incoming fiscal measures (tax reduction, housing program, higher family allowance, etc). The biggest question is how much of the resulting extra disposable income will be spent and how much will be saved. Based on consumer confidence, we think that the propensity to save will remain elevated. We do not expect a major turnaround in investment activity trends, so it will certainly be a strong negative contributor for the year. In the case of net exports, strong import demand from consumption and the general weakness of external demand do not signal a significant positive change by the end of the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more