- Quick take

- 5 August 2020

- Hungary

Hungarian retail turnover back at last year’s level

Even though June wasn't affected by the lockdown, Hungarian retail sales show only a gradual rebound. The historic collapse in 2Q points to a double-digit GDP drop

| -0.1% |

Retail sales (YoY, wda)Consensus 0.6% / Previous -2.0% |

| Worse than expected | |

Hungarian retail sales have been normalising since the April nadir, but they are nowhere near a sudden turnaround.

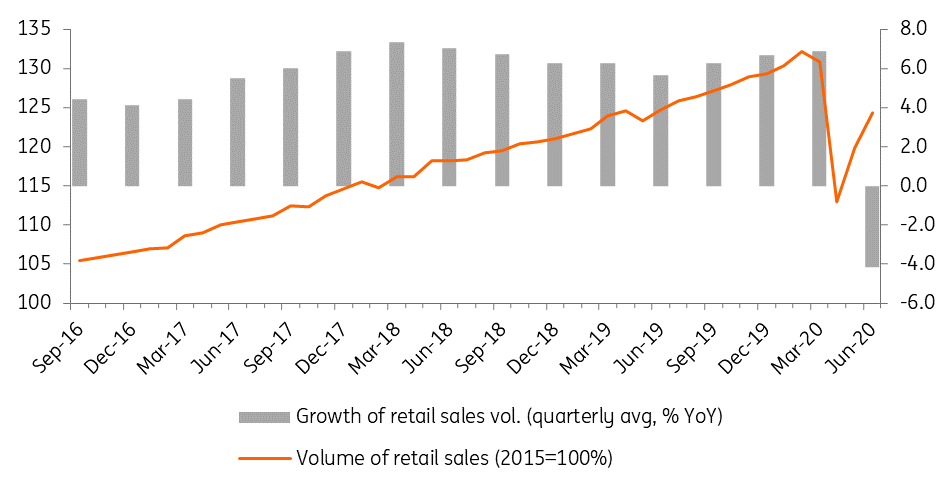

The seasonally adjusted volume of retail sales increased by around 3.7% on a monthly basis. In year-on-year terms, the sector’s turnover is still down by 0.1% based on working-day adjusted data. In April 2020, the level of retail sales equalled the level last seen in 2017. By May, the level of mid-2018 had been reached and in June, retail sales volume was roughly back to last year’s level.

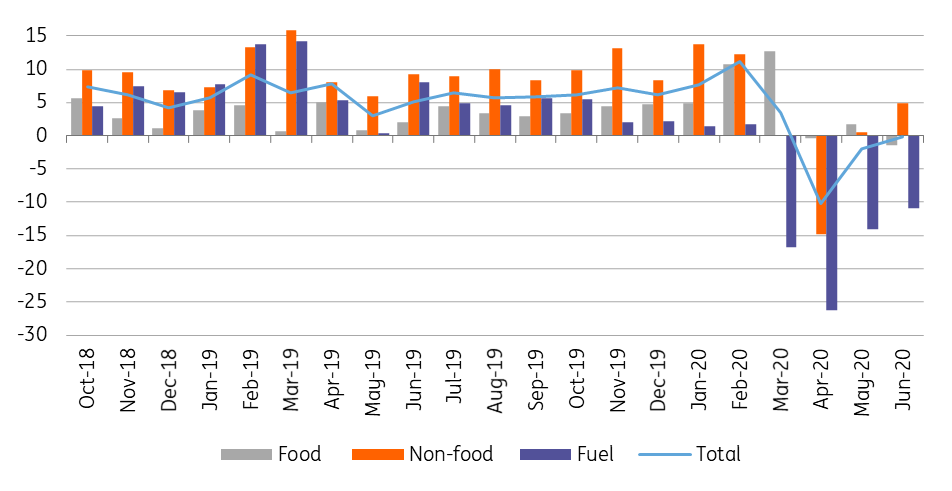

The details show only the non-food segment was able to grow in June on a yearly basis. Although the 4.9% YoY increase is only half the average growth rate measured in the past three years. Demand was strongly increasing in manufactured goods, books, computers, furniture and electrical goods. As the Covid-19 panic eased, turnover in medical goods fell. Turnover in food shops was down by 1.5% YoY in June. This partially reflects the significant price increase in fruit and vegetables, which curbs demand.

It hardly comes as a surprise that the most affected retail segment is still fuel sales. Demand for fuel decreased by 11.3% on a yearly basis as people were still commuting less.

Breakdown of retail sales (% YoY, wda)

In the summer months, we expect moderate improvement in retail sales. However, the run-off of short-term labour market subsidies could impact the disposable income in a negative manner from the autumn. By then, the pent-up demand will also become much weaker. All in all, we see only mild growth in retail sales in 2020 as a whole.

Retail sales volume and quarterly performance

In terms of GDP outlook, retail sales fell by 4.2% YoY in 2Q20, triggered by a decline of more than 9% on a quarterly basis. This has been the sharpest fall ever - nearly double the recent record seen in 3Q09.

In that quarter, GDP nosedived by 7.5% year-on-year. Against this backdrop, it is easy to imagine that the gross domestic product in 2Q20 might decrease by more than our 10.5% YoY forecast.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more