- Quick take

Hungarian retail sales and industrial production surprise on the upside

- 6 May 2021

- Hungary

Both retail sales and industrial production in Hungary caused an upside surprise as we reach one year of lockdowns. Although, this bodes well for the big picture, we're still likely to see a drop in GDP on a quarterly basis

Hungarian retail sales improved in March 2021, outperforming market expectations despite the lockdown measures.

Retail sales turnover rose by 0.8% on a monthly basis and thanks to the buying frenzy last March before the lockdowns, the base was relatively high. This translated into a 2% YoY volume drop in retail sales (working-day adjusted). So, the weak year-on-year performance can be seen as a technical glitch; however, this is still in contrast with the significantly improving labour market metrics.

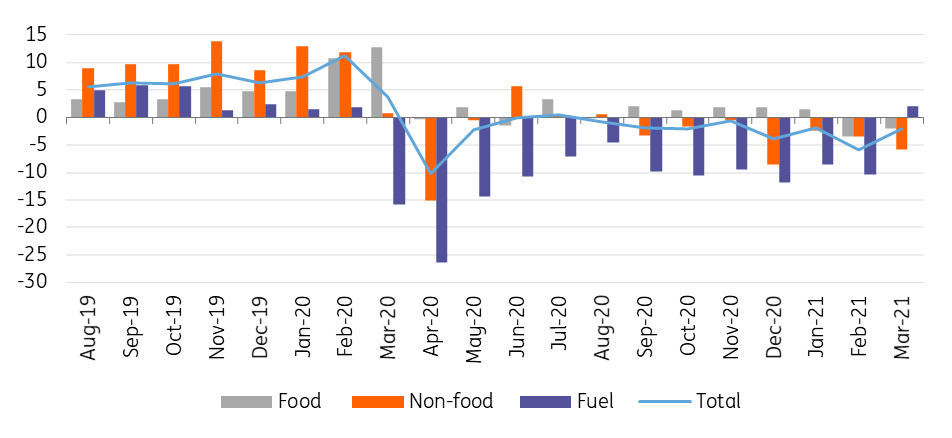

Breakdown of retail sales (% YoY, wda)

Within the main subsectors, fuel sales caused the most critical upside surprise.

Despite the sheer number of people working from home, given that last year’s base was so low, fuel sales grew by 2.1% on a yearly basis. The food retail sector showed a 2% YoY drop due to the high base effect, while non-food retail continues to suffer as people are still holding back significant spending.

On a yearly basis, retail sales turnover decreased by 5.9% in such shops. Clothing and furniture shops are among the worst performers with close to a 50% drop on a yearly basis.

Like retail sales, industrial production also caused an upside surprise in March.

Despite the new round of lockdown measures, which were problematic from a labour force point of view for manufacturers, industrial production grew by 0.4% on a monthly basis. This increase in production comes in contrast with the grumblings of car manufacturers due to input shortages.

Due to the low base effect caused by the temporary shutdowns last March, the year-on-year performance jumped to a record high of 16.2% based on calendar-adjusted data.

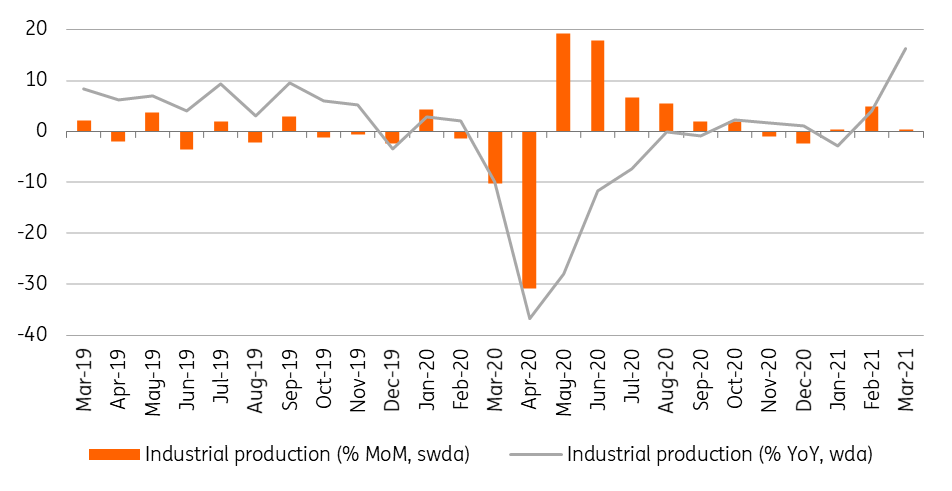

Performance of Hungarian industry

When it comes to the details, the Statistical Office highlighted that car manufacturing was the main driver behind the good performance due to base effects. In the meantime, the other two major segments, the electronics and food industry displayed below-average growth in March. But the real good news here is that all of the subsectors were able to increase the production levels on a yearly basis.

Although the March figures in industry provide some comfort, one carmaker in Hungary went through a temporary shutdown in April because of semiconductor shortages. So, industry is still facing significant hurdles going forward, but we expect the sector to be a positive contributor to GDP growth during the year.

When it comes to the outlook of retail sales, reopening will probably push people to spend more. However, this money will be rather spent on experiences rather than stuff. This means that the positive impact of reopening might not show up in retail sales statistics for a while.

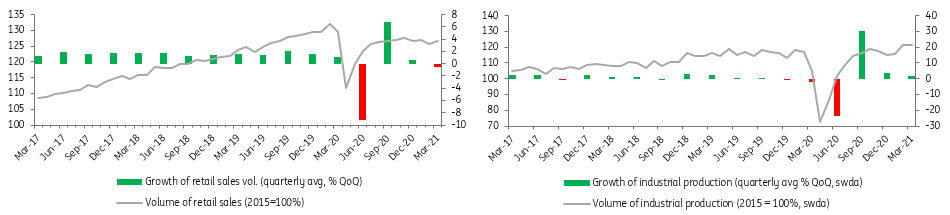

Quarterly performance of retail sales and industry

As we are approaching the release date of 1Q21 GDP data, it might be worth talking about the past.

Industry was able to grow during the first quarter, whether it is a quarterly or a yearly comparison, which gives some hope for a better-than-expected outcome. On the other side, however, retail sales shrank both on a quarterly and a yearly basis during January–March. With services being practically shut down, this could mean that consumption remained a significant drag on growth.

All things considered, we stick to our call of a 1% QoQ drop in GDP in 1Q21, meaning a W-shaped recovery after all.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more