- Quick take

- 9 June 2021

- Hungary

Hungarian inflation remains steady at 5%

The reopening effect hasn’t reached consumer price statistics just yet in Hungary despite anecdotal evidence fuelling expectations. Even though headline inflation remained flat at 5.1% YoY in May, we think the central bank should stick to its guns with a 15bp rate hike affecting both the 1-week deposit rate and the base rate at the June meeting

| 5.1% |

Headline inflation (YoY)ING forecast 5.4% / Previous 5.1% |

| Lower than expected | |

After a series of upside surprises and strengthening, inflation has stopped accelerating in May.

It is rare to talk about annual inflation above 5% with a negative bias but given the vast majority of forecasts expected headline inflation to reach a new high and a peak in May. The details show that we seem to be missing the reopening related inflation pressure which we expect to show up in eating out and services based on anecdotal pieces of evidence.

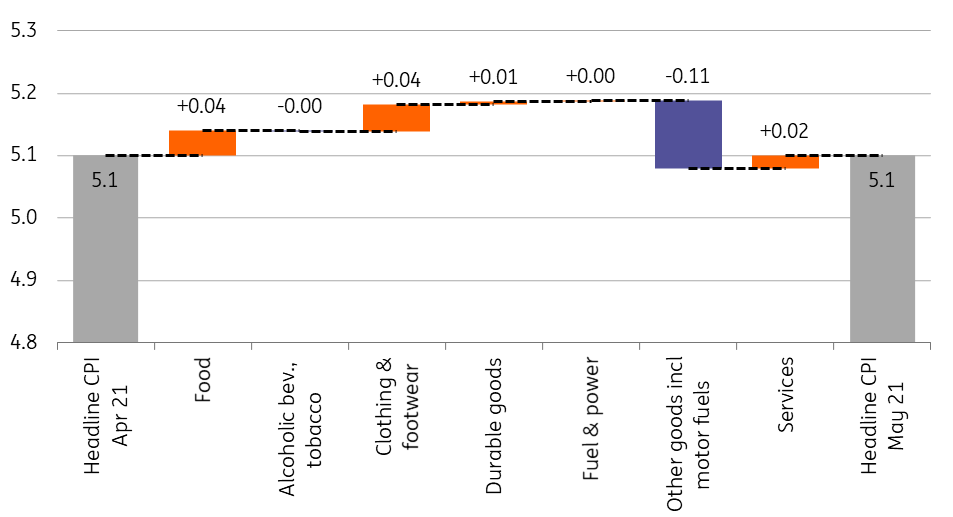

Main drivers of the change in headline CPI (%)

- Starting with the downside surprises, we need to mention the food prices first. Inflation in this product group was only 0.8% MoM, translating into only a 2.6% YoY reading. Eating out showed only 1.1% price increase on a monthly basis, where we expected a much stronger impact stemming from the reopening. It also seems that agricultural producer price increase is spilling over with a delay. We expect June to show a much stronger price pressure in food.

- When we are talking about reopening related inflation, services should come to our mind too. With a gradual reopening started in April and with most of the service providers being able to open for business in May, we expected a significant repricing. In contrast, inflation is services came in at 0.2% MoM and 2.1% YoY. Far away from that price pressure which was tied to reopening in theory. Again, we believe that we see just a delay in statistics.

- The series of downside surprises end with clothing prices where May used to bring a significant price increase based on seasonal pattern. This May however proved to be different in this way too.

- On the upside surprises, the list is relatively short. Fuel prices showed a 1.7% MoM price increase, in contrast with our calculation of a much lower change. Even with this, fuel prices are up by 36.2% YoY, showing a 3ppt deceleration to April. Durables inflation came in at 0.7% MoM, the highest reading in the past 12 months. The ripple effect from accelerating producer price changes and elevating shipping cost seems to be stronger and faster, offsetting the strengthening of HUF.

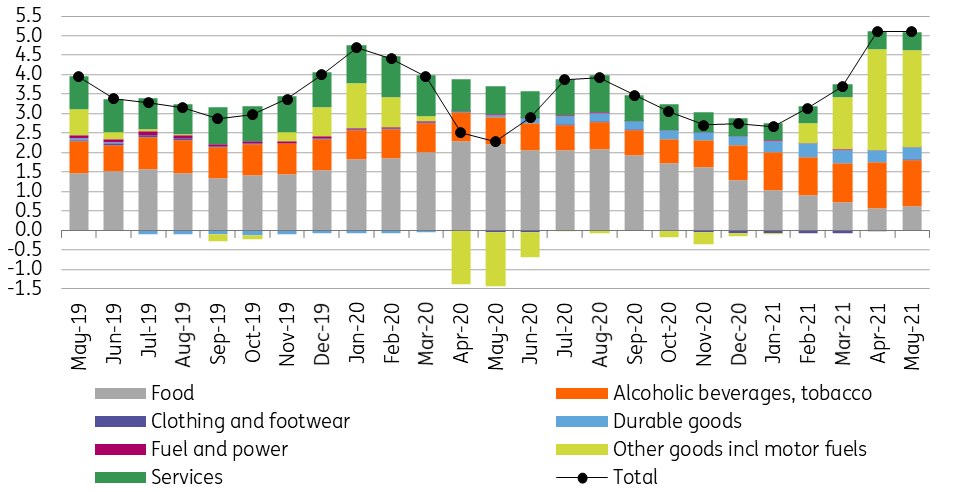

The composition of headline inflation (ppt)

delayed reopening inflation effect

In all, we see today’s surprise is stemming from a delayed reopening inflation effect, which will show up in June.

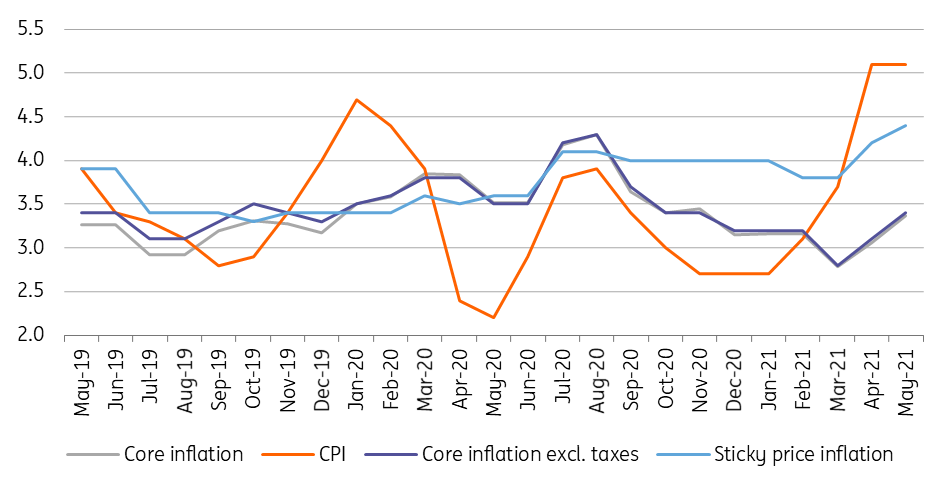

However, core inflation has already moved higher to 3.4% YoY, showing a 0.3ppt acceleration compared to April. This is clearly related to durables. With services and food inflation moving higher in the coming months, core inflation is expected to move north. The underlying price pressure is quite visible if we check the central bank’s indicators. The so-called sticky price inflation moved to 4.4% YoY, the highest since the summer of 2007.

Headline and core inflation measures (% YoY)

With further increasing underlying inflation, we don’t see today’s downside surprise in the headline reading to change the big picture regarding monetary policy.

Upside risks are still there, stemming from delayed reopening price pressures, elevated commodity prices and higher shipping cost, and supply-side issues, which are increasing the price of intermediate products. With all of these pipeline pressures, the central bank needs to stick to its playbook, at least in the short run.

This means a 15bp rate hike affecting both the 1-week deposit rate and the base rate at the June rate-setting meeting, in our view.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more