- Quick take

- 11 January 2022

- Hungary

Hungary’s 2021 deficit explains turn in government’s fiscal plans

The government announced plans to postpone some public investment in mid-December and plans to run a much lower deficit in 2022. Based on 2021 figures, we can see why the government acted so quickly

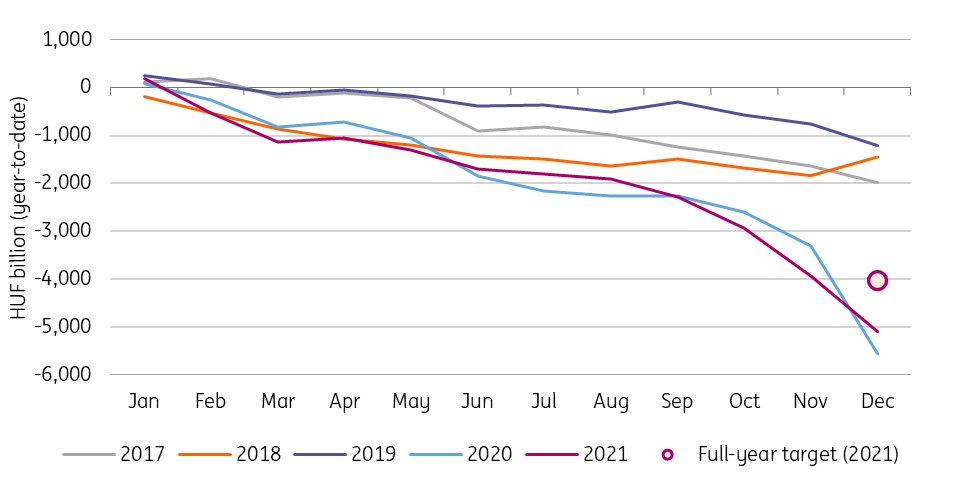

The government decided to postpone some public projects worth HUF 350bn in total in the middle of December. We saw this as a clear signal that something was wrong. The last official data showed the monthly deficit in November at HUF 1.009tn. But of course, the government could already see the budget developments in early December and presumably realised that it wouldn't be able to meet fiscal targets unless action was taken.

The key issue here could be the debt-to-GDP ratio, as based on the fiscal rule, the government needed to reduce public debt as a percentage of GDP in 2021. Early signs were good on nominal GDP growth, but as the third and fourth quarter outlook was revised down, the previously estimated fiscal spending could have caused problems.

But even with this targeted spending freeze, the monthly deficit in December came in at HUF 1.170tn. This is much higher than we initially expected after the government’s announcements and with that, the cash-flow based deficit target was missed by a wide margin. The 2021 budget deficit is 27% above the amended target and is 3.5-times higher than the government planned in late 2020.

Cash-flow based year-to-date central budget balance

We still have to wait until mid-February to see the 4Q21 and full-year GDP figures. But it seems the government has tried its best to estimate this and based on that, tried to use every bit of estimated room still available to spend, without jeopardising the reduction of the debt-to-GDP ratio within a small margin. Against this backdrop, it would be hard to accuse the government of using the “kitchen-sink’ method to reduce the deficit and debt figures. In all, we expect the 2021 debt-to-GDP ratio slightly below 80%.

More than HUF 2.000tn was spent by the government in the last couple of months of 2021 and a roughly similar amount will be pumped into the economy in the first couple of months this year through different tax reductions, tax refunds, wage settlements etc.. With these, we can expect a front-loaded cash deficit accumulation this year and probably significantly increased domestic demand in a supply constrained economy.

Taking into consideration the pro-inflationary and budgetary impact of these moves at the start of the year, it's easy to see why the government is talking about the need to be more conservative with the budget in 2022. As a sign of this, the Finance Ministry announced that it is targeting a 4.9% deficit-to-GDP goal in 2022, 1ppt lower than originally planned. The government will manage savings mainly through cutting planned public investments (either direct spending, incentives or development appropriation).

We see this shift in fiscal policy as favourable in the wake of the demand-supply mismatch which created inflation pressures, and considering the expected record high growth in GDP in 2021 which suggests less fiscal stimulus is needed.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more