- Quick take

- 30 April

- Hungary

Hungary breaks the chains of stagnation but risks being bound again

Economic growth in the first quarter was just as we expected. Increased government transfers finally emerged as a positive contributor, providing momentum for the economy. However, geopolitical tensions could set back any progress achieved so far

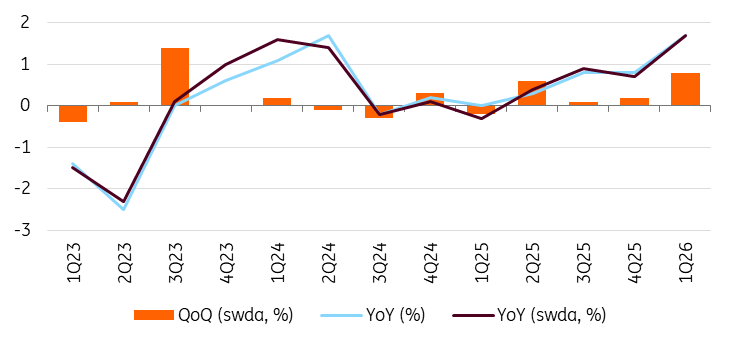

| 0.8% |

GDP growth in Q1 (QoQ, swda)ING forecast 0.8% / Previous 0.2% |

The latest GDP data came as a significant positive surprise compared to the market consensus. In the first quarter of 2026, the Hungarian economy grew by 0.8% on a quarterly basis. This matches our forecast, which provided the most optimistic projection among domestic forecasters. Taking into account last year's low base, the year-on-year index jumped to 1.7%. The last time we saw similarly dynamic year-on-year growth was in 2023, but that was an outlier.

Hungarian GDP growth

The fresh data indicates that the Hungarian economy has now grown for the fourth consecutive quarter. This suggests that the country may have left behind the period of prolonged stagnation. This conclusion is supported by the fact that the Hungarian economy has grown by an average of 0.425% per quarter over the past four quarters. The last time this occurred was between the second quarter of 2023 and the first quarter of 2024.

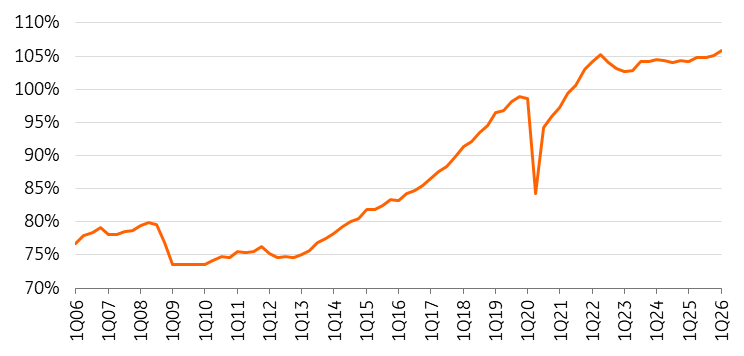

Real GDP in Hungary (2021 = 100%)

As usual, the Hungarian Central Statistical Office (HCSO) provided few details about the underlying dynamics in its flash report. As expected, the services sector made the most significant contribution to the headline number. Within this sector, it was professional, scientific, technical and administrative activities that drove growth. We suspect that this is linked to preliminary activities (e.g. technical and engineering design) related to real estate developments associated with the Home Start programme. Industry also made a positive contribution to the overall performance in the first quarter. This is in line with our preliminary expectations; except we had also anticipated a slight positive contribution from agriculture. However, as the HCSO did not mention this, its effect was likely negligible.

The second estimate, due on 2 June, will shed light on the factors behind the improving performance of the economy. On the demand side, we expect consumption to have been the main driver, supported by modest investment growth. However, the economy’s overall performance may have been held back by the ongoing negative impact of net exports. The latest foreign trade statistics from March also indicate weakness in this area, showing that Hungary’s foreign trade surplus shrank significantly year-on-year in the first quarter.

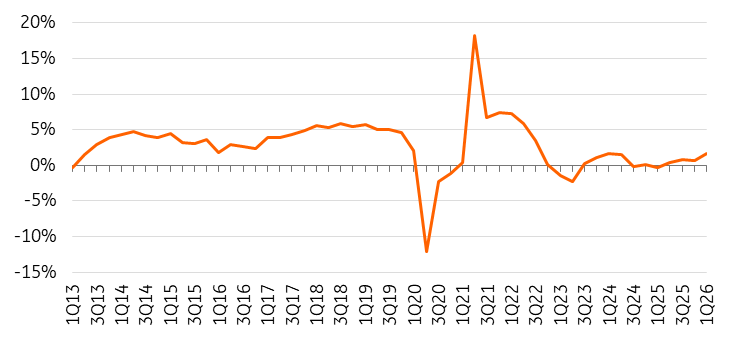

The quarterly annualised growth rate of Hungarian real GDP

We are not revising our 2026 GDP forecast considering the recent data, as this was in line with our expectations. That said, our optimism is not without reservations. The latest developments in the Middle East suggest a more significant negative impact on growth and stronger upward pressure on inflation.

Taking our baseline scenario for current geopolitical developments and energy market prices into account, we forecast GDP growth of around 1.5% for 2026. However, in light of the recent oil price movements, we are becoming increasingly worried that the prospect of a prolonged conflict is a realistic one. This scenario assumes persistently high energy prices. In that case, just as the Hungarian economy appears poised to finally take off, it would face a significant headwind. Uncertainty would therefore be extremely high.

Nevertheless, regardless of the scenario, the structure of economic growth will not change substantially for this year. Consumption could be the driving force, primarily due to fiscal stimulus measures, which may also be supported by a temporary improvement in consumer and business confidence following the elections. However, the prolonged blockade of the Strait of Hormuz poses a clear negative risk to this.

Regarding investments, we anticipate only a modest turnaround and slight growth. In a favourable scenario, therefore, the decline will halt and growth of perhaps 1–2% may emerge. Meanwhile, the heavy reliance on imports for both consumption and investment will drive import demand higher. At the same time, weak external demand and supply chain and energy market shocks do not bode well for any significant positive changes in exports, meaning that net exports could meaningfully hinder economic growth overall this year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more