- Quick take

- 5 September 2022

- Hungary

Hungarian retail sales show signs of weakness

Behind the solid headline retail sales figure, we see some worrying developments. In our assessment, the economy is getting closer to a technical recession

| 4.3% |

Retail sales (year-on-year, wda)ING forecast 5.1% / Previous 4.5% |

| Worse than expected | |

If we look at things superficially, the July retail sales performance in Hungary looks quite good. It shows a 4.3% year-on-year growth rate (adjusted for working days), which is only a tad slower than the headline figure from the previous month. However, as soon as we dig a bit deeper into the data, we see some red flags and signs of weakness.

First and foremost, the month-on-month growth in retail sales was only 0.5%. The only good thing we have to say about this is that it is at least positive after three months of continuous decline. But is also says a lot about the yearly index, which was able to remain strong because of the base effect and not due to the strong monthly performance.

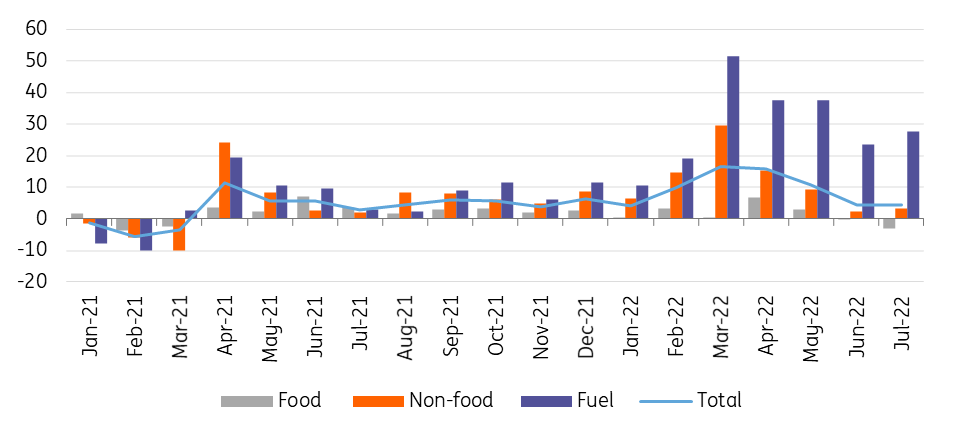

Breakdown of retail sales (% YoY, wda)

After checking the detailed data, today’s release on retail sales paints a rather gloomy picture. Retail sales turnover in the food sector decreased by roughly 0.1% on a monthly basis and also showed an annual drop. This is quite a bad reading in light of the fact that consumers with the highest marginal propensity to consume (i.e. pensioners), received their pension supplement in July. But even this was not enough to boost the volume of food shop turnover, so it can still be said that ever-rising prices are increasingly restraining the consumption of households.

A similar phenomenon can also be observed in the sales volume of non-food stores. Turnover in this segment fell by 0.25% compared to the previous month, even though the news was full of stories about households rushing to the shops to replace non-energy-efficient appliances as the government announced changes to the utility bill support scheme. Moreover, sales people have echoed that demand has increased sharply for alternative heating devices in order to reduce gas consumption. It seems that either these effects have not yet been reflected in the July statistics or, despite the boost in demand, households have already closed their purses and cancelled shopping for non-essential major goods and cut fast-moving consumer good spending.

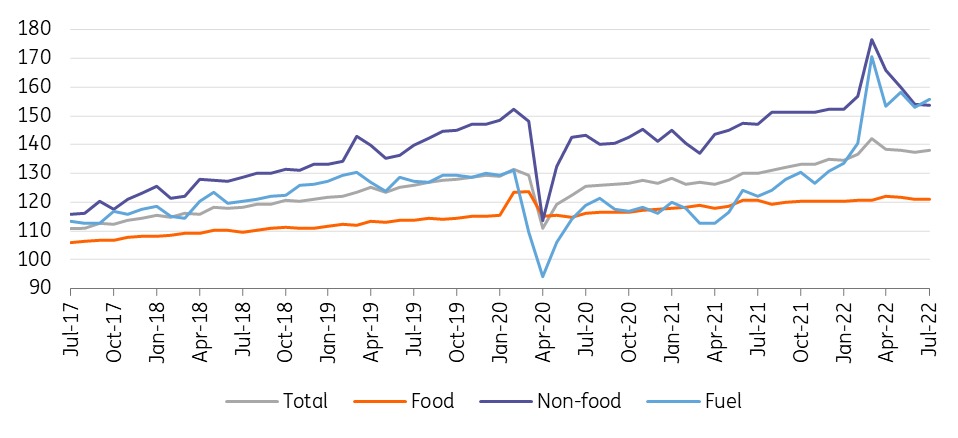

Retail sales volume in detail (2015 = 100%)

Only the turnover of fuel retailers was able to increase on a monthly basis in July. In essence, this one item ensured that retail turnover did not shrink continuously for four months. This, therefore, paints a rather gloomy picture, especially as we know that the increase in fuel sales may be a one-time effect as the government announced a reduced range of beneficiaries of the fuel price cap from 1 August. Many people who use a company car for private purposes will have to buy fuel at a much higher market price from August, so the last chance to buy fuel at administered prices came in July, giving an extra boost to fuel demand.

In addition to all of this, it is also quite telling that in all the sub-sectors, the turnover of second-hand shops increased the most, which once again highlights the increase in the price sensitivity of consumers and the transformation of shopping habits.

Retail sales and consumer confidence

Based on today's retail statistics, we can say that although the main indicator does not reflect this, the underlying processes and detailed data already show a strong slowdown in consumption at the beginning of the third quarter. Households continue to adapt to higher inflation, and in the coming months the effect of budget tightening (e.g. the changes in the utility bill support scheme) may further strengthen this. Although it is still too early to make a judgment, the probability that the volume of GDP will show a quarter-on-quarter decrease in the July-September period has clearly increased. Our silver lining here would be that during the summer, services can help the expansion of consumption to a greater extent. Instead of buying things, consumers are focusing their spending on experiences, which is not measured by retail sales data.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more