- Quick take

- 29 September 2023

- Hungary

Hungarian labour market remains surprisingly stable

We are seeing a gradual deterioration in the labour market for the third consecutive month. However, the changes have been so gradual that the unemployment rate has remained stubbornly low despite the economic difficulties

| 4.1% |

Unemployment rate (Jun-Aug)ING Forecast 4.0% / Previous 3.9% |

| Worse than expected | |

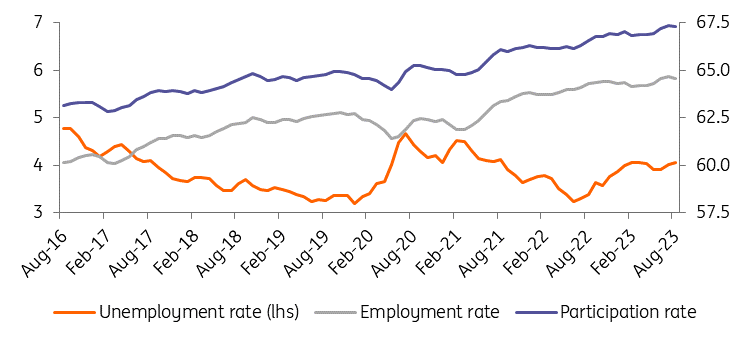

The latest unemployment figures published by the Hungarian Statistical Office show no significant change in the labour market in August. Both the model estimate for August (4.0%), and the survey-based official three-month moving average unemployment rate (4.1%) increased by 0.1ppt compared to the previous month. In this regard, the number of unemployed people remained below 200,000.

Although the unemployment rate is higher than a year ago and has now deteriorated slightly for three consecutive months, these labour market statistics are still quite positive given the Hungarian economy has been in an unprecedented four-quarter technical recession.

Looking at the monthly data, perhaps the most important change is that the number of people employed dropped by 35,800 (-0.8% month-on-month). Those who left their jobs mainly left the labour market altogether, as the labour force participation dropped by 34,100, while the number of unemployed moved up by only 1,700 in August. All this leads us to the conclusion that the rise in the unemployment rate is mostly due to the bigger fall in participation. It is important to note, that the number of labour market participants is still above 4.9 million, only 1% below the all-time high.

Historic trends in the Hungarian labour market (%, 3-m moving average)

In our view, the slight increase in the unemployment rate is not an overly worrying trend. Yes, there are some ongoing adjustments in the labour market, but this is more or less to be expected in a situation where the economy is going through four quarters of GDP declines on a quarterly basis. We expect further small increases in the unemployment rate in the coming months due to seasonal effects, but even if we see a further rise in the indicator, the peak could remain close to 4%.

Our relatively optimistic view stems from the supply side of the labour market, which is strongly influenced by the high inflation environment. This keeps people interested in having or getting a job and earning more. But as disinflation progresses, some of the labour force may be checked out. This suggests that employers may face further difficulties on top of the labour shortages they are already experiencing.

Against this backdrop, firms will continue to insist on retaining staff, knowing that it will be difficult to increase hiring in the recovery phase with a structural shortage of labour. The guiding principle is therefore two-fold: firms are optimistic about the recovery of the Hungarian economy, but also pessimistic about labour supply.

We continue to see upside inflationary pressures as the main risk stemming from the tight labour market. Ongoing talks on next year's minimum wage point to a possible agreement on an increase of between 10-15%, which, barring any major inflationary surprises, would lock in significant real wage growth for next year. There are also rumours of some additional wage adjustments for this year's inflation towards the end of the year. What could anchor inflation expectations is a long-term deal on minimum wages, which also seems to be on the table with pre-agreed minimum wage increases until 2027. In this respect, recent developments – if they materialise – lead us to believe that the likelihood of wage-push inflation is lowering in the long run.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more