- Quick take

- 28 September 2021

- Hungary

Hungarian labour market participation plateaus

Demand for labour is increasing while supply seems to be reaching a plateau. This suggests higher fluctuations and increasing wage push inflation

| 4% |

Unemployment rateING forecast 3.9% / Previous 3.9% |

| Worse than expected | |

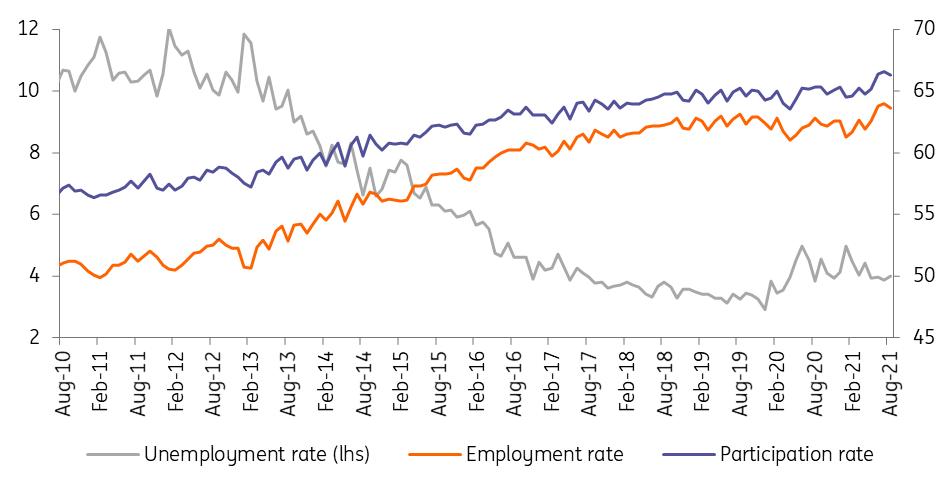

According to the latest data from the Hungarian Central Statistical Office (HCSO), the unemployment rate was 4% in August. This shows stability as the jobless ratio has been fluctuating around this level for four months. This could even be a technical effect coming from a proportionate increase in labour market participation and employment.

Based on the detailed data, it's becoming clear that there was only a minimal fluctuation in the different labour market indicators during the summer months. The number of participants (economically active) in the Hungarian labour market has stabilised at just under 4.9 million, which is a record high. Thus, based on the official statistics, participation seems to be plateauing. We see two important barriers here: first, the current regulatory environment and second, labour market frictions (e.g. localisation and quality mismatch of work force). Neither of these are really being addressed, so labour market supply is unable to expand much further.

Labour market trends (%)

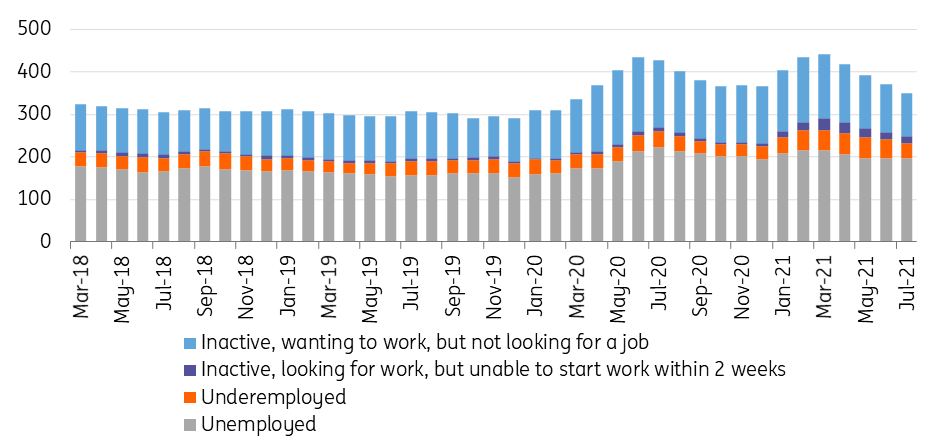

Among labour market participants, there are roughly 190,000 people unemployed but actively looking for job, while the number of employed also stabilised at around 4.7 million in the past few months. But the unemployed are just one part of the potential labour reserve in the country. There are also people who are inactive and wanting to work but not looking for a job. There is also a group of inactive people who are looking for work but unable to start work within two weeks. And finally, there are the underemployed.

The HCSO used to release monthly data about the potential labour reserve but not anymore. Since a methodological change in July, we won’t see the monthly data in the official database. However, in its weekly monitor we can check the three-month moving average of the potential labour force with some delay. According to this, the labour reserve is now around 350,000 (56% unemployed, 10% underemployed, 29% inactive not looking for job and 5% inactive but unable start in two weeks' time). This shows a trend-like decrease since the start of the year, culminating in an increasing labour shortage.

Potential labour reserves within the 15-74 age group ('000)

3-month moving average

The labour shortage is also driven by increasing labour demand, as the number of job vacancies are increasing and edging closer to the pre-crisis record level. The most glaring need for labour in the private sector can be seen in manufacturing, accommodation, IT, finance and administrative and support services.

Against this backdrop, the pre-crisis labour market issues are returning, which are causing significant fluctuations and work force drains, with constantly increasing wage pressure in the economy. In our view, today’s data is another clear signal that wage push inflation is building and strengthening.

We do not expect the fourth wave of Covid to generate a significant labour market problem. We expect a very slow improvement in the labour market situation due to the supply side constraints. By the end of the year, the unemployment rate could move close to 3.8% with the help of rising average wages, which could increase the number of labour market participants. And in the current labour shortage situation, the market can quickly absorb new entrants.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more