- Quick take

- 8 May

- Hungary

Hungarian inflation picks up but second-round effects still contained

Hungary’s inflation continued to accelerate in April, moving meaningfully away from the decade low reached in February. Yet the latest figures are a clear positive surprise given that we have now entered a third month of energy price shocks. Despite all the unknowns, we still anticipate a favourable full-year average inflation rate this year

| 2.1% |

Headline inflation (YoY)ING estimate 2.2% / Previous 1.8% |

| Lower than expected | |

Inflation is rising, but the pace remains measured

According to the latest data released by the Hungarian Central Statistical Office (HSCO), inflation in April accelerated further, clearly steering away from the decade-low level seen in February. Still, the latest print is a clear positive surprise, as it implies somewhat less price pressure than market consensus had feared. Consumer prices were 2.1% higher year-on-year, while the average price level rose by 0.4% month-on-month.

What makes this resilience particularly noteworthy is that the inflation data has now been reflecting the impact of the war in the Middle East and the blockade of the Strait of Hormuz for two months. Even so, Hungary’s inflation figures have so far shown an impressive ability to absorb the shock. Of course, the second-round effects have not arrived in force yet (for example, in the APAC region, they are already more visible), so it would be premature to sit back and relax. But it is still encouraging that companies appear to be holding off on broad price hikes, despite March producer price data already signalling a meaningful cost shock for manufacturers.

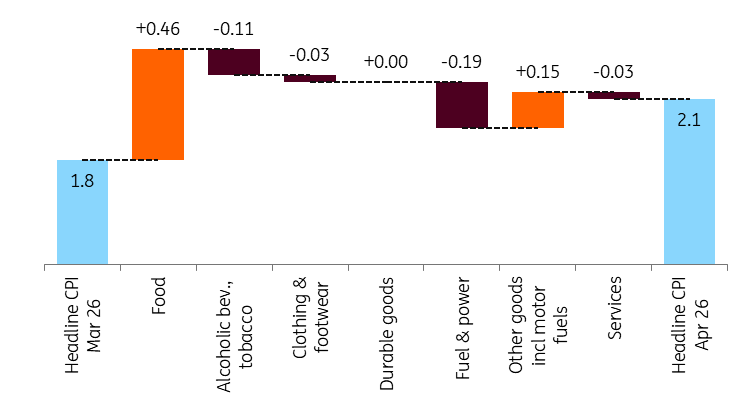

Main drivers of the change in headline CPI (%)

The details

- Food prices have not yet been significantly affected by the conflict in the Middle East. For now, prices increased by just 0.1% month-on-month in April. However, the conflict is likely to affect the food chain with a delay, primarily through fertiliser prices and the associated cost pressures on agriculture. The year-on-year increase is due to the base effect, whereby the impact of the margin freeze has moved into the base period.

- For durable goods, a 0.1% monthly decline is a mild surprise. In our view, this is consistent with the significant strengthening of the forint, which likely helped dampen imported goods inflation.

- As expected, clothing and fuel provided a meaningful lift to inflation. The former due to seasonal effects. On fuel, from now on we can expect flat prices until the price caps are in place.

- By contrast, household energy acted as a notable drag, with prices falling by 0.9% on the month, reflecting the utility bill changes with a lag due to technical factors. The change was also in line with our expectations.

- If there is one area where the energy shock may already be starting to seep in, it is services. Beyond seasonal effects, we are seeing price increases in categories that are directly exposed to the strains created by the current geopolitical environment, notably transport-related services. Meanwhile, the holiday-heavy April period pushed up the price of domestic recreation more strongly, which is likely to prove largely a one-off.

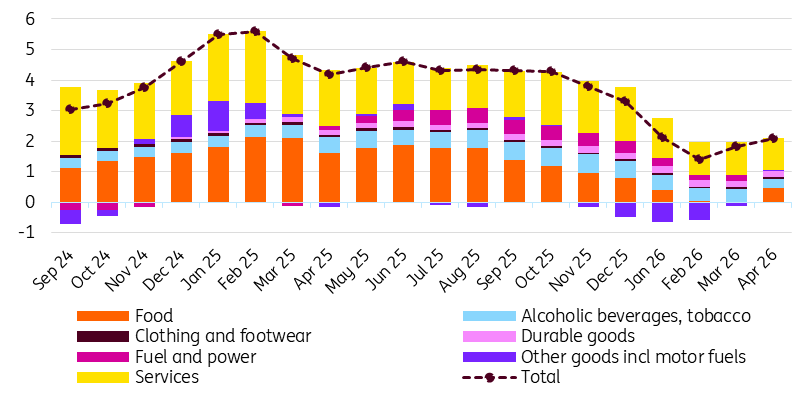

The composition of headline inflation (ppt)

Underlying price pressure shows a favourable picture

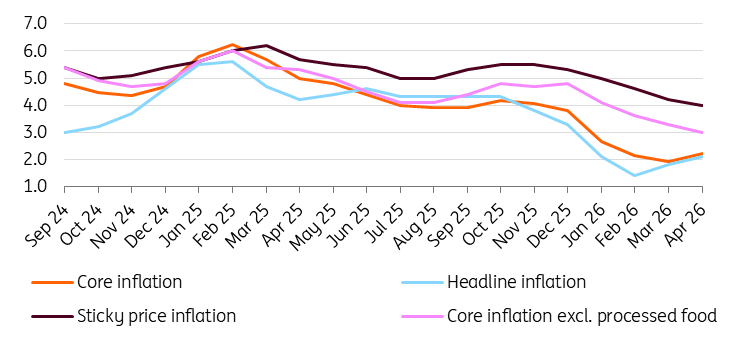

The core inflation rate, which is adjusted for volatile items including changes in fuel prices, still looks good. This suggests that second-round effects are not yet widespread. The acceleration to 2.2% year-on-year is not a figure that should cause concern. Other underlying indicators calculated by the central bank also show a favourable picture, especially as these have kept moving lower in April. However, this does not mean that things could not deteriorate quickly. Each month that passes with a live blockade increases the likelihood of a major price shock due to non-linearities.

Headline and underlying inflation measures (% YoY)

A better-than-feared trajectory remains possible

Based on the latest figures, there is a significant chance that inflation in 2026 will be more favourable than the scenario predicted by the National Bank of Hungary in March. The April figure was below the central bank’s point forecast, but still within the uncertainty band. However, the toughest part is still ahead. Energy prices remain significantly higher than before the outbreak of war in Iran, and the risk of delayed pass-through remains high.

Our latest quick estimate suggests that year-on-year inflation could rise to around 3% in the summer and reach 4.0–4.5% by the end of the year, according to our base case scenario. Therefore, although inflation is rising from a decade-low starting point, the pace of acceleration is still fairly contained. This leaves room for headline inflation to average around 3.0–3.5% in 2026. However, a prolonged blockade or re-escalation would pose a clear upside risk to our base case, with average inflation potentially exceeding the NBH’s tolerance band.

Inflation in the coming months will be shaped by the price‑shield measures. We expect the new government to extend these in the near term before gradually phasing them out. Voluntary price caps imposed by service providers will be lifted in the coming months. The delayed impact of fiscal policy changes could also pose some pro-inflationary risks. Local weather-related issues will also push up food prices going into the end of the year, with the impact of the Strait of Hormuz blockade being the ultimate wild card.

In this highly uncertain environment, it is unlikely that today's inflation data will materially shift the stance of monetary policymakers in the near term. That said, we would not rule out a rate cut or a rate hike later this year; the direction will depend on how the geopolitical situation evolves and whether the Hungarian forint can strengthen significantly. According to our base case scenario, we expect the base rate to remain at 6.25% throughout the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more