- Quick take

- 13 January

- Hungary

Hungary’s inflation surprise shuts some rate cutting doors

Inflation in Hungary came as an unpleasant surprise in December, driven mainly by the service sector. Despite the positive trend of falling inflation, we think this recent development has reduced the options available to the National Bank of Hungary

| 3.3% |

Headline inflation (YoY)ING estimate 3.0% / Previous 3.8% |

Inflation rate getting lower but not as low as expected

According to data recently released by the Hungarian Central Statistical Office (HCSO), inflation continued to decline in December 2025. However, the latest figures have left analysts with a somewhat bitter taste. At 3.3%, the inflation rate exceeds the market consensus. On a monthly basis, prices rose by only 0.1%. The 0.5ppt slowdown in the year-on-year indicator compared to November is therefore partly due to low monthly repricing and partly to the base effect.

Main drivers of the change in headline CPI (%)

The details

- Perhaps the biggest surprise is the increase in service prices. This is an unusual development. At the end of the year, the monthly rate of price change is typically low due to seasonal effects. However, in December 2025, the price level of services increased by 0.8% month-on-month. The last time this happened was in 2022, at the height of the domestic inflation shock, when the price increase for services in December was also this high. This means a previous record has been matched.

- The 9.5% monthly increase in transport prices may be related to a significant rise in road tolls, prompting carriers to increase their prices drastically. There was also a notable increase in the cost of telephone and internet services. The high monthly inflation rate is likely due to the discontinuation or restructuring of certain subscription packages in an evolving market.

- Food prices were generally stable on a monthly basis, consistent with global price trends and the extended price cap measure. Prices of alcoholic beverages and tobacco products rose slightly less than expected in December.

- The price of household energy rose significantly on a monthly basis, adding to the series of surprises. As expected, falling fuel prices significantly reduced the monthly inflation rate.

The composition of headline inflation (ppt)

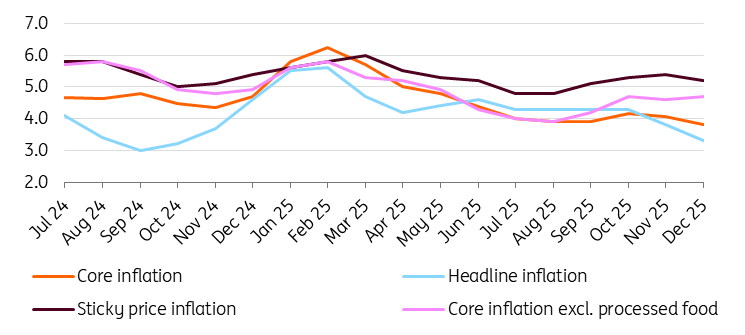

Core inflation is still inconsistent with the goals

Despite the long-standing moderate monthly inflation rate, the underlying trends are not yet clearly favourable. This is evident in the core inflation indicator, which, although it has declined, remains inconsistent with the central bank's price-stability target. In December, core inflation stood at 3.8% YoY. Furthermore, sticky price inflation, as calculated by the National Bank of Hungary, remains at an uncomfortable rate of 5.2%.

The yearly inflation fell from 3.8% in November to 3.3% in December, mainly due to a slowdown in the annual inflation rate for fuel and food. In contrast, the year-on-year inflation rate for services accelerated. In terms of the structure of inflation, services remain the largest contributor, with food, alcoholic beverages, and tobacco products also accounting for a significant share. Together, these generate 3.1% inflation. It will be interesting to see how service inflation, which is widespread and strong, will shape household inflation expectations. These remain too high and are not consistent with achieving price stability.

Headline and underlying inflation measures (% YoY)

Dreams for a cut in January has been destroyed

Looking ahead, the inflation rate may continue to decline in the coming months due to base effects. However, compared with previous months, the risk of rising prices for services and durable consumer goods has increased. The extremely cold weather in January may also have an adverse impact on household energy prices, pushing them up significantly. The future of price-cap measures will also significantly influence this year's average inflation rate, but another extension is likely. Furthermore, the National Bank of Hungary’s calculations show that inflation of tradables and market services, excluding the price-reducing effect of the price restrictions at the time of their introduction, rose to 5.7% in December.

In light of Mihály Varga's statement yesterday that the NBH will prioritise the December inflation data, particularly service inflation, it is highly unlikely that there will be an interest rate cut in January. However, more moderate repricing this month could pave the way for an interest rate cut in February. We can expect a total easing of 50–75bp this year, although this forecast is subject to a number of uncertainties stemming from both local and external factors.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more