- Quick take

- 14 January 2022

- Hungary

Hungarian core inflation at 20-year high

While price drops in some non-core product groups stopped headline inflation from accelerating, core inflation jumped to a level not seen in 20 years. Higher-than-expected data supports our non-consensus CPI outlook

| 6.4% |

Core inflation (YoY)ING forecast 5.9% / Previous 5.3% |

| Higher than expected | |

Headline inflation stuck at 7.4%

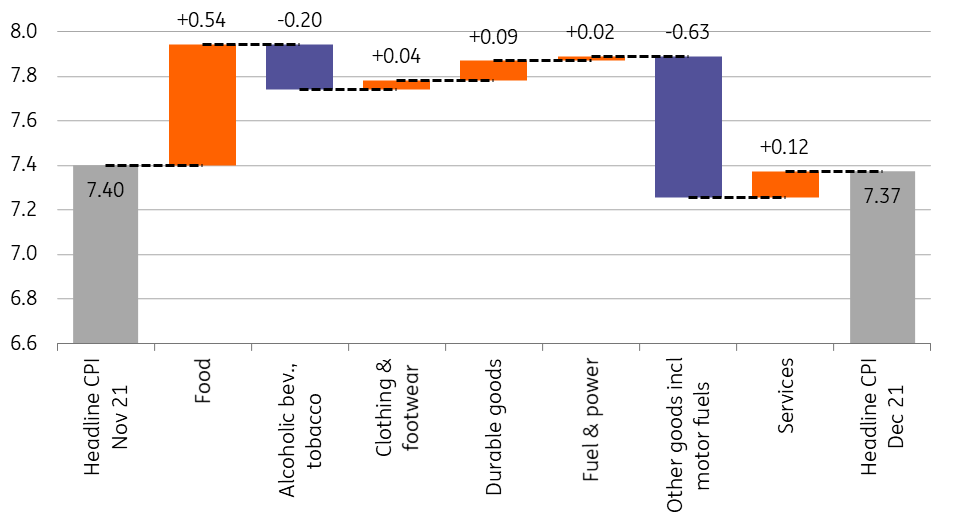

Analysts were hoping that fuel price changes would tame inflation somewhat in December. But headline inflation remained at 7.4% year-on-year, matching the figure from the previous month. Month-on-month inflation came in at 0.3%, the same figure seen in December last year and the year before. So we can’t say this was a true outlier. What was an outlier, however, was core inflation as price pressures became more widespread, with corporates using their strong pricing power in an economy driven by shortages.

Main drivers of the change in headline CPI (%)

The details

- Speaking of pricing power, first and foremost we can see this effect in food inflation, which was sitting at 8% YoY in December. Producer prices in agriculture are skyrocketing on energy and commodities. On top of that, price expectations are also moving higher, making price changes easier for food producers and retailers. In our view, retailers might have moved price changes from January to December given the rise in minimum wages, the new “best-before” regulation and the retail tax hike in 2022, which have all put pressure on margins.

- Inflation in services also accelerated by 0.4ppt to 5.0% YoY in December, mainly driven by cultural and leisure activities, holiday packages and household services. The 0.3% monthly price increase roughly matches the average seen in the past month; thus this sector didn’t bring forward any start of the year price increases, in our view.

- We also need to talk about durables, where inflation moved up to 7.5% YoY after another +1% monthly price increase. Imported inflation in Hungary is becoming more of an issue as manufactured goods producers face increasing cost pressures from the supply side. Domestic industrial output prices were 31.2% higher on average based on the latest available data, which points to further pipeline price pressure.

- What saved Hungary from another rise in headline inflation was the change in fuel prices. The fuel price cap wasn't needed in December, as the drop in oil prices helped to drive fuel sales prices down 5.3% on a monthly basis. This shaved off 0.3ppt from monthly headline inflation. Another non-core product, tobacco also helped to tame inflation pressure. Although the 1.5% month-on-month increase looks strong, last year’s base was even higher as tobacco producers had already raised prices in December, facing an excise duty change in January and feeling the cost side pressure from a weaker forint.

The composition of headline inflation (ppt)

Underlying price pressures rise

In all, there is widespread inflation pressure in non-core elements, showing a significant spillover effect from supply-related price shocks and the second-round effects of wage growth. Core inflation rose by 0.8% MoM translating into a 6.4% YoY figure in December, a 20-year record. The so-called sticky price inflation (which shows the prices of components of the consumer price index which are slow to change, and therefore are good predictors of medium-term developments in headline inflation) spiked to 6.6% YoY, an all-time high.

Headline and core inflation measures (% YoY)

2022 inflation could be well above official forecast

Considering the upside surprise in core inflation and the possibility of a further increase in headline inflation in January, we see the latest official forecasts of the government and the central bank as conservative with a roughly 5% YoY reading in 2022.

We see our 5.6-5.7% headline inflation forecast as justified, with risks tilted to the upside mainly on underlying inflation pressure. While it seems that food retailers have already started to price in the cost of new measures and elevated wages, we haven’t seen this behaviour in other sectors. We still see a non-negligible chance for an above 1% MoM headline inflation in January, which would elevate headline inflation further. However, price cap measures in food (90 days from 1 February) and a possible lengthening of the fuel price cap (ends 15 February based on recent regulation) will help avoid headline inflation moving well above 7.5%, while base effects will reduce the reading from the second quarter.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more