Higher deficit and unidentified outflows weigh on reserves in Turkey

External pressures in Turkey continued with another higher-than-expected current account deficit in May, while reserves have remained under pressure given weak capital flows

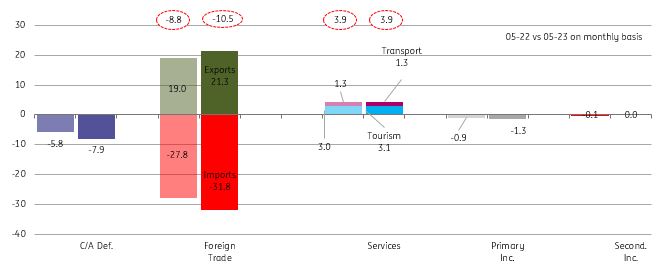

Breakdown of current account (monthly, US$bn)

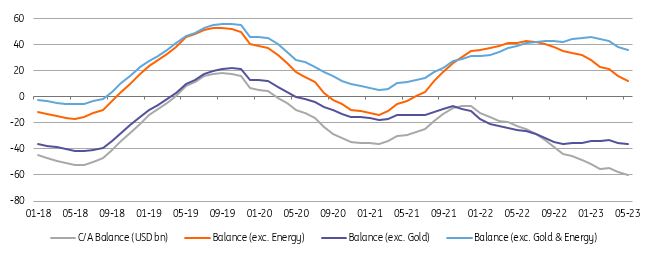

External developments remained challenging in May with another higher-than-expected current account deficit of US$7.9bn, widening the 12M rolling figure further to $60bn (translating into around 6.1% of GDP), the highest since late 2013. A quick glance at the May data points to a similar performance in the services balance with respect to the same month of 2022, although there was a relatively wide deficit in the goods balance driven by higher core trade and gold deficits despite the improving energy trade balance.

Current account (12M rolling, US$bn)

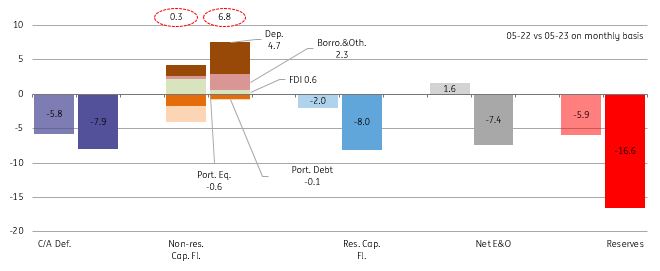

The capital account, on the other hand, witnessed net outflows of $-1.2bn. With the monthly current account deficit and outflows via net errors and omissions at $7.4bn, official reserves recorded another large decline at $16.6bn (not only the cumulative deficit in the first five months but also part of large unidentified outflows at $13.7bn in the same period).

In the breakdown, contributing to net monthly outflows, we saw asset acquisitions abroad by residents at a net $8.0bn, driven by growth in external deposits and trade credits extended by locals. For the non-residents, $6.8bn inflows were attributable to $0.7bn gross of foreign direct investment, $5.1bn of deposits placed by foreign investors to the Central Bank of Turkey, $1.6bn of trade credits and $0.7bn net borrowing by banks.

On the flip side, we see outflows via declining equity assets of non-residents at $0.6bn. Regarding the rollover rates, we saw a strong performance for banks at 142% on a 12M rolling basis (vs 86% in May alone), while the same ratio for banks stood at 85% (a healthy 130% in May).

Breakdown of financing (monthly, US$bn)

Overall, the data once again confirm a growing need for a rebalancing in the economy. Going forward, we will likely see an improvement in the current account as evidenced by the normalisation in energy prices and continuing strength in tourism, while a recovery in global demand should also be supportive of the foreign trade balance.

Continued strength in domestic demand points to upside risks to imports, however recent currency weakness in the aftermath of elections and tightening in the policy mix has led to a slowdown, helping to control import growth.

On the capital account, total flows have remained weak in the absence of strong unidentified inflows, leading to pressure on international reserves so far this year. Going forward, a pivot to a more conventional policy stance will likely be critical for recovery in investor confidence and hence capital inflows.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap