- Quick take

- 18 July 2017

- FX Rates

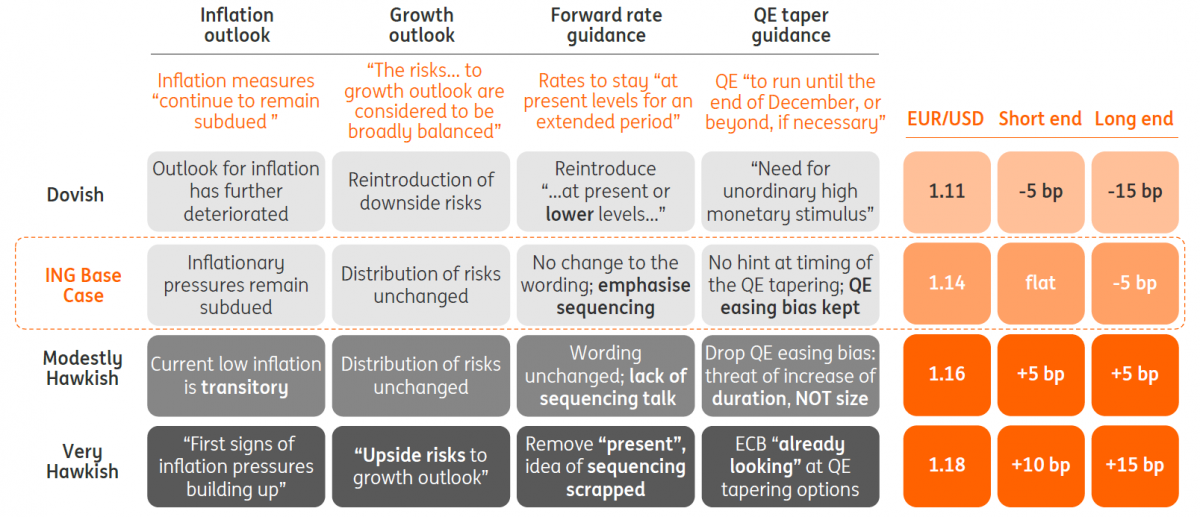

Four scenarios for markets at July’s ECB meeting

Draghi's challenge will be to keep markets tuned into tapering, without causing a 'taper tantrum'

Fully justified EUR/USD strength – break above 1.1500 is on the cards

We see the two-step post-French elections EUR/USD rally as fully justified starting with a build-up of QE taper expectations, amplified by Draghi’s Sintra speech, mainly driven by steeper German yield curve. It seems it will only be a matter of time before EUR/USD breaks through 1.15 (as bund yields nudge up), with an overshoot around the ECB September meeting.

Materially lower EZ yields not necessarily desirable at this point

We see limited scope for lower Eurozone sovereign yields. While the ECB wants to avoid a taper tantrum bund sell-off, it also seeks to pre-prepare the market for eventual QE tapering via gradually higher yields. Thus, a dovish surprise and sharp decline in bund yields is not desirable. The likely retention of the QE easing bias (the threat of an increase in QE duration and size) may push German 10-year yields lower, but don’t expect a material move below 0.55%. We could see German yields rise hit 0.65% later this year.

Scenario analysis: How to position for Draghi's alternatives

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more

Included in the following bundle

Our guide to July’s ECB meeting

- This bundle contains 2 Articles