- Quick take

- 14 December 2023

- Romania

Back to the drawing board on fiscal consolidation in Romania

Romania's 2024-2026 fiscal budgetary strategy lays out an 'as good as it gets' plan given the numerous past and future budgetary obligations the country faces. The most striking element is the unwritten one: bringing the deficit to -3.0% of GDP is officially out of sight

The 2024 budget draft has been published by the Ministry of Finance (see here, in Romanian only) together with the 2024-2026 fiscal budgetary strategy. Looking at the main numbers, one might argue that the fiscal consolidation plan is not looking overly ambitious. However, considering the most recent pension law, the future public wage hikes and plans for investment spending, the targets don't appear to be overly loose.

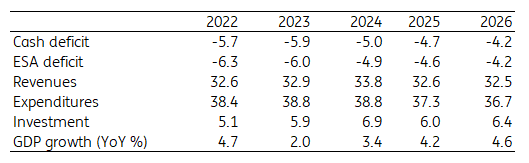

Key numbers (% of GDP)

We note that, despite very recent public statements coming from officials that the 2023 budget deficit will be -5.5% of GDP, there is a last-minute estimated slippage to -5.9% which will make the deficit even wider than in 2022. This is rather surprising for us, given that Romania is under the Excessive Deficit Procedure (EDP) and we were expecting a small but nevertheless symbolic improvement from 2022’s -5.7% of GDP deficit. It remains to be seen how this will reconcile with the European Commission’s tolerance for the graduality of fiscal consolidation in Romania.

For 2024, there is a 12.6% planned increase in total revenues, with most categories set to contribute more to the budget. The most notable exception is EU money, as 2023 likely marked a peak in the amounts received from the EU given the overlap of 2014-2020 MMF, the NGEU and the 2021-2027 MMF.

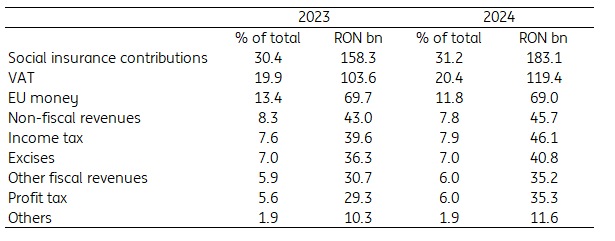

Revenues composition and dynamic

On the expenditure side, there is a slightly more nuanced picture. The total expenditures are planned to increase by 9.4%, with the main categories set to grow by double-digits. Investment spending in particular should see a whopping 29% increase in 2024, as this will probably the peak year for investment spending over the medium term.

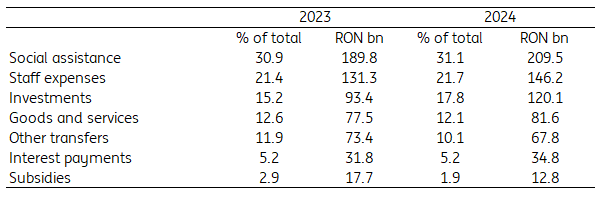

Expenditures composition and dynamic

We also note that the official GDP growth and inflation estimates for 2024 are at the upper range of consensus forecasts, which leaves limited room for manoeuvre in case of risks materialising.

Chiefly among these risks, we underline the possibility of EU funds absorption being below plan, a rather optimistic estimate on the growth in the number of employees in the economy, strikes that are certain to occur in the electoral year, overstated improvement in tax collection and overstated impact on revenues of the most recent fiscal changes and – last, but not at all least – an even less supportive external environment, be it economic or geopolitical. Even the 4.2% GDP growth in 2025 looks rather toppish to us, given the fully fledged fiscal reform (read: higher taxes) that we expect to be adopted in late 2024 in order to offset the pension hikes.

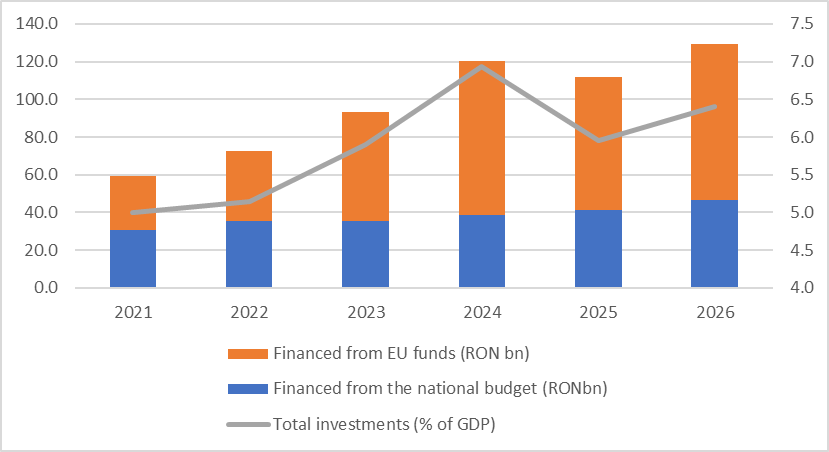

EU funds remain key to investment growth

How the financing looks

In pretty much any scenario, the total financing needs will be smaller in 2024 compared to 2023. 5.0% of GDP deficit in 2024 means approximately RON 87bn. On top of that, we estimate 2024 redemptions at RON 75bn which leads to a total of RON 162bn to be financed. A small part of this amount will be prefinanced in 2023 already (say north of RON 10bn), leaving roughly RON 150bn to be financed from the market in 2024.

A sticky financing source should be retail bonds, which could bring another RON 15bn or more next year, leaving what we believe to be a reasonable amount to be tapped in 2024. As in 2023, we believe that the financing will focus on the domestic market, where the Ministry of Finance will probably issue as much as the market will want to buy at a relatively constant yield differential versus peers. The marginal buyers versus 2023 could be the local banks, as a decreasing yields environment and still strong deposit growth might incentivise adding some papers and duration to their portfolios.

What we make of it

The pace of fiscal consolidation might not look overly ambitious, but it does strike a realistic balance in our view between the need to preserve support for the economy while bringing the deficit closer to more acceptable levels. At this moment, our forecasts for the 2024-2026 budget deficit are very close to the official ones. However, there are very few positive risks while quite a few downsides to the base case. Moreover, negotiations with the European Commission over the pace of deficit reduction could still bring some changes to the plan.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more