- Quick take

- 11 July 2019

- Turkey

Turkey: External deficit at its lowest since 2003

External balances remained on a recovery track in May, while a monthly surplus and capital flows contributed to an increase in reserves.

| $-2.3 bn |

Current account deficit12-month rolling, as of May |

With weak economic activity weighing on import demand, and healthy exports on increased price competitiveness and support from tourism revenues, external balances have seen a quick improvement since mid-2018, standing at a mere a US$-2.3 billion on a 12M rolling basis, their lowest since 2003. The slightly lower than expected surplus in May at US$0.15 billion contributed to the further narrowing in the annual deficit, at -0.3% of GDP.

In the breakdown, the monthly improvement over the same period of 2018 is attributable to a contraction in foreign trade, along with relatively small supportive readings from services and secondary incomes.

External Balances (USD bn, 12M rolling)

On the capital account, May saw some inflows at US$1.3bn following outflows in the previous two months - on the back of increasing concerns about CBT reserves and ensuing market volatility. Given a mild external surplus and inflows via net errors & omissions, official reserves recovered by US$3.0 billion.

In the monthly breakdown, capital inflows are mainly attributable to declining FX currency and deposit assets of banks held abroad. We see contributions from continuing FDI, also facilitated by cheaper Turkish assets in the aftermath of August 2018 volatility and trade credits. This is despite drags from further portfolio outflows, a drop in non-resident banks’ deposits held in Turkey and debt repayments of banks and corporates.

On borrowing, banks have remained net payers at US$-0.6 billion (driven by long term repayments translating into a monthly rollover ratio at 83% vs the 12M rolling figure at 65%), while corporate sector borrowing was also negative (with the long term monthly rollover ratio at 78% vs 115% on a 12M rolling basis).

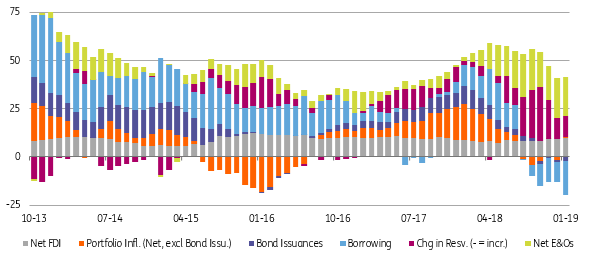

Breakdown of C/A Financing* (12-month rolling, USD billion)

* Positive sign in reserves shows reserve accumulation

Overall, on year-to date basis, key capital account trends over the same period of 2018 are: (1) residents’ increasing acquisitions of assets abroad, (2) higher FDIs, (3) higher portfolio flows facilitated by the Treasury’s Eurobond issuances, (4) negative net borrowing, and (5) sharp decline in net errors and omissions. Going forward, a global backdrop with increasing market expectations of Fed rate cuts given weakening prospects for global trade and global investment can impact countries like Turkey. But, idiosyncratic risks should remain a drag for the capital flow outlook.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more