- Quick take

- 27 February

- Hungary

Employment in Hungary hits an almost five-year low

The official unemployment rate increased in January, while the population continues to decline. Employment dropped to a level not seen for almost five years, suggesting that Hungarian companies started to rationalise earlier than expected

| 4.6% |

Unemployment rate (Nov–Jan)ING estimate 4.4%/ Previous 4.4% |

The latest labour market statistics from the Hungarian Central Statistical Office (HCSO) paint a much gloomier picture than forecasters had anticipated. It seems that companies adapted to wage cost pressures much sooner than expected. According to model estimates, the unemployment rate reached 4.6% in January 2026. Meanwhile, the official three-month moving average survey reports a similar rate. So in both cases, we can speak of a significant increase, i.e., a deterioration in the labour market situation. Based on these official figures, the unemployment rate has reached a new high since autumn 2024, meaning that there are now around 225,000 unemployed people in Hungary.

Examining the details, the monthly data reveals that the decline in the working-age population continued at the start of this year, accompanied by a decrease in the number of people in employment. However, the decline in the number of those employed far exceeds the decline in the number of labour market participants. In January, there were just over 4.6 million employed people, which is the lowest figure since May 2021.

As the decline in employment was not accompanied by an increase in inactivity, it is clear that layoffs are the main cause of the decline in employment, as the number of unemployed people increased by a roughly similar amount. What's more, this type of move is atypical for January, suggesting that we are experiencing genuine job cuts and not a seasonality-driven move.

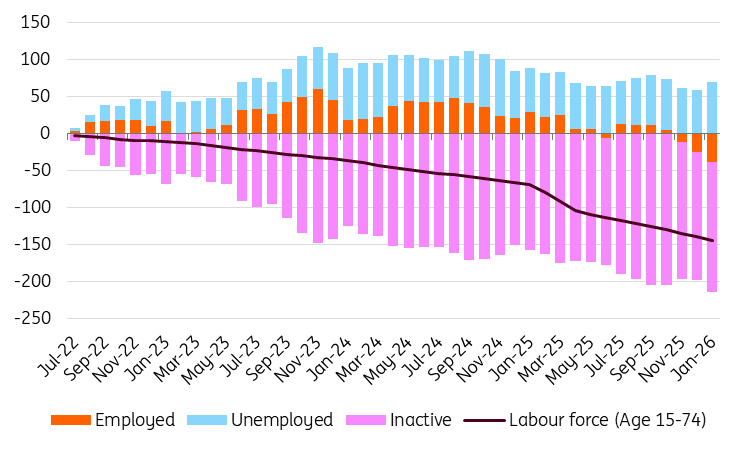

Changes in the labour market since mid-2022 ('000, 3-m moving avg)

Looking at the broader picture, a more serious problem is looming in the Hungarian labour market. Employment has fallen to a four-and-a-half-year low, and unemployment is at its highest since summer 2020. Compared to the labour market peak in mid-2022, the working-age population has fallen by 144,000 due to a population decline. This exceeds the total population of Hungary's fifth-largest city. Meanwhile, the number of unemployed people has risen by around 70,000 during this time span.

As both the demand and supply sides of the labour market have recently declined, the activity and employment rates have remained stable. While the labour market therefore remains tight in terms of ratios, this masks the negative changes taking place beneath the surface. The demographic situation is reducing the number of available workers, while companies are trying to manage significantly rising wage costs in a stagnating economy, knowing that the quantity and quality of available workers is constantly deteriorating in terms of geography, skills and age.

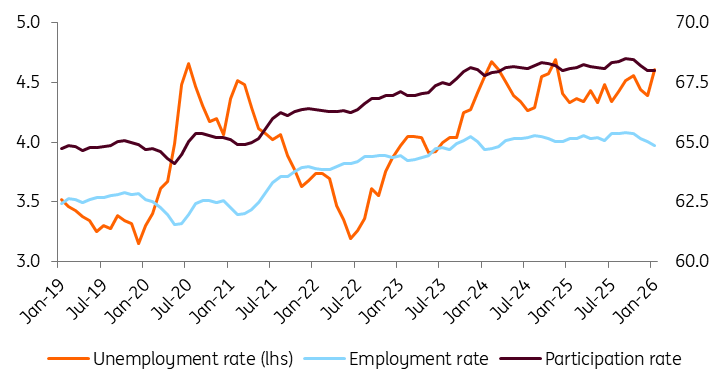

Historical trends in the Hungarian labour market (%)

Looking ahead, we do not anticipate any significant changes to the supply side of the labour market. There are no signs of a demographic shift, and rising labour costs and the lack of a sharp economic turnaround may further dampen labour market demand. While it may be early to draw far-reaching conclusions from one month's data, it appears that companies have begun rationalisation ahead of schedule. In other words, they did not wait until the end of the first quarter of this year to assess the performance of their own businesses and the national economy. It is quite possible that the decline in business confidence will accelerate in the coming months, leading to a further decline in employment.

In light of the latest data, we are revising our labour market forecast. The previous forecast predicted an average unemployment rate of around 4.4% for 2026. However, due to the weak start to the year, we think that the rate will be closer to 4.6%. While the new productive capacities from FDI is a downside risk to that ratio, a weaker-than-expected economic performance in the coming months could push the rate even higher.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more