- Quick take

- 15 October 2025

- Poland

Cooling inflation opens door to more rate cuts in Poland

Headline inflation remained at 2.9% year-on-year in September as easing food price growth offset a less pronounced drop in fuel prices compared to August. The disinflationary trend gives policymakers room to ease monetary policy further. We expect rate cuts to continue in 2026, but do not exclude a 25bp cut in November

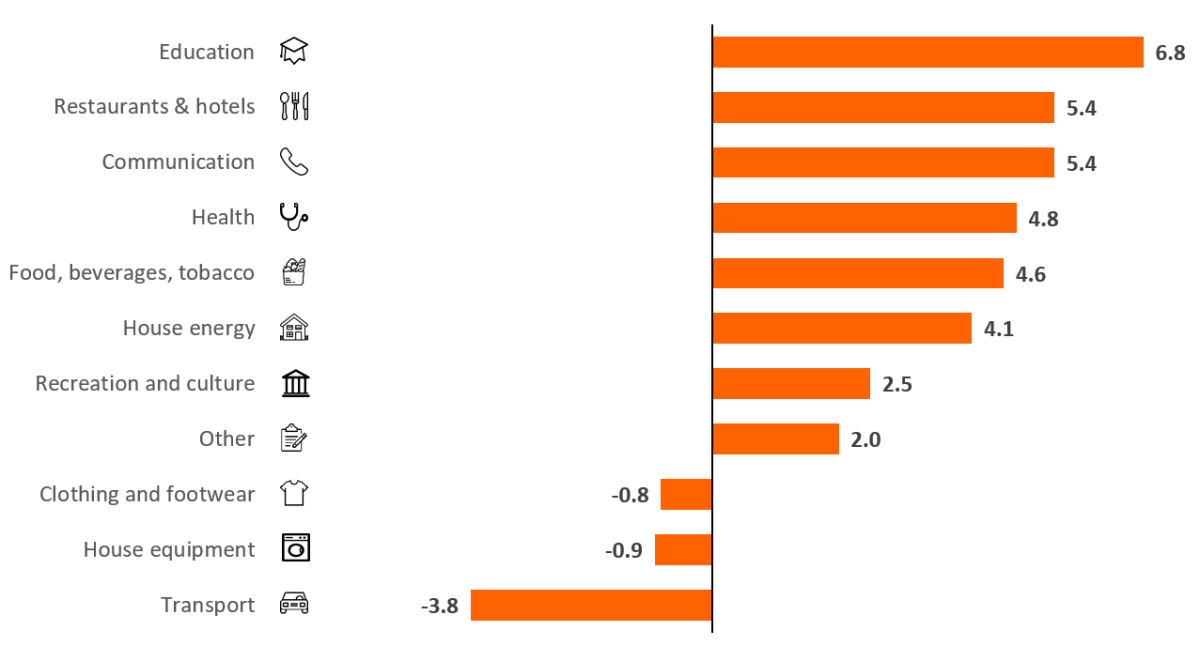

The flash estimate of September CPI inflation at 2.9% YoY was confirmed by the final data. Prices of goods went up by 1.9% YoY and prices of services advanced by 5.8% YoY, compared with 1.7% and 6.0% increases reported in August. Annual inflation remained unchanged vs. August (stable at 2.9% YoY) as a slower YoY increase in food prices compensated for a shallower YoY decline in gasoline prices. Compared to August, substantial price drops were reported in the case of fruit (-3.7% month-on-month) and vegetables (-2,2% MoM). There was also a decline in services prices (-0.2% MoM), which was partly facilitated by falling prices of tourism packages (-4.0% MoM) and cheaper transport services (-12.4% MoM).

Consumer prices were stable in MoM terms for the second month in a row. Food prices went down by 0.5% MoM and fuel prices were 0.4% MoM cheaper. At the same time, central heating prices jumped by 1.1% MoM in September and the upward trend is likely to continue as authorities unfroze prices in July. Price growth in core categories eased to 0.2-0.3% MoM in recent months from 0.4-0.6% MoM seen at the beginning of this year. We estimate that in September, core inflation (excluding food and energy prices) moderated to 3.1% YoY vs. 3.2% YoY reported in August.

Disinflationary trends are visible in the Polish economy and in the coming months, headline inflation should continue running within a 2.5-3.0% YoY range, i.e. close to the National Bank of Poland's target of 2.5% (+/- 1 percentage point). The beginning of the new year will bring a higher excise duty on alcohol and tobacco and a hike in sugar charges. At the same time, administrative prices of electricity for households are expected to be reduced, however distribution charges may increase somewhat. In 2026, we see inflation close to the central bank target, which means that there is still room for further interest rate cuts. The upcoming data releases and the new macroeconomic projection from the NBP's staff may convince the Monetary Policy Council to cut rates already in November, but this is not our baseline scenario. We expect policy rates to be kept on hold this year and the MPC to resume its “cycle of adjustments” to the policy stance in 2026. At the end of next year, we see the main policy rate at 4.00% vs. 4.50% currently.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more