- Quick take

- 1 June

- Poland

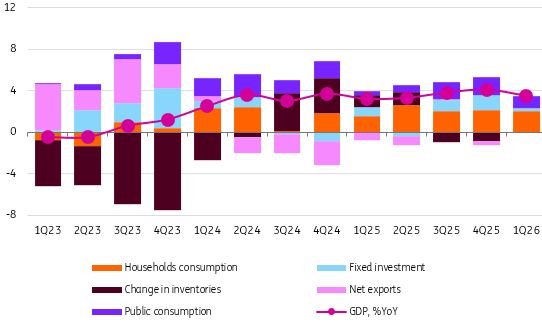

Early-year slowdown, but Poland still poised for robust 3.4% growth in 2026

Poland’s economic growth slowed to 3.5% YoY in the first quarter, from 4.1% YoY in the final months of 2025. Private consumption eased amid weaker wage growth, while investment was hit by harsh weather disrupting construction. We expect investment to pick up on EU funds, with GDP rising by 3.4% this year

In 1Q26, GDP growth eased to 3.5% YoY from 4.1% YoY in 4Q25, reflecting slower growth in both private and public consumption as well as weaker investment. Seasonally adjusted data indicate that growth slowed down to 0.6% QoQ from 1.0% QoQ in the previous quarter.

Domestic demand increased by 3.7% YoY and was driven primarily by household consumption, which rose by 3.3% YoY, down from 4.3% YoY in 4Q25. Wage growth in the economy slowed to 6.7% YoY in 1Q26 from 8.5% YoY in the final quarter of last year. Combined with stable inflation, this implies further deceleration in real labour income growth.

Public consumption rose by 6.0% YoY, compared with 7.7% YoY in 4Q25. Investment increased by 2.4% YoY, a slower pace than in 4Q25 (6.6% YoY). Past interest rate cuts and the inflow of European Union (EU) funds, under the National Recovery Plan (NRP) and structural funds, provide ongoing support for investment activity. However, in 1Q26, construction projects were postponed due to adverse weather conditions, and local government investment activity was weak.

Regarding inventory changes, they were neutral for GDP in the first quarter of this year. Foreign trade also made a neutral contribution to annual GDP growth in 1Q26, as the trade surplus was similar to a year earlier. Exports of goods and services increased by 5.6% YoY, while imports rose by 6.1% YoY. Both export and import prices continued to decline.

The start of the year brought a moderation in economic growth, but we still expect GDP to grow by 3.4% in 2026, compared with 3.6% in 2025. We forecast that private consumption growth slows to around 3.0%, from 3.7% a year earlier, due to easing wage growth and likely less buoyant spending on durable goods amid uncertainty related to the situation in the Middle East and higher fuel prices, which limit the scope for other expenditure.

A shift in savings behaviour could mitigate the slowdown, but a turnaround in the savings rate, which has been rising in recent quarters, appears unlikely given elevated geopolitical uncertainty. Stronger investment activity should support GDP this year. We expect fixed investment to increase by close to 8% in 2026, driven by the absorption of National Recovery Programme (NRP) and EU cohesion funds. We anticipate a significant improvement in investment dynamics and robust growth in the remainder of the year.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more