- Quick take

- 30 April

- Japan South Korea

Middle East disruptions hitting economic activity in South Korea and Japan

March industrial production data from South Korea and Japan showed halts in petrochemical and refinery activities. We expect this to weigh on economic growth in the current quarter, but negative impacts should be mitigated by fiscal support and strong chip activity

| 0.3% |

Korea: Industrial production% MoM, sa |

| Lower than expected | |

Korea: Output declines in refinery and semiconductor sectors

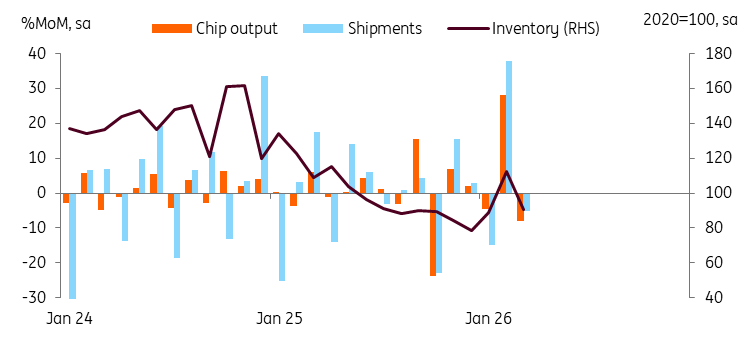

South Korea’s industrial production rose 0.3% month-on-month, seasonally adjusted, in March (vs 5.3% in February, 0.6% market consensus). Oil disruptions are one reason, but a technical payback after a strong gain in February probably contributed to the slowdown. Details showed that the robust output gain in transportation – cars (7.8%) and other transportation (12.3%) – offset the decline in semiconductors (-8.1%) and oil refineries (-6.3%). The production of hybrid vehicles and automotive components rose significantly. The output of container ships and aircraft parts also recorded notable growth.

We clearly see activity interruption in the petrochemical and refinery industry. Output (-6.3%), shipments (-5.4%). The utilisation rate for chemicals (-2.7%) and oil refinery (-5.2%) all dropped while inventories rose sharply 11.8%. We believe they have gone into survival mode – running the operation at a minimum level to avoid shutting down production entirely – as the supply situation worsens. We expect a sharp decline in oil supply for at least two months - in April and May - and that the weakness in refineries and related industry should intensify.

Strong chip demand will continue to boost economy

The drop in semiconductor activity was a surprise given the strong March export data. We believe seasonal adjustment could be a reason for the monthly fluctuation. The February gains were quite sharp. Thus, the March decline should be partly due to technical payback. Another reason could be that the strong chip performance is mostly driven by the price gain rather than the volume increase. Looking at the details, output dropped 8.1% (vs 28.2% in Feb), shipments also dropped 5.3% (vs 37.8%), and inventory dropped 19.2% after two months of gain. The utilisation rate also dropped quite sharply 7.2%.

We don’t think the overall weakness was due to raw material supply issues. Instead, it seems chip manufacturers are adjusting production rates to suit their own interests. Today at Samsung Electronics’ first-quarter conference call, the company stated that while advancements in AI are increasing structural memory demand, expanding supply is likely to be limited because of the time required to build new capacity. Due to concerns about supply shortages, customers are already placing orders for 2027. Based on current orders, the gap between supply and demand in 2027 is expected to grow even larger than in 2026.

Tomorrow, Korea April trade data will be released. We expect exports to grow 50% YoY. Early April data shows an 183% growth in chips and a 48% rise in petrochemical exports. Refineries pass higher input costs through to output and tight supply of chips should push up prices.

We continue to believe that strong global chip demand will support overall Korean growth, outweighing the disruption of oil supplies if the energy situation follows ING's base case scenario.

Semiconductor output dropped but only for temporarily

GDP and BoK outlook

Going forward, the negative impact of energy disruption will increase in the current quarter. But we believe that semiconductors and other transportation activities, including vessels, should remain quite strong. Meanwhile, the government’s cash payout program has just begun. The lower-70%-household income group would receive up to a $400 consumption voucher. The supplementary budget also financially supports oil importers in importing non-Middle East oil and gas. Thus, the economy can avoid a contraction in the second quarter. Recent quarterly GDP growth of 1.7% was remarkable, but it should moderate sharply to 0.2% in 2Q26. We expect 2026 GDP to rise 2.8% year-on-year. Following ING’s oil scenario, we expect the supply to improve gradually in 2Q26. However, the global energy prices are expected to remain above $90 by the end of the year.

The Bank of Korea will face difficult challenges. The strong growth rate is being driven mostly by external demand. The domestic economy is exposed to greater downside risks amid higher energy prices. However, as inflationary pressures broaden, the BoK is expected to deliver rate hikes, probably at a modest pace. We believe the BoK to hike in June and another one in 4Q26. The pace of rate hikes should be determined by developments in the Middle East and their impact on inflation.

| -0.5% |

Japan: industrial production%MoM, sa |

| Lower than expected | |

Japan: Retail sales offset weaker-than-expected industrial production

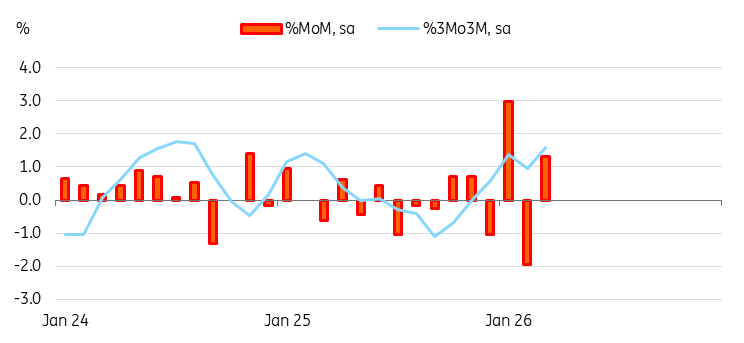

Similar to Korea’s IP data today, Japanese industrial production was weaker than expected. IP unexpectedly dropped by 0.5% in March (vs 1.1% market consensus), following a 2.0% drop in February. Output and shipments of chemicals, petroleum, and coal products fell, while electronic parts and devices increased.

However, the production forecast survey result showed that manufacturers expect an increase in output in April (2.1%) and May (2.2%). Thus, we expect the oil-related industry to weigh on growth in the current quarter, but gains in chips/equipment and transportation will cushion the shock.

Meanwhile, retail sales rose sharply by 1.3% MoM in March (vs -2.0% in February, 0.6% market consensus). Retail sales increased across all major categories. The significant rise in fuel consumption (8.2%) is likely due to consumers refuelling their tanks before prices rise. Thus, we may see a sharp decline in April. The monthly gain didn’t fully offset February’s decline. But the quarterly growth accelerated to 1.6% quarter-on-quarter compared to 0.6% in 4Q25, thus it should still work favourably for 1Q26 growth.

Retail sales continue to be a driver of growth

Tokyo CPI is expected to rise firmly in April

Tomorrow, Tokyo CPI inflation data will be released. We expect it to rise to 1.7% YoY from 1.4% in March. Energy prices should rise modestly thanks to government subsidies. Amid strong wage growth, we expect businesses to pass on input cost hikes onto consumers, particularly since April is the usual month for the adjustment. Recent weakness in JPY should also add more pressure.

BoJ and market watch

Today's monthly activity data offers mixed signals for first-quarter growth. As the economy depends on domestic demand and services rather than exports and manufacturing, the slowdown in manufacturing should be offset by improving consumption. Thus, we expect first-quarter GDP to advance 0.3% QoQ, at a similar pace of 4Q25 growth.

Earlier this week, the Bank of Japan kept its policy rate steady at 0.75%. However, there is growing pressure for a rate increase amid rising inflation risks. We believe that oil disruptions will have a greater and longer-lasting effect on inflation than on economic growth. Therefore, we anticipate the BoJ will implement two rate hikes in the second half of 2026, with the first possibly happening as early as June.

As we mentioned in our earlier note, the BoJ's remaining on hold and a hawkish Federal Reserve put upside pressure on USDJPY. Intervention risks should limit the JPY depreciation to move not far above 160 level, yet it cannot be ruled out that the authorities may wait until the level reaches 165 to ensure that their intervention is effective. Pressure on Japanese government bonds (JGBs) intensified as well. We expect 10YJPY to continue to rise. We expect 10YJGB yields to rise to 2.75% by the end of 2026, along with a 50 bp hike by the BoJ. Ironically, the BoJ’s gradual hikes should put more pressure on long-maturity JGBs as markets now worry it's behind the curve and that inflation expectations may rise faster.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more