- Quick take

- 13 August 2020

- Czech Republic

Czech inflation surpasses expectations yet again

Czech inflation grinds higher as the price of tobacco, transport and alcoholic beverages rise. For the whole year, inflation is likely to be around 3%

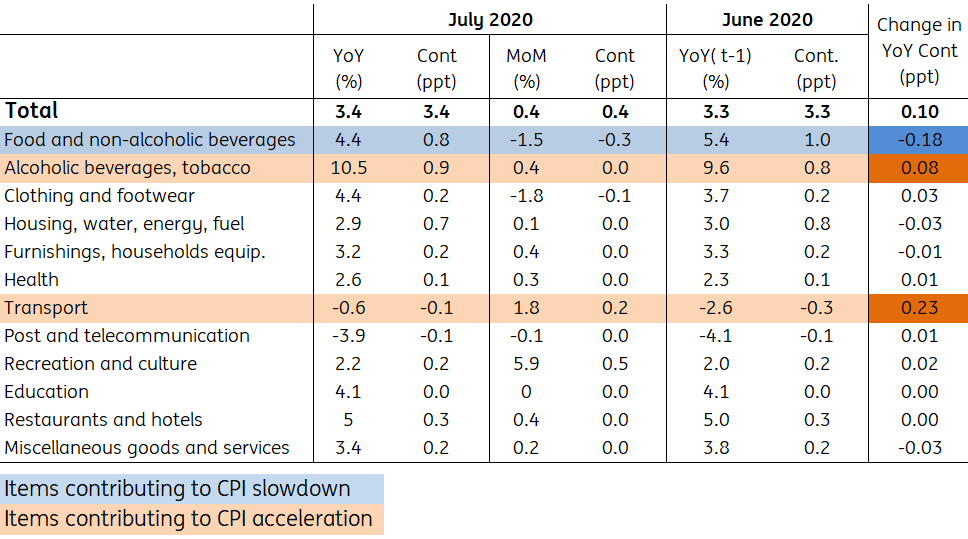

Czech inflation has surprised us again on the upside in July, and the main reasons are similar to previous months.

Firstly, the price of tobacco and alcoholic beverages further increased in YoY terms as a result of the gradual phase-in of higher excise tax. The price of tobacco rose from 12.2% to 13.8% YoY and the price of spirits increased from 8% to 10.6% YoY. A higher contribution comes also from the transport category, not only due to higher fuel prices (+4.5% MoM), but also the price of cars. Mainly, the prices of older cars increased to 8% YoY in July after stagnating at the beginning of the year, but new cars’ prices rose too to almost 4%.

Another reason for higher-than-expected inflation was holiday prices, which rose by 5.9% month-on-month.

Holiday prices have been growing traditionally due to summer months, but we expected weaker than usual MoM growth this year due to the Covid-19 crisis, leading to a slow down in inflation in YoY terms. Unfortunately, the data didn't support our view and the price of foreign holidays just decelerated by 2% YoY, and were more than compensated by higher growth in domestic holidays to almost 9%.

Also, despite the disruptions of Covid-19, the price of services keeps growing to around 3% - leading to higher than anticipated inflation dynamics.

Structure of inflation in the Czech economy

Due to higher price growth, in its latest forecast, the central bank has revised inflation upwards and expects it to remain above the 3% threshold until the end of the year.

For the whole year, it assumes inflation will be at 3.4%, which would represent the highest full-year inflation since 2008. However, according to the new forecast, inflation should slow down to 2.4% next year, but we expect a slowdown below 2%. Still, the extent to which the Covid-19 crisis impacts inflation in the coming quarters remains very uncertain.

However, falling producer prices suggests inflation should start to slow down. It is important that higher inflation is temporary and the central bank does not react to higher prices, because it remains within the tolerance band of this monetary policy cycle.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more