- Quick take

- 7 November 2019

- Czech Republic

Czech Republic: Central bank in wait-and-see mode

The Czech National Bank did not surprise today and kept the main rates unchanged, as broadly expected. The press conference was relatively hawkish again, with two board members voting for a hike as in September. Future CNB steps will be highly foreign-development dependent

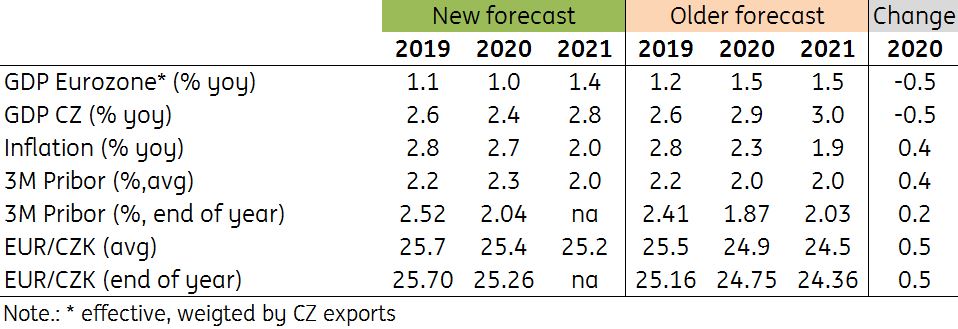

Economic growth revised downwards

As expected, the Czech GDP growth was revised downwards in the new forecast for next year, from 2.9% to 2.4%. On the contrary, inflation is higher for the next year from 2.3% to 2.7% in 2020, not only due to favourable household consumption, but also to tax increases and a weaker koruna. Indeed, the CNB has finally revised the Czech koruna to weaker levels in the new forecast and now sees EUR/CKZ remaining above CZK 25 per euro over the next two years, (25.4 and 25.2 in 2020-21), vs 24.9 and 24.5 in the August inflation report, see the table below.

Higher rates expected due to weaker koruna

Despite the weaker expectations of domestic economic growth, the new forecast expects higher CNB key interest rates in this and next quarter, ie, two 25bp hikes in the half-year horizon. However, the forecast assumes rates decline from the mid-2020. The new assumption of higher interest rates is also driven by the fact that the koruna's exchange rate has been revised and is almost 2% weaker in the new forecast in 2020 than in the previous forecast. As such, the tightening of monetary conditions is not delivered by the exchange rate and the model is pushing it over higher rates.

| 2.0% |

The main CNB rateunchanged, as expected |

Foreign uncertainty crucial

According to Governor Rusnok, the board discussion was similar to the previous one. Advocates of higher rate were arguing by overshooting the inflation target, and also highlighted some improvement in the situation abroad. On the contrary, supporters of rates stability argued that the situation abroad did not improve significantly and the slowdown in Germany is already more noticeable in domestic firms, as some companies have already started to cut production

Updated forecast

If global situation stabilizes, the CNB might deliver one prudent hike in 1Q20

As we mentioned earlier, and as the press conference suggested, further path of CNB rates trajectory will largely depend on developments abroad. We are rather sceptical about two projected CNB hikes but see a meaningful chance for a hike in 1Q20 should the external environment continue improving. On the other hand, pencilling in rate cuts in a one-year horizon seems less likely now, even if global developments does not improve enough to support hikes, in our view.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more