Czech PPI picks up but production price pressures remain subdued overall

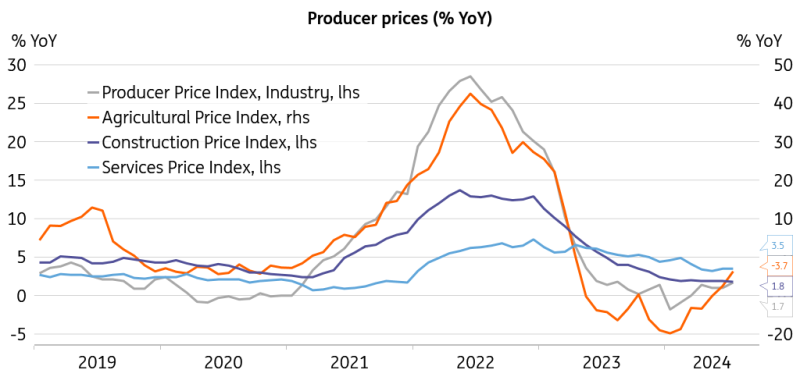

Prices in Czech manufacturing quickened and surprised on the upside in July, but the annual rate of 1.7% remained moderate. Agricultural production prices continued to fall in yearly terms while price growth in business services stabilised. The supply side does not seem to provide upward impulses for consumer inflation in the months ahead

Prices in industry driven by automotive

Czech industrial producer prices rose by 0.6% month-on-month and 1.7% year-on-year in July, exceeding market expectations. The major driver of the acceleration was the price increase in motor vehicle manufacturing, where prices gained 1.5% from a month earlier and quickened to a 4.7% growth rate in annual terms. This seems to align with some revival in the auto industry, represented also by a solid pick-up in new orders in the segment in June. The energy and water supply sector also contributed to the rebound in overall producer prices. In annual terms, prices in the industry have expanded for four consecutive months.

Production prices remain soft except in business services

In contrast, agricultural producer prices in July remained unchanged from a month earlier and shed 3.7% on an annual basis, falling for 15 months in a row. Construction work prices remained tepid, increasing by 0.1% MoM and 1.8% YoY in July, pointing to only a gradual liftoff in the building sector. Prices of services for businesses shed 1.3% from the previous month, which is attributable to seasonal patterns where prices typically fall in July. Still, the stabilisation of the annual rate at 3.5% in July points to persistency in price growth in the service sector, as July's figure remains above the average growth of 1.4% recorded between 2016 and 2019.

Supply-side price dynamic does not pose an inflationary threat

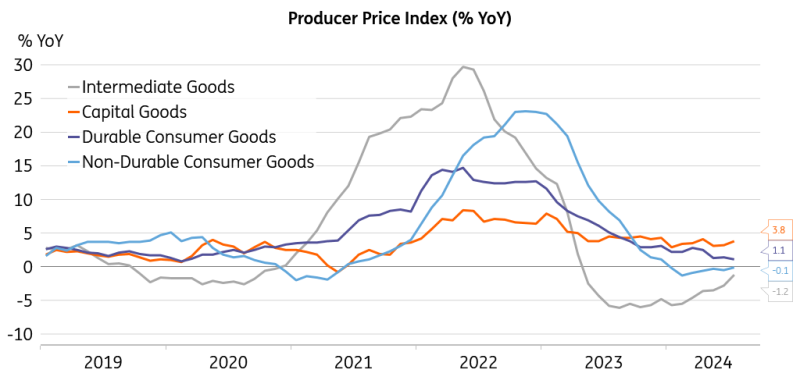

Price growth in durable consumer goods softened further to 1.1% annually in July, while non-durable consumer goods prices continued in a mild decline. Overall, production prices show subdued pressures across sectors, which is likely to limit consumer inflation in the coming months. With rather tamed price pressures in the Czech economy, lukewarm real output growth, and more risks to the recovery ahead, there is room for further easing in monetary policy conditions in the coming months. We see a 25bp cut in September and November as a realistic way forward, followed by a break in December to wait for the typically more pronounced price moves at the beginning of the year.

Production of consumer goods shows benign pricing

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap