- Quick take

Czech inflation reaches 3%, highest since 2012

- 10 April 2019

- Czech Republic

March inflation accelerated on the back of higher food, fuel and housing prices. However, we expect this pick-up to be temporary and prices should start to slow down after May. A central bank hike isn't completely off the table, but it all depends on external factors

March inflation accelerated as expected

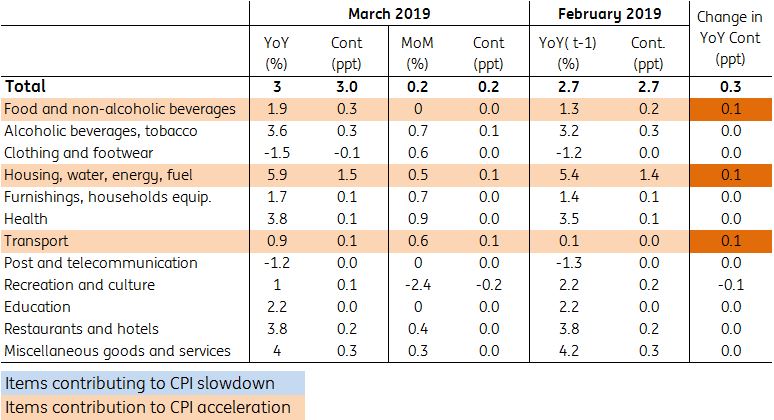

Inflation accelerated from 2.7% year on year in February to 3.0% in March, above market expectation of 2.9%. There were mainly three factors behind the price growth which include food, fuel and housing, and all items evenly contributed 0.1 percentage point to annual CPI growth compared to February.

| 3.0% YoY |

March inflationHighest since October 2012 |

| Higher than expected | |

Structure of inflation in the Czech economy

Deceleration in prices expected after May

Despite the gradual increase in oil prices, fuel prices should start to bring down annual inflation from May onwards as a result of the high comparison base of last year. Since May 2018, gasoline prices crossed CZK 32 per litre, while in June they went above CZK 33 per litre, where they mostly remained until the end of the year. However, core inflation should slightly come down in the second half of 2019 but still, remain above 2%.

Inflation is mainly being pushed by services

In general, the prices of services are mainly pushing inflation higher this year. Although they represent only 35% of the consumer basket, they are soaring this year. In January and February they increased by 3.9% YoY, and just slightly decelerated to 3.7 % in March due to marginally weaker prices of package holidays which slowed down at the end of the winter season. House price growth is the main culprit here, which accelerated by 6 % this year contributing by 3% inflation by 1.5ppt, i.e. by half.

Central bank hike remains on the table

March inflation hit the upper-tolerance band of the Czech central bank's inflation target, and is the highest level since October 2012. Though the Bank won't feel nervous as 3% inflation should only be short-lived, the inflationary outlook would justify another rate hike, especially as the koruna won't be appreciating as fast as the central bank expected.

However, to see a hike in May, we'd need to see some calm in foreign risks in the weeks ahead, which has been the primary reason behind the central bank's 'on-hold' decisions in the last few meetings. Having said that, a May hike still remains on the cards.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more