- Quick take

- 10 December 2019

- China

China November CPI peaking

Inflation in China in November rose further to 4.5%YoY, but there are clear signs that it is peaking

| 3.8% |

November Pork price increaseLowest monthly increase since June |

It may be high, but it won't stay high

Newswires running headlines like "China November inflation highest since 2012" entirely miss the point. Inflation in China has been driven higher by rising pork and consequently other meat prices. This is fallout from the African Swine Fever (AFS) epidemic that has killed half of the hog population in China.

In November, pork prices rose 3.8%MoM. But this was way down from the 20.1% increase in October, the 19.7%MoM increase in September, and the 23.1% increase in August. In fact, it was the lowest increase since June (3.6%MoM).

The reasons for this moderation are various but include:

- Higher pork imports, including from the US alleviating supply shortages

- Mobilisation of the strategic pork reserves (frozen pork warehoused for emergencies)

- A decrease in new reports of African Swine Fever (AFS) and rebuild of stocks

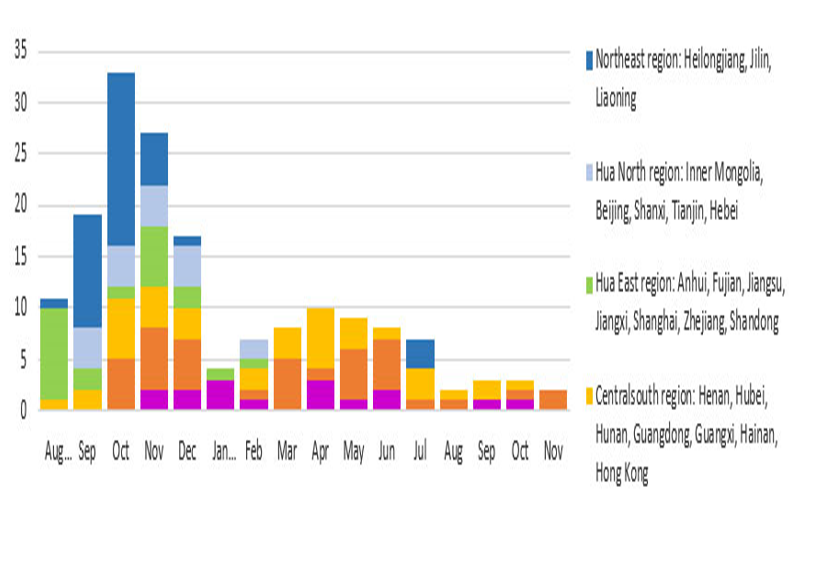

Number of African Swine Fever reported villages by region by onset month* in China

The peak of the epidemic has passed

The chart above, taken from a UN report just five days ago, highlights that the peak of the AFS pandemic has passed. Pork prices may even start to decline next month, and in the coming months, dragging down other meat prices along the way. Inflation rates should now have peaked, and the coming months will see measured inflation drop steadily.

More than that, household spending will get a lift from the additional purchasing power following the decline in meat prices, which will provide a broader lift to the domestic economy at a difficult time for the economy.

There are no specific policy implications from this. The improvement in purchasing power reduces the urgency of additional supportive fiscal measures, and the People's Bank of China was, in any case, looking through this food price spike in terms of its monetary policy settings, so it does not need to shift its stance.

Possibly, the improvement in China's domestic food situation reduces the incentive to give more ground in trade talks with the US, especially in terms of commitments to buy agricultural produce. Though there may be broader reasons for making concessions to secure tariff rollbacks. The next few weeks should provide greater clarity on that.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more