- Quick take

- 30 June 2023

- China

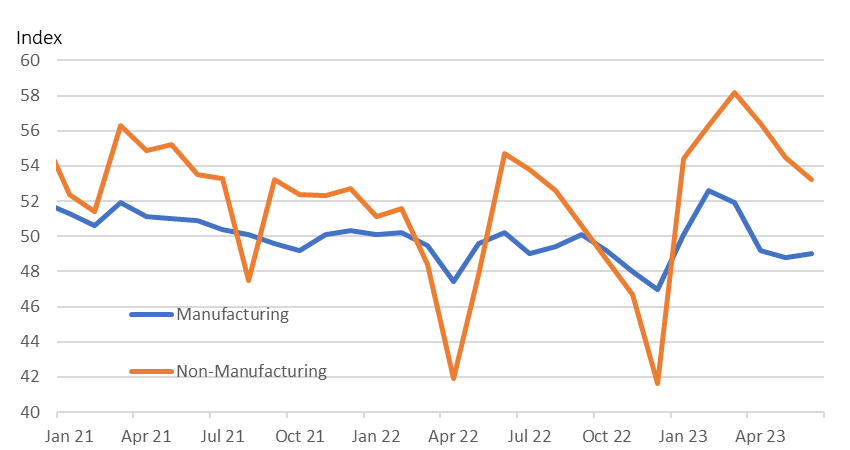

China: Non-manufacturing activity slows

Official PMI data confirm that the re-opening surge in the service sector is subsiding

| 53.2 |

Non-mfg PMI indexDown from 54.5 |

| Lower than expected | |

The main engine of growth is spluttering

Apart from a short-lived bounce in the manufacturing sector after the zero-Covid measures were shelved in early December 2022, China's manufacturing has been limping along. The official PMI index for the manufacturing sector (which tends to focus on larger, state-owned enterprises) has been below the breakeven 50 level since April. It was not much of a surprise to see it stay in this area in June, though perhaps the fact that the contraction is relatively stable is a source of some comfort. At least things aren't getting noticeably worse.

Instead, it has been the non-manufacturing sector, buoyed by consumer spending, that has been keeping China's economy growing in the first half of this year. But what this data confirms, which we already suspected, is that the initial surge contained a lot of pent-up demand. Domestic tourism, and dining out have been making up for lost time in the early part of the year. But there is only so long that this can go on. Other indicators of retail sales suggest that it remains well above historical trends, and suggests some further moderation over the second half of this year.

Looking at the breakdown of the surveys, there are no particular standouts. Most sub-indices are declining in both manufacturing and non-manufacturing surveys. This includes new orders, new export orders and employment.

Caixin PMI data due early next week will provide more insight into smaller and more export-oriented firms.

China PMI data

PMIs support our GDP downgrade

These latest data provide further support for GDP downgrades for the second quarter. They also support the idea that the second half could see weaker support from the service sector. We will be publishing new GDP forecasts next week for China, and these look highly likely to show a cut to the existing full-year GDP figure of 5.7%, and likely take the forecast below the existing consensus forecast of 5.5%. We may still just sit on the right side of 5.0% - the government's target for this year - but that only goes to show what a low hurdle 5% was to achieve after last year's 3% outcome.

The market continues to fixate on the possibility of stimulus measures, and in due course, we do expect the government to step in and provide some support. However, we remain unconvinced that this will resemble anything like the financial bazooka that some want to see, but will instead be more of a buck-shot spray of smaller more targeted measures that may not move the GDP needle substantially.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more