China: January PMI edged up but remained in contraction

Manufacturing PMI data came in slightly below forecasts, indicating a soft start to the year

| 49.2 |

China's manufacturing PMIHigher than December 2023's 49.0 but remaining in contraction |

| Lower than expected | |

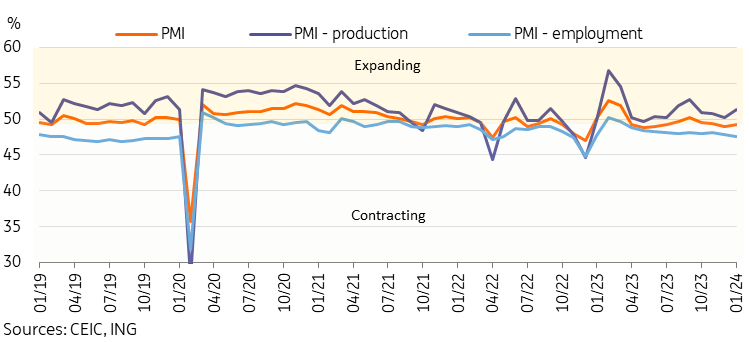

PMI edged up slightly, showing a smaller contraction

We got our first look at China’s 2024 activity data with the January manufacturing PMI. The headline number of 49.2 was slightly weaker than our forecast of 49.5, but trended in the expected direction, up from 49.0 in Dec 2023.

The Chinese manufacturing sector remains under pressure amid a weak domestic recovery and poor external demand. The manufacturing PMI has been under 50 for 9 of the past 10 months.

Small uptick in new orders, but still in contraction

New orders and employment remained in contraction while production remained the lone bright spot

By subcategory, new orders edged up from 48.7 to 49.0, while new export orders rebounded from the low of 45.8 to 47.2. New orders have contracted for 4 consecutive months, while new export orders have contracted for 10 consecutive months. The employment subindex fell to a 13-month low of 47.6 and has remained in contraction for 11 consecutive months. On the brighter side, production notched a 4-month high, up from 50.2 to 51.3, staying in expansion for 8 consecutive months. The purchasing price index subcategory dipped from 51.5 to 50.4, but remained above 50 for the seventh consecutive month.

Production remained the bright spot while employment reached a 13-month low

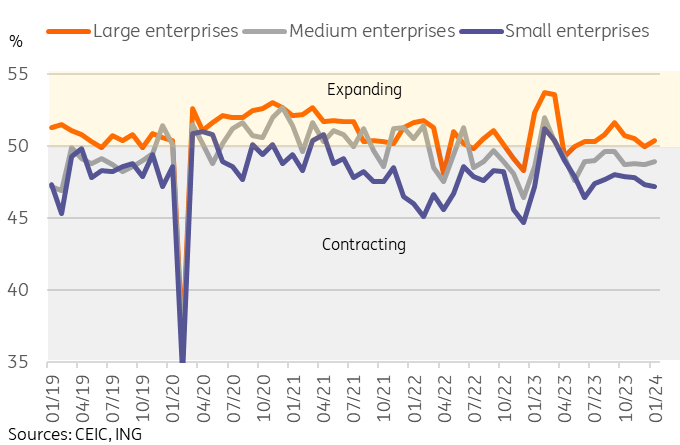

Large enterprises continued to outperform medium and small enterprises

China’s post-Covid economic recovery has been uneven, with a significant divergence seen in the trajectory of different-sized enterprises. Large enterprises' PMI has been at 50 or higher for 12 of the past 13 months and remained in expansion to start 2024 at 50.4. However, medium and small enterprises have remained in contraction for 10 consecutive months.

Large enterprises have consistently outperformed since the pandemic

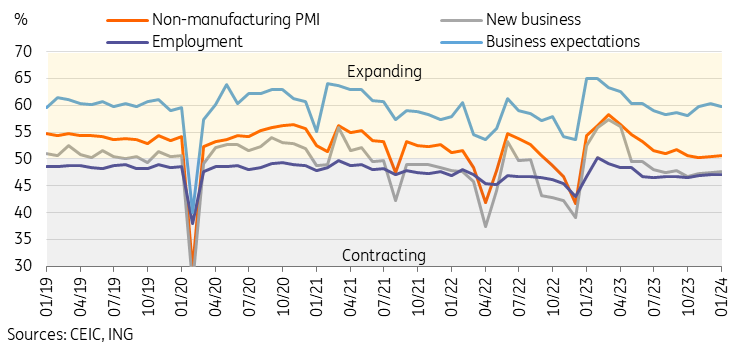

Non-manufacturing PMI continued to outperform, but sub-indices present a case for caution

The January non-manufacturing PMI came in at 50.7 to start the year, up from 50.4 in Dec 2023. Services have outperformed manufacturing over the past year in China, which is not a China-specific but rather a global phenomenon. While the headline numbers still look relatively healthy, the sub-indices have presented a cause for caution in past months, with new business and employment remaining in contraction for 9 and 11 consecutive months respectively.

China non-manufacturing PMI remained in expansion

PMI indicated that 1Q may be off to a soft start

Overall, the PMI data shows that China’s economy remains relatively soft, as confidence remains weak. Until forward-looking indicators such as new orders return to expansion, economic momentum is likely to remain tepid. Employment remaining in contraction in both the manufacturing and non-manufacturing surveys also indicates that the job market remains weak, which will continue to be a headwind to consumption.

While we have seen numerous piecemeal supportive policies targeting specific sectors released over the past few months which have helped stabilize growth somewhat, markets are looking ahead to the Two Sessions in anticipation of a larger-scale policy package. The larger-than-expected 50bp RRR cut last week could be seen as a signal of more significant supportive policies ahead.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap