- Quick take

China: Further rate cuts and weak activity data

- 15 June 2023

- China

After the rate cuts yesterday, the 1Y medium-term lending facility (1Y MLF) was cut 10bp today. Weak activity data mean that this is probably not the end of the stimulus, though the more important measures are likely to be fiscal

| 2.65% |

1Y MLF-10bp |

| As expected | |

1Y MLF cut 10bp

After the cut of the 7-day reverse repo rate by 10bp yesterday, it was no surprise to see the 1Y MLF rate also cut by 10bp, taking it down to 2.65%. Lending volumes also rose to CNY237bn, above the CNY200bn expected. Still, this is not going to move the needle for Chinese activity particularly. More easing will be needed, and though there does look like a good case for further monetary policy easing in the months ahead, the bulk of the authorities' response will probably need to come from targeted fiscal measures.

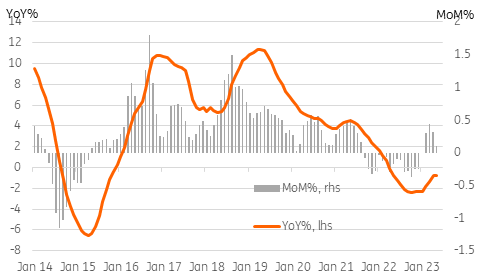

New home prices still rising, but only just

Ahead of the bulk of the activity data, new home prices showed a fifth consecutive month without falling. Though the rate of increase was only 0.1% MoM, which is down on the recent trend and may indicate momentum slowing in this part of the economy.

70-city new home prices

Activity data was very weak

The main body of activity data can be summed up in one word. Disappointing.

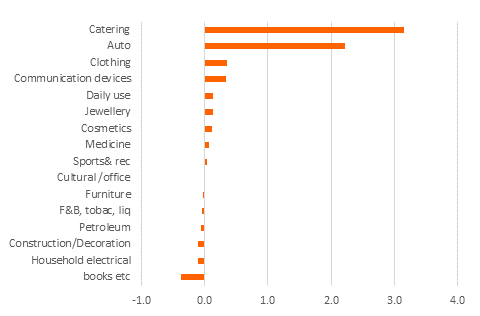

Retail sales is the figure we have been focussing on, as it is at the moment, the only functioning engine of Chinese growth. And although the year-on-year growth rate of 12.7% looks impressive, this equates to a seasonally adjusted decrease in month-on-month sales and shows that the re-opening momentum is falling.

Breaking the numbers down to look at what is driving growth, and catering is still the major driver, which won't do a lot to boost domestic production and manufacturing, though it does lift GDP. Vehicle sales is the only other notable contributor to growth, after which very little else is showing much signs of life, including consumer confidence bellwethers, like clothing.

Industrial production rose 3.5%YoY, though this was well down on the 5.6% rate of growth in April, and the year-to-date growth figure was unchanged at 3.6%.

Urban fixed asset investment slowed from 4.7% to only a 4.0% pace, which may illustrate the problems local governments are having trying to boost growth in the absence of cash from land sales. Some more central government support may be of help here if it is forthcoming.

Also, property investment continues to weaken and is now falling at a 7.2%YoY pace, down from -6.2% in April. We had been hoping for more of a flat line from property development in China in 2023 after what we calculate was about a 1.5pp drag on GDP growth in 2022. It could be worse than this.

Contribution to year-on-year retail sales growth

Outlook for the CNY is negative

There will doubtless be more support measures coming in the days and weeks ahead. And in anticipation of these, markets may rally. But the underlying story on the economy is extremely disappointing right now, and that suggests that apart from periods of temporary stimulus-generated relief, we should anticipate markets remaining soft in net terms.

The CNY gapped higher ahead of the data today, and there is nothing in the numbers that suggests that this gap should be closed. Our recently revised CNY forecasts already look out of date. 7.20 could be reached in days. And though the authorities will be keen not to see the currency weaken in an uncontrolled fashion, they will surely regard a weaker CNY as one of the policy tools they will need to lean on to help the economy out of its current state of weakness.

We will be returning to those CNY forecasts shortly. The profile will undoubtedly be raised further, and the turn probably pushed out too.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more