China’s exports and imports contracted in October

China experienced a contraction in international trade in October amid falling demand in Europe and the US. Exports should continue to be weak into mid-2023

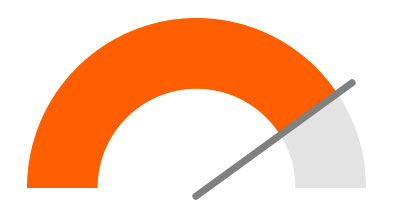

| -0.3% |

Exports (year-on-year) |

| Worse than expected | |

| -0.7% |

Imports (year-on-year) |

| Worse than expected | |

Weak export and import trade in October

China's exports contracted 0.3% YoY while imports contracted 0.7% YoY in October. This is the first contraction in international trade since May 2020.

- Exports to Europe fell 6% in a month, with an even deeper fall of 7.4% MoM for exports to the US. Exports to ASEAN fell 6.5% MoM. This is not seasonality in play as exports fell 9% YoY to Europe and 13% YoY to the US.

- However, export growth to ASEAN was up 20% YoY while imports rose 4.5% YoY, signalling a continuous shift in the supply chain from Mainland China to ASEAN.

- Electronic products was the biggest trade item, contracting by 7% MoM and by -0.73% YoY.

- Imports painted a similar picture. But imports of electronic products fell faster at 11.7% MoM and -7% YoY.

We can blame the Golden Week holiday in China for the monthly contraction in exports and imports but the holiday does not have any seasonal effect on the year-on-year data. As such, the contraction in international trade activity in October stems from other factors.

Covid cases started to climb in October but have affected factory activity only slightly, and there were no cases found in ports. So we can rule out shipment delays as a factor in the contraction. Inflation in Europe and the US continued to be high, which could be a factor. Slower imports of electronic products paint a similar picture. If this is the reason for the contraction in China's international trade in October then we should expect the contraction to continue as our economists covering Europe and the US project a recession in these two economies.

Deeper electronic import contraction shows global economic weakness

Another observation from the data is that ASEAN stood out as a source of growth for imports, which shows that the supply chain of China-ASEAN continues to build. We observe at least three patterns: China-ASEAN-China exports, ASEAN-China exports and China-ASEAN exports. This means China and the rest of Asia have become increasingly integrated in international trade.

This set of data shows a bigger trade surplus in October compared to September and is therefore supportive to GDP growth. Our GDP forecast is 3.3% for 2022.

China and ASEAN form supply chain

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap