- Quick take

CEE January PMIs: Positive figures despite supply chain issues

- 1 February 2021

- Czech Republic Hungary

The Central and Eastern Europe region posted solid PMIs in January confirming the ongoing recovery and improving conditions in industry. However, supply chain disruptions are mounting in the region, which might slow the recovery

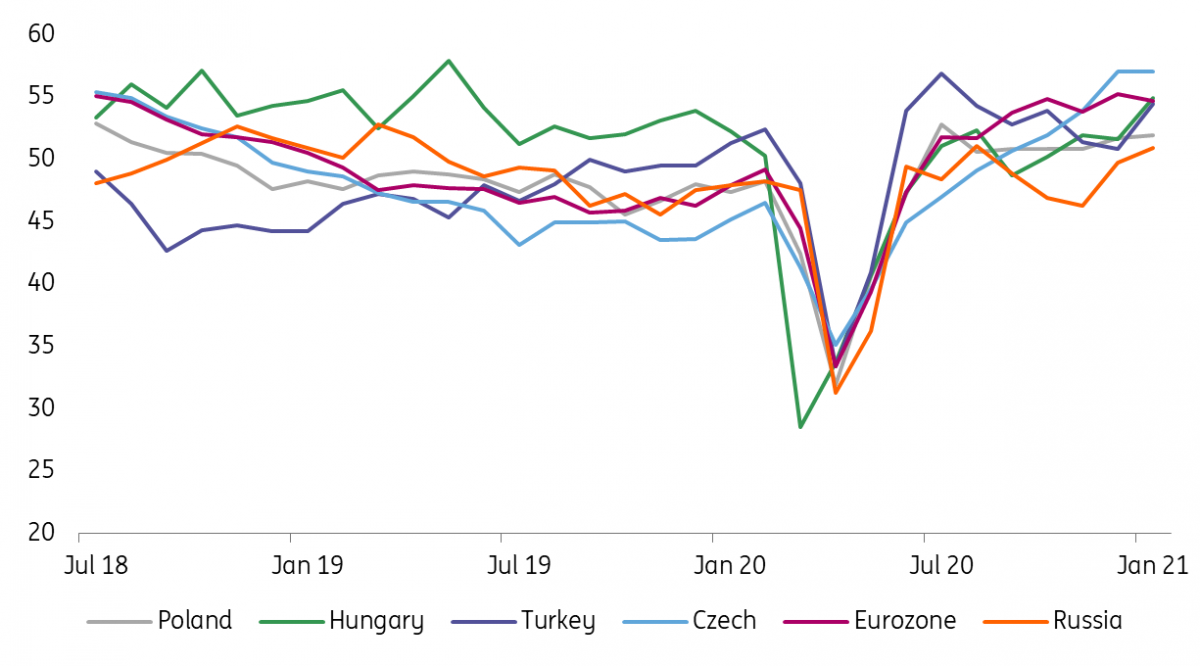

As the eurozone and German manufacturing PMIs fell slightly in January, the market also expected some slowdown in the CEE surveys compared to the readings at the end of 2020. However, the figures broadly improved and surprised the market on the upside. Czech PMI stagnated at 57 points, Hungary and Turkey surprisingly increased above 54, Poland was at 52 points and Russian was again above the 50-threshold. Still, problems in supply chains are mounting and delivery times are increasing, signalling that even industry is facing challenges related to the pandemic, which might weaken the recovery in the months ahead.

Czech Republic: Supply chain disruptions mounting

The Czech manufacturing PMI stagnated at a solid 57 points, while the market expected some slowdown towards 55.5. Firms in the survey reported an increase in production and new orders, and optimism about future production increased. On the other hand, delivery times deteriorated significantly, being the worst since April 2020. This caused an increase in input prices, which rose at the fastest rate since March 2017. Companies either did not pass these through to clients, or did so only partially, but output price inflation was still the second fastest since the end of 2019.

All in all, this was a positive figure but problems in supply chains are mounting and the biggest Czech automaker announced a temporary partial shutdown last week. As such, this should weaken production somewhat in the weeks ahead and slow the ongoing recovery. Also, delayed supply deliveries are pushing the PMI higher as the methodology considers this to be an increase in demand. This means, that the situation in industry is less rosy than the PMI indicator itself suggests, though it remains solid so far given the pandemic situation.

Hungary: Surprisingly strong PMI might be driven by reopening hopes

Hungary's manufacturing PMI surprised on the upside in January. The 54.9 point reading is the highest since mid-2019, suggesting an excellent expansion in the sector. Considering the bad news from car manufacturing, which was related to supply chain disruptions, shutdowns and dropping shifts, this January reading is even more puzzling.

The details provide some explanation however. From an economic activity point of view, the most important sub-index, the production volume index, fell but was able to remain in expansion territory. It seems that other sectors outside of car manufacturing are doing well. This idea is supported by the purchased inventories sub-index, as purchased inventories showed a strong increase. This could reflect an expected jump in demand in the near future, as manufacturers prepare for reopening. New orders also rose from the previous month, remaining in expansion territory, supporting the idea of a reopening boost. In parallel, the employment index showed an expansion too, after dropping below the 50-point threshold in the previous month. Supply chain issues affected only the delivery times, which were longer than in December. In all, despite the upside surprise in the soft indicator, the issues in car production (to the sector’s share in industry) could have a dampening effect in the whole sector in January, so we’d take today’s PMI data with a pinch of salt.

January PMIs in the CEE region above expectations

Poland: Sentiment in manufacturing improved in January

Poland's manufacturing logistics managers improved their assessment of the economic climate. In January, the PMI index increased to 51.9 points, the second highest level since July 2018. The market expected a mild decline to 51.3, we assumed a stabilisation at 51.7. Despite the prolonged lockdown, sentiment in manufacturing remains relatively good. This was also shown in other surveys.

PMI components point to a second consecutive increase in new orders, with stronger exports than domestic demand. Backlogs and material inventories are also rising, firms continue to report limited capacity and staff shortages, also due to workers in quarantine. This is generating demand for new workers. Material shortages and supply chain disruptions are also resulting in rising cost pressures - in January they reached their highest level since April 2011.

Polish manufacturers expect production to increase once the pandemic is contained. We also believe the sector will remain healthy. In the course of the year, as further restrictions are relaxed, services will also begin to recover.

Russia: Producers back to cautious optimism

Russia's manufacturing PMI re-entered positive territory in January with a 50.9 result after a temporary drop below the key 50 level in 4Q20. The performance seems to be in line with the manufacturing recovery seen at year-end, which allowed positive manufacturing growth of 0.3% for the full year, driven mostly by consumer-focused sectors. At the same time, the optimism among producers may be challenged by the year-end drop in consumer confidence amid apparent pressure on income growth in the private sector. In addition, the expected fiscal consolidation is also a factor that might limit the pace of industrial recovery in 2021.

Turkey: Continuing strength in the PMI

Despite expectations of further moderation amid a gradual downtrend in the second half of 2020, the Turkish PMI jumped again to 54.4 in January, the highest level since last July, from 50.8 a month ago. Accordingly, it has remained in growth territory despite a recent policy shift by the Central Bank of Turkey, with significant tightening, momentum loss in lending and new pandemic measures in the last quarter, as Covid cases accelerate.

According to the breakdown, we see strength in manufacturing with new orders supporting production, while employment in the sector has recorded the highest increase in the last three years. A recent stabilisation in the exchange rate has also taken some steam out of input and output prices.

All in all, the PMI has strengthened to well above the 50 threshold and has remained in expansion territory since the reopening of the economy after the first wave of the Covid-19. However, the withdrawal of policy stimulus will weigh on the strength of the recovery this year, likely pushing the PMI downwards in the period ahead.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more