Weak Turkish capital flows add pressure to international reserves

While the current account deficit continued its widening path, capital flows have remained quite weak in the absence of unidentified solid inflows, and that's leading to pressure on international reserves this year

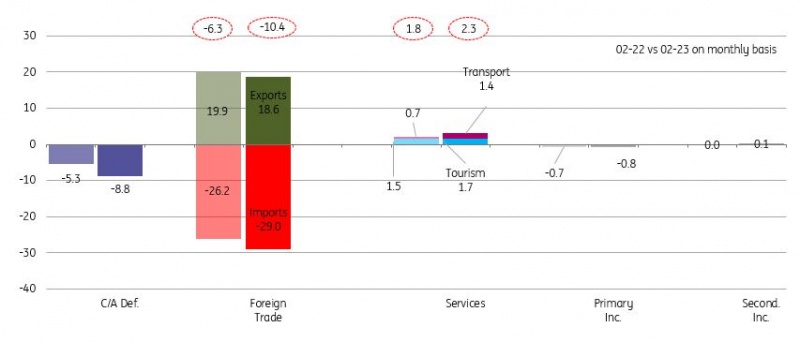

Breakdown of current account (monthly, US$bn)

After the record monthly deficit in January, we saw continuation of widening in external imbalances with US$-8.8bn in February, broadly aligned with the market consensus. Accordingly, the 12-month rolling deficit maintained widening and reached US$55.4bn (translating into around 6% of GDP). The key driver on monthly reading over the same period last year was a rapid increase in net gold trade (US$-3.8bn vs US$-0.3bn last year), while core trade that was at US$1bn surplus last year turned to US$0.8bn deficit this year.

Among other variables, net energy deficit and services income showed some improvement to US$-7.0bn from US$-5.8bn in Feb-22 and to US$2.3bn from US$1.3bn, respectively.

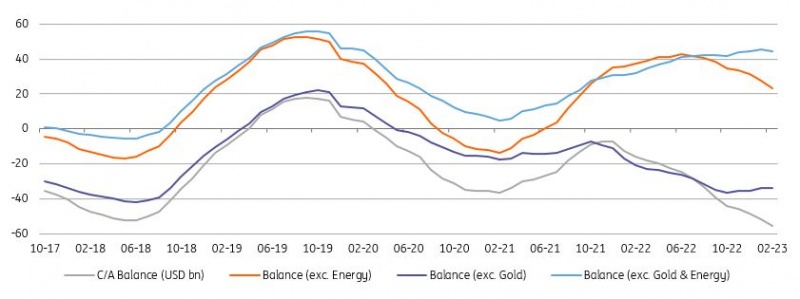

Current account (12M rolling, US$bn)

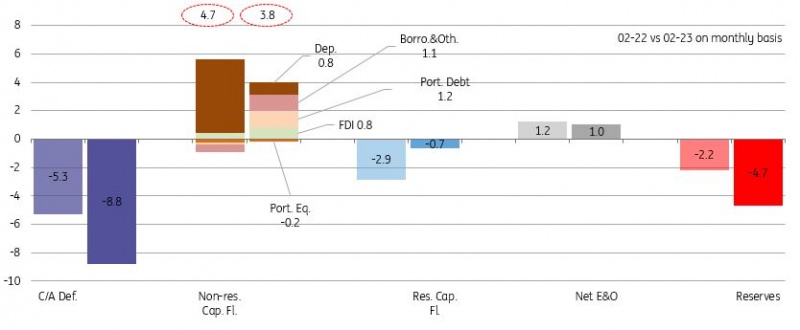

The capital account, on the other hand, has remained weak, with a mere US$3.1bn of net inflows. With the monthly current account deficit and small net errors and omissions at US$1bn, reserves recorded a US$4.7bn drop (financing roughly three fourth of the cumulative deficit this year).

In the breakdown, weighing on net monthly inflows, we saw asset purchases by residents at net US$0.7bn driven by rise in companies’ financial asset acquisitions. For non-residents, US$3.8bn inflows were attributable to:

- US$0.7bn gross FDI,

- US$0.8bn deposits placed by foreign investors to Turkish banks,

- US$1.2bn Eurobond issuance by banks,

- US$1.4bn net borrowing by banks and corporates.

Regarding the rollover rates, we saw a strong performance for corporates at 162% on a 12M rolling basis (vs 131% in February alone), while the same ratio for banks stood at 82% (260% in February).

Breakdown of financing (monthly, US$bn)

Overall, while the current account deficit remained on its expansionary path in February, the latest indicators hint at further widening in March with a continuing increase in the foreign trade deficit driven by gold trade and core imports. However, gold imports almost halved last month, the lowest since July 2022, likely due to a tightening in regulations that govern gold trade and the domestic transactions of gold.

Going forward, the impact of these regulations and domestic demand will be key for the current account outlook, while we expect the current account deficit to narrow to about 3.5% of GDP this year from 5.2% in 2022 due mainly to moderate energy prices and softer domestic demand. On the capital account, banks’ borrowing and eurobond issuance played a key role in the capital account in February. However, total flows have remained weak in the absence of strong unidentified inflows, leading to pressure on international reserves this year so far.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap