- Quick take

- 11 July 2018

- Turkey

Turkey: C/A deficit likely at its peak

The 12M rolling deficit kept widening in May, with a higher than expected monthly reading at USD5.9 billion. The good news is that early June indicators suggest that the uptrend, in place since early 2016, is likely to end in coming months

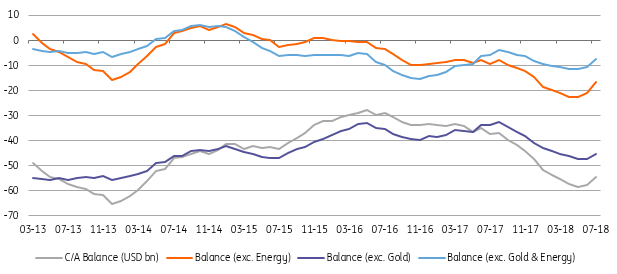

External Balances (USDbn, 12M rolling)

Tourism limits the widening in the deficit

One of the major concerns for Turkey is external imbalances, on a rising path since early 2016. The latest May C/A balance data - higher than expected at a USD5.9 billion deficit - shows further widening in the 12M rolling deficit to USD57.6 billion, its highest since the first quarter of 2014. The good news is that this is likely the peak and that it should gradually improve in the period ahead. Easing economic activity should help to curb import demand, as evidenced by early indicators in June.

The breakdown reveals that the further expansion is attributable to the continuing impact of the trade deficit, deterioration in primary income balance and the primary income balance moving to deficit despite strong services income supported by the ongoing boom in tourism

Flow outlook weakened, though corporates have raised long-term credit

On the financing front, given the increasing risk anticipation for Turkish assets, the capital flow outlook was weak. There was USD0.3 billion outflow on the back of local banks increasing their deposits abroad, broadly offset by trade credits, FDI, an increase in foreign banks’ deposit holdings in Turkey and net borrowing. Accordingly, Turkey relied on net errors & omissions at USD3.4 billion (USD14.8 billion on a 12M rolling basis) and USD2.8 billion in reserve depletion to finance the monthly current ccount deficit.

Despite volatility in local financial markets being exacerbated by political uncertainty with the call for snap elections, the corporate sector managed USD1.6 bn net long-term borrowing -translating into more than 300% rollover ratio. Banks, on the other hand, recorded close to 100% rollover ratio, both reinforcing the view that the Turkish banking and real sectors maintain their access to foreign funding.

Overall, the ongoing momentum loss in the economy and weaker TRY will likely help the trade balance recover, indicating that we may have reached the peak for the external deficit. On the other hand, the capital flow outlook has weakened, with increasing reliance on reserves and net errors & omissions that is likely not sustainable for long.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more