- Quick take

- 14 November 2018

- Bulgaria

Bulgaria: Slower growth, accelerating inflation

3Q18 flash GDP reading came in at 3.0% QoQ/YoY in line with our forecast, but below the Bloomberg median of 3.2% YoY. CPI accelerated to 3.7% YoY in October, above consensus and ING estimates

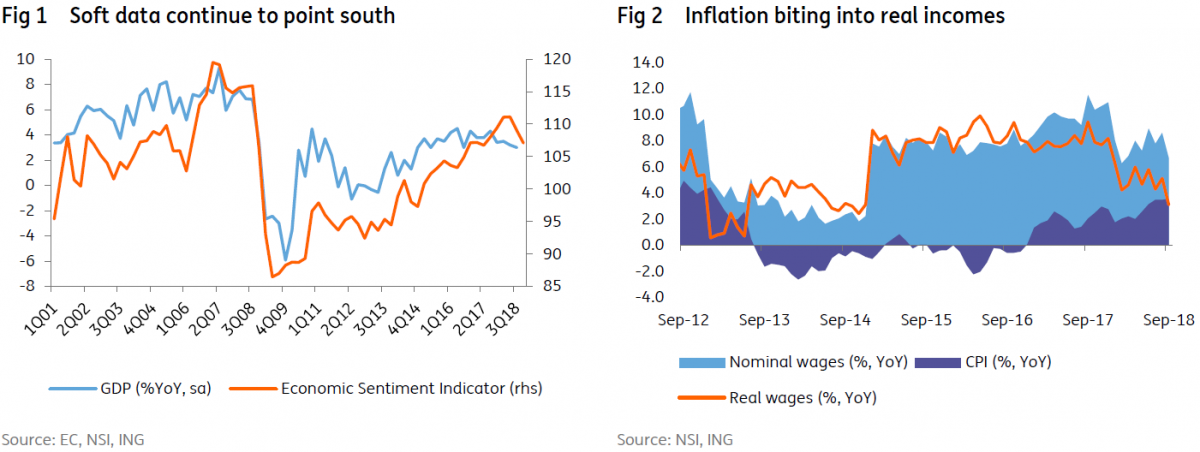

3Q18 sequential deceleration to 0.5% QoQ from 0.8% previously was not a big surprise given the dismal third quarter Eurozone GDP data, especially the reading for Germany which is the main export market for Bulgarian goods. Still, the export of goods and services and consumption are cited as the main contributors to the quarterly expansion. High frequency indicators also suggest a softer growth, with retail sales posting a quarterly deceleration, while industry contracted in the third quarter versus 2Q18. There were weaker Economic Sentiment Index (ESI) readings across the board as all three major components (industry, services and consumer) reported softer confidence in the third quarter which was also a good indication for today’s GDP release.

In annual terms, final consumption posted a mild slowdown from 7.7% to 6.9% YoY in the third quarter, as well as investments from 7.0% to 6.2%. Today's 3.0% YoY growth in 3Q18 is consistent with our full-year forecast for 2018 of 3.3%. This is a shift into a lower gear for the growth story compared with last year rather than raising any meaningful concerns.

Soft data continues to point south at the start of the fourth quarter, with ESI printing the lowest reading since Jul-17, despite the improved sentiment for industry, as services and consumer morale turned sour signalling weaker domestic demand, with inflation biting into disposable incomes. In fact, those services surveyed cited weak current and expected demand for the deterioration in sentiment, while for consumers the bleaker outlook for the financial and economic situation was cited as reasons for lower optimism, despite improving labour market prospects.

October CPI surprised to the upside, after posting a sharp 0.7% MoM rise with a few items registering eye-popping monthly jumps such as bread, gas, but also, somewhat surprisingly given the oil price developments during the month, liquid fuels. In fact, our forecast error came mainly on the back of liquid fuel prices.

Given the recent CPI numbers, the ECB’s concerns about Bulgaria sustainably meeting the inflation convergence nominal criteria seem to be materialising. After steps taken to join the Banking Union simultaneously with ERM II in 2019, the latest Cooperation and Verification Mechanism (CVM) review mentioning that the EC was “confident that Bulgaria – if it pursues the current positive trend – will be able to fulfil all the remaining recommendations and thereby the outstanding benchmarks” could alleviate some worries on institutional convergence. Still, the real convergence process is much slower than for other CEE countries due to structural limitations to potential growth, including a shrinking labour force due to ageing population and migration, but also a slower growth rate in capital accumulation.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more