- Quick take

- 10 November 2023

- Bulgaria

Bulgarian activity is weakening

New high-frequency data for Bulgaria came in today, rounding off the third quarter. The rather weak prospects suggested by this data lead us to expect a meagre 0.1% quarter-on-quarter advance in the third quarter GDP data due next week, in sync with a slowdown to 1.7% in year-on-year terms

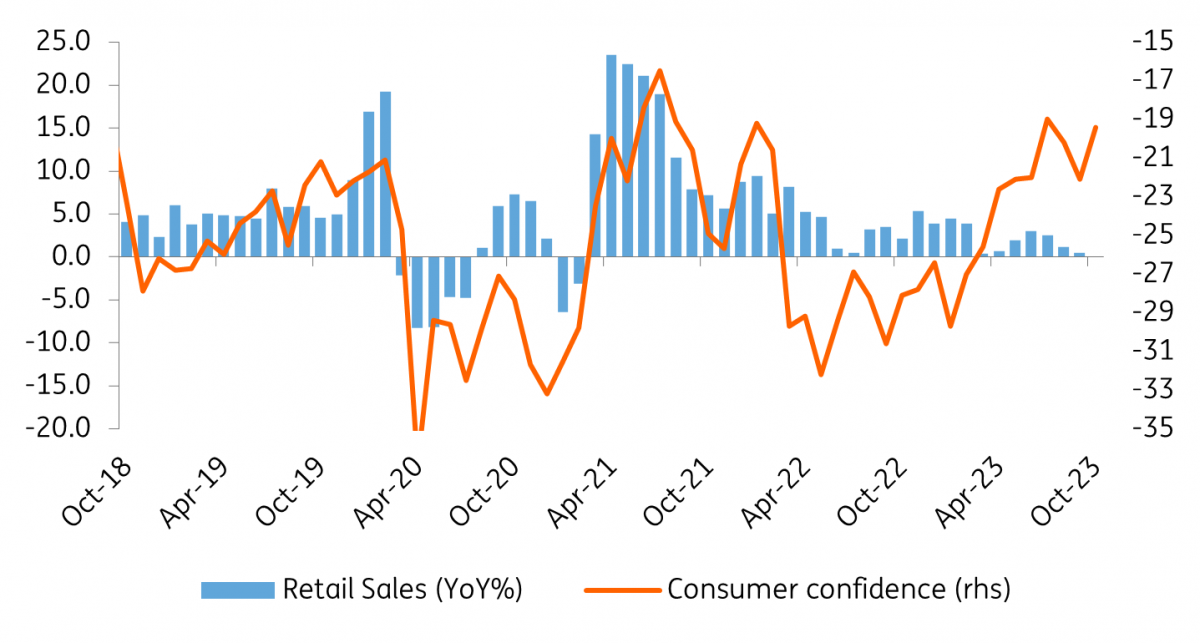

Despite the visible advance of real wage growth into positive territory since March, retail data continued to remain weak throughout this period, recording two consecutive QoQ contractions in the second (-1.3%) and third quarter (-0.2%), respectively. The declines were not broad-based though. Food sales rebounded in 3Q23, but they were unable to sufficiently offset the consistent losses from non-food and fuel items. Looking ahead, while private consumption could find some support in 4Q23 from the real wage gains which we expect to continue, we think the large bulk of the positive impact will be felt in 2024.

Recent gains in consumer confidence point to improvements in retail sales ahead

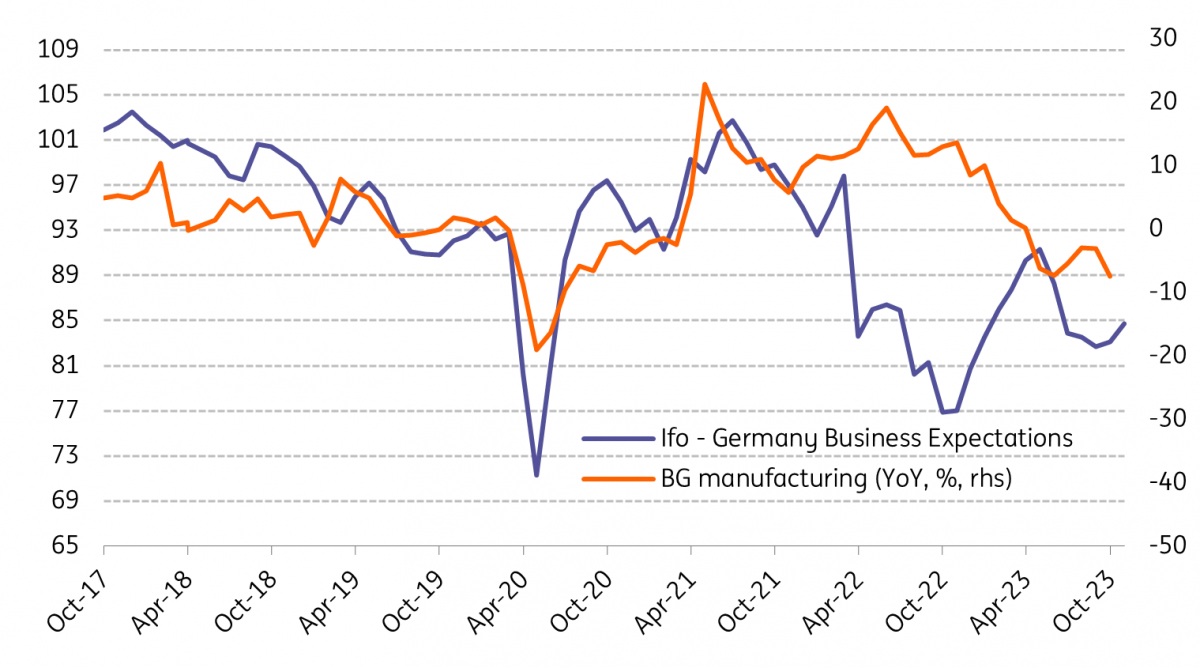

In industry, the negative developments continued – a new monthly contraction in September (-2.7%) cemented the fifth consecutive quarterly sequential drop and led to an overall 8.6% decline in year-to-date terms. The rather small QoQ rebound of the manufacturing sector and a stagnation in energy production activity over the same period offer some relief against another strong contraction in the mining industry. Looking forward, we expect only a small rebound in the industrial sector in 2024, which will likely not come even close to offsetting the losses of this year. This partly matches our below-consensus view regarding Bulgaria’s key trading partners' GDP growth in 2024.

Weakening external demand is a drag on industry

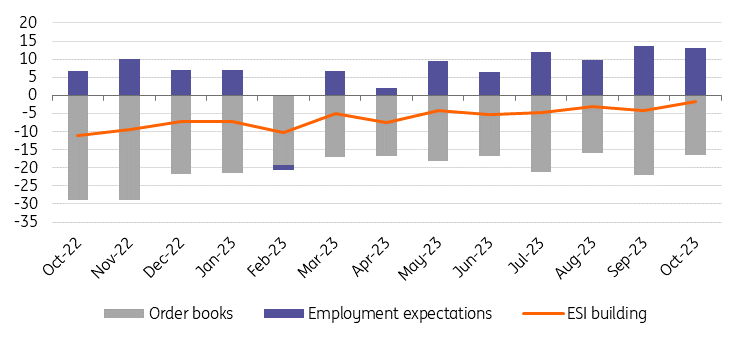

Construction data also remained weak – another sequential decline led to a year-to-date contraction of 1.2%. Civil engineering projects are largely to blame, dragging down the reading and more than offsetting the small year-to-date increase in buildings. Given the recent reforms, which go hand in hand with a stronger EU funds absorption, we don’t expect this trend to continue. As such, while still-high interest rates might continue to pressure residential and commercial projects in the near-to-medium term, civil engineering projects could benefit more as a direct outcome of a more stable political environment. Moreover, recent surveys point to improvements in order books and employment expectations for the whole sector.

Business surveys point to some recent improvements in order books and employment

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more