- Quick take

Broad-based decline in Polish inflation leaves room for further rate cuts

- 15 December 2025

- Poland

Although the November CPI reading was revised to 2.5% year-on-year from the previous estimate of 2.4%, the decline in inflation was broad-based. Food inflation eased, while the fall in core inflation was driven by both goods and services. With inflation at the central bank’s target, policymakers still have scope for rate cuts

CPI inflation down in November despite upward revision

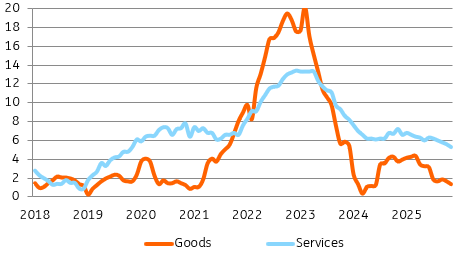

In November, CPI inflation moderated to 2.5% year-on-year from 2.8% YoY in October. Although the flash estimate was revised upward from 2.4% YoY, the detailed report clearly paints a broad-based disinflationary picture.

Prices of goods increased by 1.4%YoY, while services prices advanced by 5.3% YoY. In both cases, increases were slower than in October (1.7%YoY and 5.6%YoY respectively). Headline inflation eased by 0.3 percentage points vs. October due to slower food inflation and lower core inflation. According to our estimates, core inflation excluding food and energy prices fell to 2.7%YoY from 3.0%YoY in the previous month.

Downward pressure on core goods

In the case of food prices, November brought a decline in meat prices (-1.0% MoM), especially the most popular poultry (-4.1% MoM) and fruits (-0.2% MoM).

The decline in core inflation was broad and significant in both services and core goods. In the case of the former, there was a drop in tourism, both domestic (-1,6% MoM) and abroad (-3,4% MoM).

The downward pressure on tradable goods likely stems from China’s influence – both through low-cost imports and the competitive squeeze on domestic producers. Noteworthy price declines were reported in furniture and furnishings (-2.8% MoM), house appliances (-1.1% MoM), electronics (-1.2% MoM) and passenger cars (-0.6% MoM).

Central bank to resume rate cuts after a pause in early 2026

CPI inflation is already at the National Bank of Poland's (NBP's) target, and the inflation outlook looks favourable. Wage pressure on services prices is easing. American trade policy (protectionism) increases the inflow of inexpensive products from China to Europe. The energy shock is abating. The weak US dollar and stable energy commodity prices stabilise domestic fuel prices.

We expect the Monetary Policy Council to resume rate cuts at the turn of the first and second quarters of 2026 after a short pause. In our view, policymakers underestimate the scale of disinflation we are likely to experience in the coming quarters, and we still see room for adjusting rates to lower prices. We forecast the main policy rate may be reduced to some 3.25% by the end of 2026.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more