Bank of Korea preview: Rate cuts resume, but inflation caution clouds outlook

With the FX market stabilising and concerns about slowing growth intensifying, we expect the Bank of Korea to resume rate cuts next week. But inflation worries persist as trade war risks increase

| 2.75% |

BoK's 7-day repo rate |

The BoK is expected to resume its policy easing, but the decision may not be unanimous

We believe that the Bank of Korea's priority is supporting weak domestic demand, even as concerns about the inflation outlook keep policymakers on a hawkish footing.

The USDKRW fell to 1,440, but the move is in line with DXY trends. The political turmoil in Seoul that triggered excessive KRW weakness has abated since January’s policy meeting. Consumer-price inflation is rising at a 2% rate and pipeline prices are on the rise. Even so, we expect inflation to remain within the BoK's target range this year, giving it more latitude to cut. For now, the manufacturing sector is holding up relatively well despite tariff threats. US President Trump's reciprocal tariffs are likely to hit Korean manufacturers, increasing the odds the BoK's will remain skewed toward monetary easing on 25 February.

Yet, caution abounds. The BoK worries rate cuts could accelerate the rise in domestic household debt and property prices. As such, the BoK is likely to be extremely cautious in telegraphing more rate cuts. The central bank also is keeping a close watch on how the widening gap between the US and Korea yields affects the KRW.

Overall, we expect the BoK to cut rates four times this year, though each decision will likely be a close call. Case in point: next week's policy meeting could see a dissenting vote. Fewer than three BoK board members have expressed a clear openness to ease, which clouds market expectations over the next three months.

Next week, the BoK will publish its quarterly macro outlook report. We expect the BoK will lower its GDP forecast for 2025 to the 1.5%-1.6% range, which is still higher than ING's forecast of 1.3% growth, while hiking its inflation forecast to 2.0%.

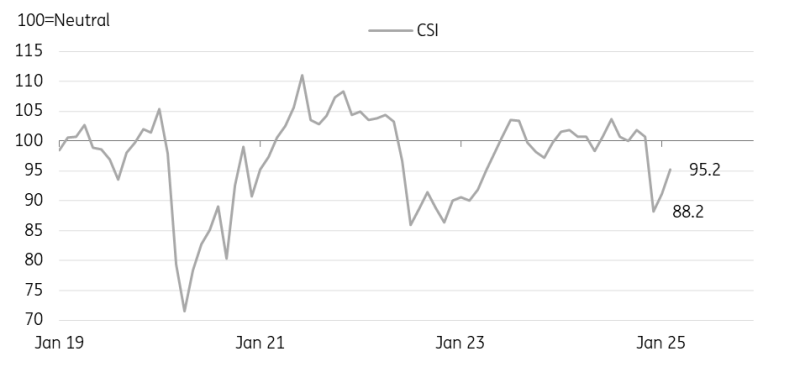

| 95.2 |

Consumer confidence index91.2 in January, 88.2 in December |

Consumer sentiment continued to recover for a second month after a sharp drop in December

The worst fears about December’s political turbulence slamming consumer confidence haven’t been realized. Since the end of 2024, data show that while sentiment remains below neutral, it hasn’t plunged as feared. Nor has financial volatility surged.

Meanwhile, inflation expectations eased to 2.7% in December from 2.8% in the previous month despite the recent acceleration in inflation. Expectations for inflation are relatively tame, which may come as a relief to the BoK. But with Trump’s tariffs heading Korea’s way, the BoK will take a wait-and-see approach to adding more monetary stimulus.

Consumer sentiment improved for a second straight month

| 1.7% YoY |

Producer prices0.6% MoM, nsa |

Pipeline inflation is on the rise

Producer prices held steady at 1.7% year on year in January for the second month, but monthly growth (0.6% MoM, not-seasonally adjusted) has accelerated in the past three months. Fresh food (4.0%) and energy prices (4.0%) rose the most. Services prices (0.4%), such as eating out (0.3%) and transportation (0.3%), also contributed. We believe that the rise in pipeline inflation will likely feed into consumer inflation with a time lag.

We expect consumer prices to hover around 2% for some time, but risks are to the upside. As a result, the BoK will be cautious about cutting interest rates. If prices rise more than expected, the government will try to curb inflation with various measures.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap