- Quick take

Base effects distort Hungarian wages data

- 26 April 2023

- Hungary

Average gross wages in Hungary rose by 15.6% year-on-year in February after excluding last year’s 'service premium' for the armed forces. Nevertheless, real wages have dropped for the sixth month in a row amid sky-high inflation

| 0.8% |

Gross earnings growthING Forecast 1.2% / Previous 16.1% |

| Lower than expected | |

The Hungarian Central Statistical Office (HCSO) released February’s wages data which indicates that average gross wages rose by a mere 0.8% year-on-year. At first sight, this figure might seem shocking, especially given that February’s inflation came in at 25.4% YoY. However, as we pointed out in our previous piece on wage data, there is a reason for this alarming headline figure: yearly base effects.

As the HCSO noted in its statement: “The change in the average earnings was considerably affected by the payment of the “service premium” (the so-called “firearms money”) for the army and the law enforcement personnel corresponding to six-month salary in February last year.”

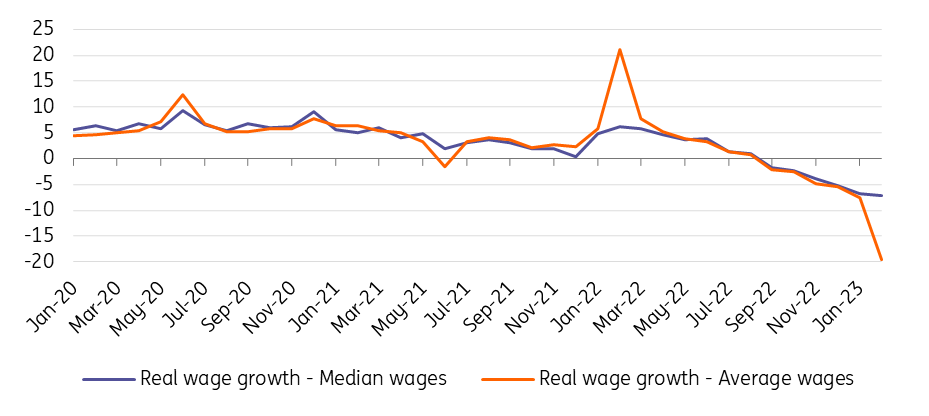

Considering the artificially-inflated wage growth number, the Statistical Office released adjusted data that more accurately reflects wage dynamics. Therefore, if we exclude last year’s “services premium”, which was a one-off payment, average gross wages rose by 15.6% YoY in February. Judging by the 16.3% YoY increase in median wages, we can conclude that lower earners are experiencing slightly more dynamic wage growth. However, in contrast to recent inflation figures, the loss of households’ purchasing power continues, with February marking the sixth month in a row in which real wage growth was negative.

Real wage growth in Hungary (% YoY)

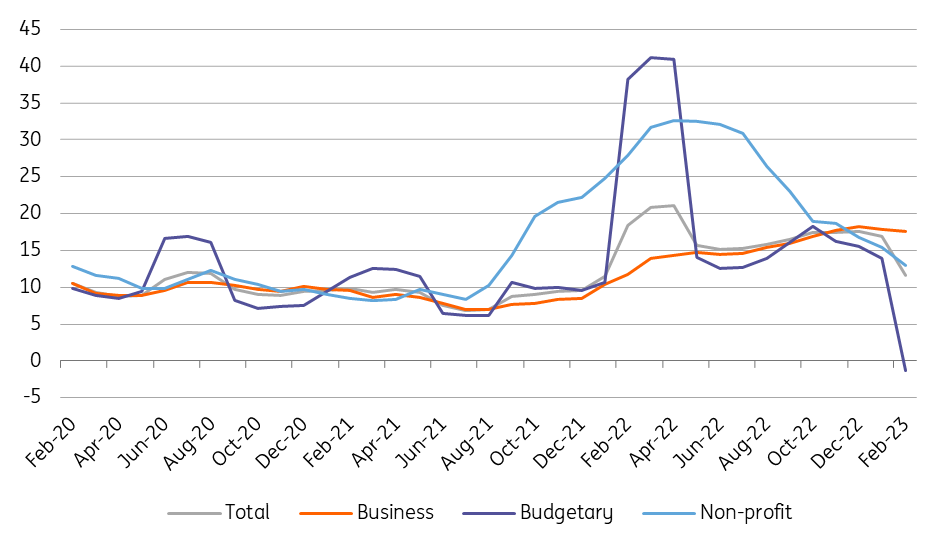

In the private sector, average gross wages increased by 17.6% YoY, while median gross wages rose even more dynamically jumping to more than 19% year-on-year. With this contrast in mind, it seems evident that companies attempted to offset the effects of sky-high inflation by increasing wages for lower-earning workers at the start of the year. However, digging deeper into the data, we can see that the only workers to have seen significant wage hikes either work in mining and quarrying or in transport and storage. In the former sector, one-off payments likely contributed to the hikes, while wage growth in the latter sector was probably driven up by labour shortages.

Wage dynamics (three-month moving average, % YoY)

Historically, the wage growth dynamics observed in the first few months of the year quite often determine the average wage growth rate for the whole year. Of course, in this case it only makes sense to consider the adjusted data which excludes last year’s “services premium”. Therefore, 2023 full-year wage growth can be expected to be somewhere around 16%. However, considering this year’s specificities (high uncertainty regarding growth and inflation), this figure is likely to be more towards the lower end of the forecast range as we see upside risks. Against this backdrop, several companies have finalised new wage agreements in the spring season, which could further increase average wage growth. Likewise, wage settlements in the public sector during the year indicate the same upside risk.

Despite the projected wage growth of 16-17% for this year, we still expect households’ purchasing power to decline as we see the full-year inflation figure hovering around 19%. However, inflation is expected to moderate significantly in the second half of 2023, which will lead to positive real wage growth starting from the end of the third quarter, in our view. This two-faced profile of real wage growth raises the question of whether it will stimulate demand (upside inflation risk) or promote savings (downside growth risk).

In our view, positive real wage growth will more likely encourage households to replenish their savings, as they have already used up their reserves to mitigate the effects of sky-high inflation. In this regard, we believe that the odds favour downside growth risks, rather than upside inflation risks.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more