- Quick take

- 11 January 2024

- South Korea

Bank of Korea: Rate cuts are only a matter of time, but there is no rush

The Bank of Korea (BoK) has kept its policy rate at 3.5% for the eighth consecutive meeting. But by removing “...need to raise base rate further…” from the statement, the BoK is opening the door to rate cuts. We expect the first cut in 2Q24, with inflation stabilizing in the 2% range, domestic growth conditions weakening and financial market stress rising

BoK trying to be hawkish while buying time with liquidity provisions to SMEs

The Bank of Korea is not in any hurry to cut rates, but rising default risks and the potential damage to financial markets may eventually force their hand. When? Currently, the market consensus shows 3Q24 as the most likely time for the first cut, but the inflation path and risks surrounding the real estate market could shift the timing of this back and forth. As our macro view is slightly more downbeat than the consensus and the BoK's view on Korea's economy, especially on domestic growth, we have pencilled in the first rate cut in 2Q24.

We believe that the BoK will continue to use its Bank Intermediated Lending Support Facility which can use up to KRW9tr of reserves to support SMEs. Also, last year, the BoK expanded its pipeline by accepting a wider range of collateral, including IG credits, which will give the BoK more options to respond to market changes before embarking on rate cuts.

The Bank of Korea is clearly concerned about the fast pace of growth of private debt and the side effects that premature rate cuts could have in terms of stimulating a property market bubble. The BoK believes that now is the time for an orderly deleveraging of private debt, thus they are quite firm about maintaining tight monetary conditions for now.

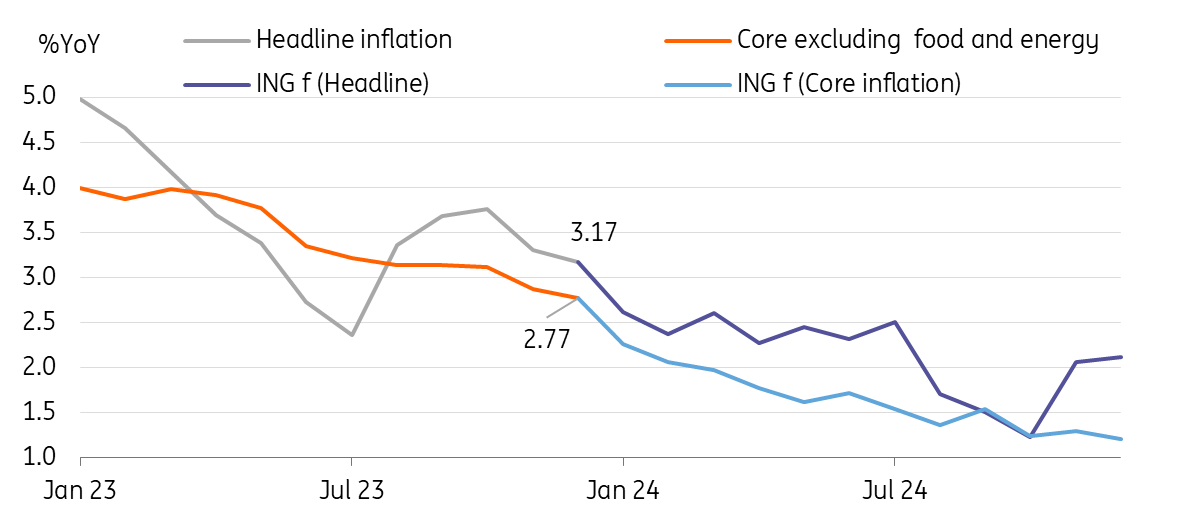

Inflation will be key to watch

We will likely see inflation slow down to a 2% range from January. Base effects should be the main contributor to the expected decline, but if gasoline and fresh food prices continue to fall, this will also help to drag down headline inflation. However, there is still significant uncertainty about the inflation path over the coming months.

Geopolitical tensions in the Middle East could also become important factors. We may also see cost-push inflation return more strongly in 2Q24 when several government price stabilization measures begin to sunset. By then, fuel tax cuts will be completed, and utility prices and other public service prices will likely increase, which could then stimulate second-round effects. Our base case scenario is that inflation will remain around the 2% range by mid-year and then go down to around 1% by the end of 2024 with demand side pressures cooling by then.

Inflation will come down to the 2% range soon

Key challenges facing growth

We think exports will be the main engine for growth at least for 1H24. But, the export recovery is quite narrowly focused on semiconductors. We expect the US economy to lose its growth momentum this year and China’s recovery will not likely be substantial, thus the semiconductor-driven export recovery will probably not be strong enough to lift overall growth.

The main challenge will be sluggish domestic demand. Default risks are increasing in the construction sector and tight mortgage rules will place a burden on an already weak property market. The government will likely step in if things get worse, so we don’t think this will trigger a major financial crisis, but investment and consumption will likely suffer.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more