Bank of England survey points to reduced inflationary pressures

The latest business survey from the Bank of England suggests price expectations are continuing to fall and the jobs market is cooling. Policymakers appear wary about putting too much emphasis on surveys, but the findings do bolster the case for another “on hold” decision in November

On the face of it, the latest Decision Maker Panel survey from the Bank of England helps vindicate the decision to keep rates on hold last month. This is a survey of Chief Financial Officers (CFOs) in the UK, and it continues to send all the right messages on inflation. These are the top lines:

- Three-year ahead CPI expectations down to 3.2%, and similar downward moves were observed for current/one-year ahead expectations.

- Expected price growth over the next year seen at 4.8%, down 0.2ppts and continues a steady downward trend from recent months.

- Wage growth seen at 5.1% over the next year, the same as last month, but around a percentage point off last December’s peak. That compares to the latest official data on private-sector wage growth in the 8% region.

- The proportion of firms finding it “much harder” to recruit is at 20%, down from a peak of 65% in summer 2022.

In other words, it suggests that inflationary pressures are continuing to ease, as are the strains in the jobs market. There are, however, two caveats to bear in mind.

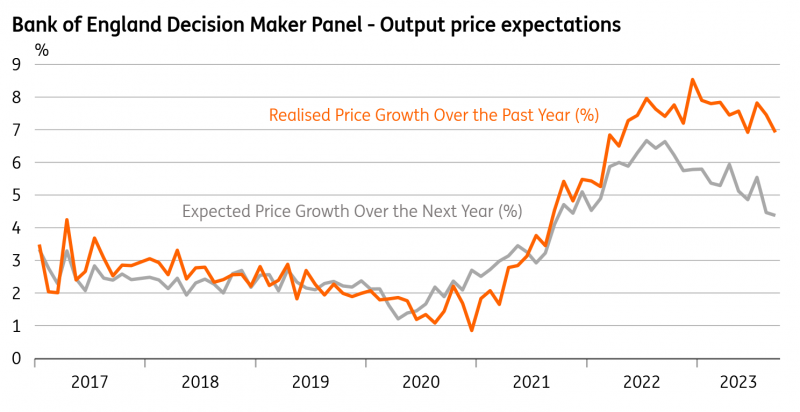

Firstly, the survey has consistently shown that “realised” price/wage growth has been higher than what firms are projecting for the future. In other words, companies are saying they expect to do one thing and ultimately, they're ending up acting more aggressively, as the chart below shows.

Expected price growth is typically below "realised" price increases

Secondly – and partly for that reason – the Bank of England appears more wary about basing policy on survey evidence than it might have done in the past. Yesterday’s big upside revision to the services PMI (from 47.2 to 49.3) will only reinforce that scepticism, and as others have noted, this may well be down to issues with seasonal adjustment processes after the pandemic. For now, the Bank has made it abundantly clear that it’s focused on private sector wage growth, services inflation, and the vacancy-to-unemployment ratio (as a gauge of jobs market tightness), and not a lot else.

We’ll get fresh data on all those things in a couple of weeks' time. But barring any unwelcome surprises, we think the Bank will be content with keeping rates on hold again in November.

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more

Download

Download snap