- Quick take

Bank of England surprises again with a pre-Christmas rate hike

- 16 December 2021

- United Kingdom

Upside surprises to inflation have convinced the UK central bank of the need to tighten pre-emptively. We expect two, or at most three, rate rises next year. However, we think policymakers will wait until after February's meeting before moving again when more data on Omicron's impact will have arrived

The Bank of England has increased interest rates for the first time since the Covid-19 crisis began, despite the mounting uncertainty surrounding Omicron.

Inflation has twice come in above expectations since the Bank’s November forecasts, and that’s what seems to have swung it for policymakers. There’s also been no discernible turbulence in the jobs market since the furlough scheme ended in September, which was a key test that policymakers had put forward last month. Policymakers are calculating that in a year-or-so time, when rate decisions today will realistically filter through to the economy, the outlook will be little changed by Omicron.

Perhaps the biggest surprise is how many committee members voted for the hike

In practice, the decision to hike rates soon was not in question anyway – but we had assumed that policymakers would wait until February. So perhaps the biggest surprise today is how many committee members voted for the hike. The decision to delay increasing rates last month suggested there were several policymakers yet to be fully convinced of the merits of tightening right now - and if anything uncertainty has risen since last month. However, the move was voted through 8-1.

All of this poses two key questions:

Will today’s move be followed by a full 25bp rate hike at the February meeting?

It’s possible but for now we suspect not. We agree with the Bank of England that (as things stand) Omicron probably won’t change the medium-term picture decisively. But in the short term, it still means turbulence for the UK economy.

Much depends on hospitalisations and the extent of any further restrictions. But raw case numbers still matter for the economy, and widespread staff shortages in late December/early January are very likely given how quickly Omicron is spreading. Meanwhile, social spending is likely to fall rapidly as households limit contacts in the run-up to Christmas, and we’re already seeing signs of that in the latest restaurant booking data. We also don’t yet know how generous government support for businesses is likely to be this time around.

We’re inclined to say that policymakers will wait until later into 2022 before hiking again.

How many rate rises are we looking at next year?

Markets think that rates will need to rise quickly next year and that the Bank rate will hit 1% by late next year. We still suspect that’s an overestimate.

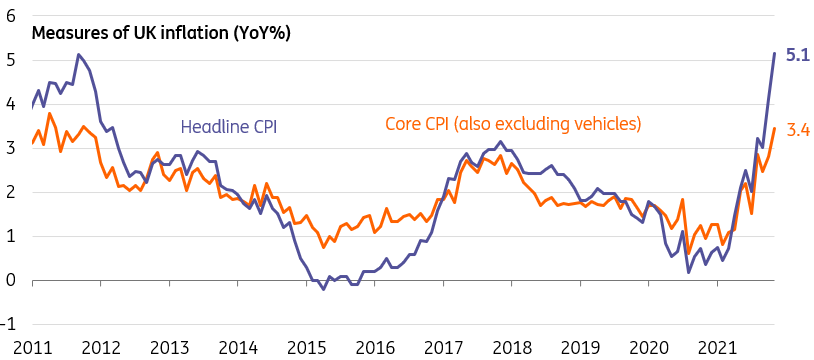

True, inflation rates are only currently going in one direction, and headline CPI will likely peak well above 5% in April.

But most of the recent upside surprises are coming from the same set of components – principally energy and used cars. Once you filter that out, core inflation is at 3.4%. That’s still elevated, but probably not enough to justify the rapid succession of rate rises markets expect. Bear in mind too that recent data suggests wage growth is currently more modest than recent labour shortages imply.

Remember as well that the Bank of England has said it plans to begin shrinking its pool of bonds amassed under quantitative easing. That will start after the next rate hike, and will do some of the heavy lifting for the BoE.

In short, we expect two (or at most three) rate rises next year. We’re penciling in May and November at this stage.

Filtering out cars, energy and food, inflation looks less exciting

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user's means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.Read more